en.Wedoany.com Reported - At the 2026 SMM (14th) Minor Metals Industry Conference Antimony Industry Forum, hosted by Shanghai Metals Market Information Technology Co., Ltd. (SMM) and titled by Guangxi Yusheng Germanium Industry High-Tech Co., Ltd., Luo Chengcai, General Manager of Hunan Tin Mine Flash Star Antimony Industry Import and Export Co., Ltd., shared insights on "The Transformation and Development Path of the Antimony Industry Amid a Century of Change."

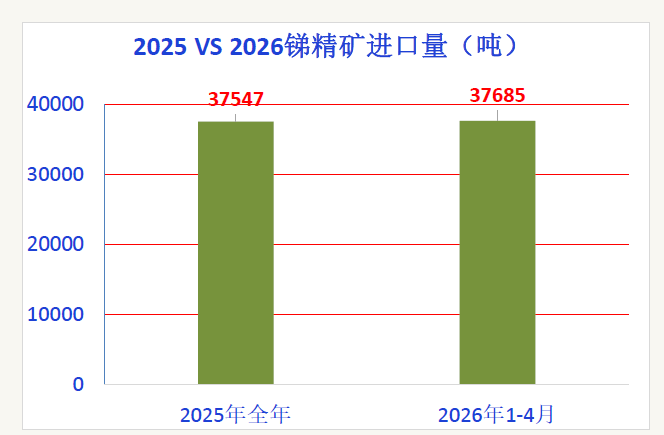

Luo Chengcai pointed out that the antimony industry is undergoing a century of change, with a reshaping of its landscape. In terms of policy, export controls have triggered profound market shifts. High prices in overseas markets are driving rapid capacity expansion, with Myanmar's Three Towers Mine producing 1,000 tons of metal content per month, demonstrating strong supply resilience. Smelting capacity in Southeast Asian countries such as Thailand, Myanmar, and Vietnam is increasing rapidly, with total overseas production capacity reaching approximately 40,000 tons per year. The domestic market faces supply-demand imbalances, with import volumes in the first four months of 2026 already matching the total for the entire year of 2025, creating unprecedented supply pressure and intense demand competition leading to significant price declines. In terms of geopolitical impacts, the Middle East conflict has caused irreversible damage: the flame retardant industry has suffered due to bromine prices rising from 30,000 to 130,000 yuan per ton and petrochemical raw material costs increasing by over 50%, with cost transmission failures leading to widespread industry losses and production cuts of about 30%. The polyester industry has been forced to reduce production by approximately 30% due to fluctuations in upstream petrochemical raw material prices. Photovoltaic glass has seen short-term demand weakening due to the cancellation of export tax rebates for modules and uncertainty in the Indian market, but the global energy transition trend remains unchanged, with long-term growth potential still intact.

Luo Chengcai believes that within the crisis lies opportunity, and there are new prospects for transformation and development. The traditional sectors maintain a stable foundation: high-performance flame retardant materials are irreplaceable in engineering plastics such as ABS and XPS, with China's annual demand for flame retardants reaching 1.5 million tons, of which bromine-antimony flame retardants account for 35%. In the polyester industry, over 90% of polyester units use antimony-based catalysts, and industrial textiles are growing at an average annual rate of over 10% in sectors like healthcare and new energy. Antimony-based clarifying agents hold over 80% of the market share in photovoltaic glass, with strong overseas demand. In terms of new growth drivers, condensed matter batteries represent the biggest future engine. Companies like CATL are planning antimony-based sodium-ion batteries using calcium-antimony composite materials as anodes, with 24 GWh of the planned 60 GWh capacity allocated for passenger vehicles. Based on an antimony requirement of 1,200 tons per GWh, full production would demand 30,000 tons of antimony annually. High-value applications are growing rapidly, with AI computing power driving antimony consumption in the semiconductor sector to over 2,000 tons. In the military field, high-purity antimony commands a premium of 3 to 5 times, with orders growing 80% year-on-year. In lead-acid batteries, antimony is used in positive grid plates, with global antimony usage at approximately 22,000 tons, of which China accounts for 13,000 to 15,000 tons.

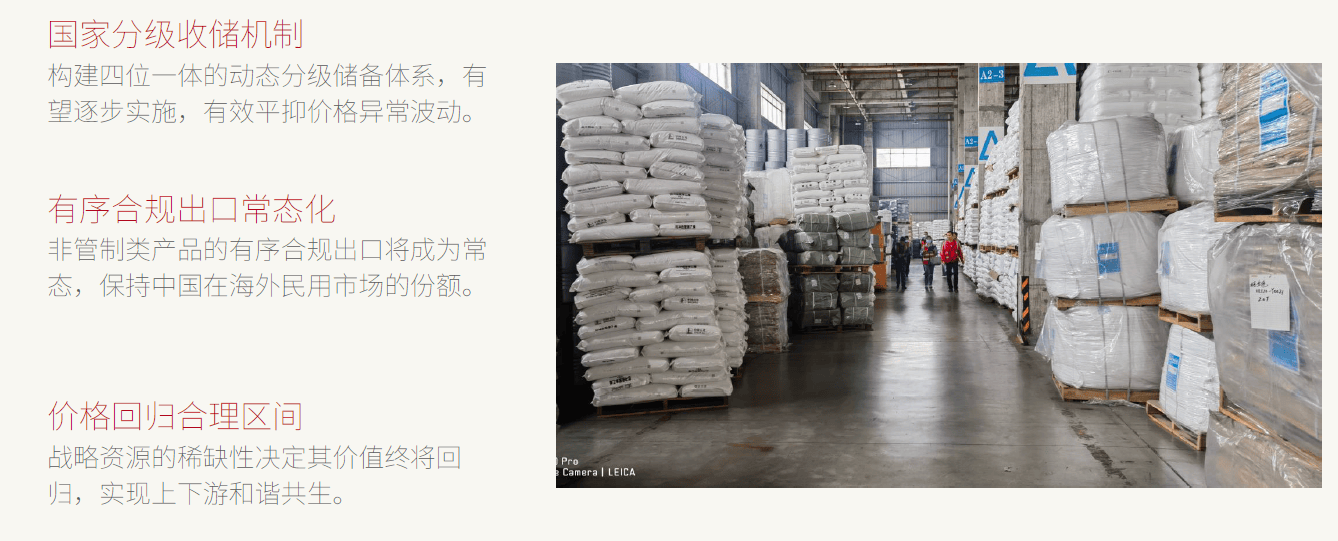

On the supply side, resource constraints and policy regulation have become the norm. Domestic resources are depleting, ore grades are declining, and production is decreasing year by year. Overseas incremental supply is limited and unstable. The global static reserve-to-production ratio for antimony is less than 10 years, making it inevitable for countries to strengthen environmental protection, implement production limits, and promote resource integration. Luo Chengcai stated that the antimony industry is at a new historical starting point. Short-term market fluctuations and price pains are necessary processes for structural adjustment. As supply tightens, emerging demand surges, and national strategic attention increases, the strategic value of antimony will be highlighted, ultimately returning to its intrinsic value amid the supply-demand balance.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com