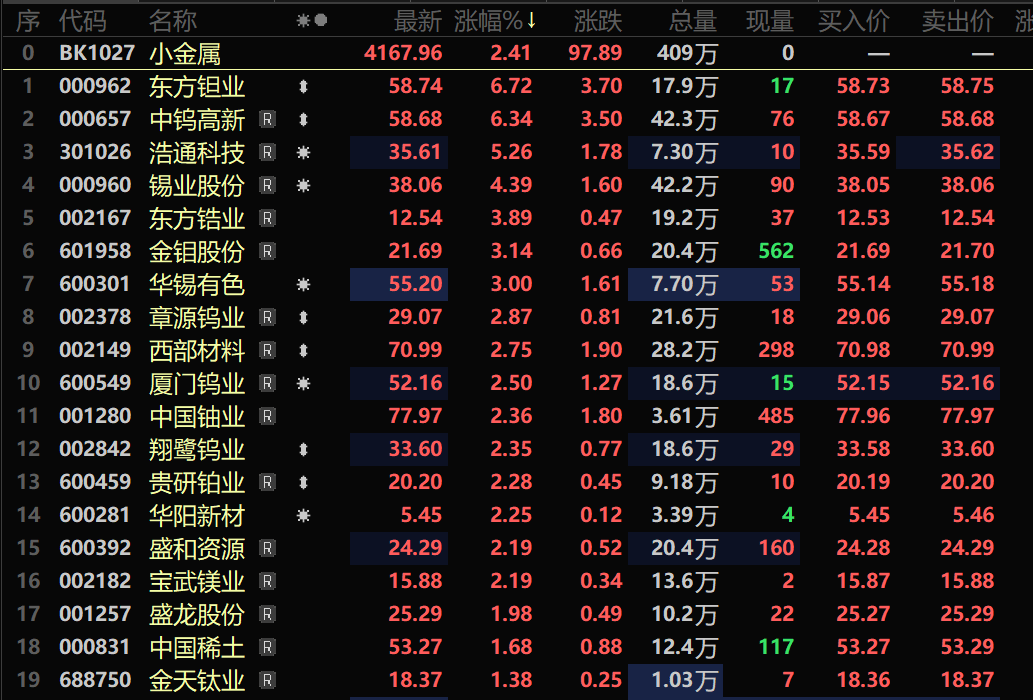

en.Wedoany.com Reported - On May 21, the minor metals sector opened stronger, with the sector's gain reaching 2.41% as of 10:22 AM that day. Dongfang Tantalum and China Tungsten & Hightech rose over 6%, while stocks such as Haotong Technology, Tin Industry Co., Dongfang Zirconium, Jinduicheng Molybdenum, and Huaxi Nonferrous led the gains. Market analysis indicates that this rally is directly driven by fundamental improvements in the spot market, coupled with a weaker US dollar, strengthening strategic resource attributes, and rising demand from emerging sectors like artificial intelligence, semiconductors, and photovoltaics. Market expectations of persistently tightening supply and demand for minor metals have heated up, increasing the willingness of capital inflows and driving an overall sector rebound.

In the spot market, the specific trends for various varieties are as follows:

Tantalum

The quoted price for tantalum ingots (Ta≥99.95%) on May 20 was 6,600~6,700 yuan/kg, with an average price of 6,650 yuan/kg, up 1.53% from the previous trading day. The recent tantalum market has reached a turning point, with tantalum prices bottoming out, stabilizing, and beginning to rebound, gradually clarifying the industry's upward trend. Low-priced supply within the industry chain is being cleared at an accelerated pace, and quotations for various product categories are rising simultaneously, with the overall market steadily improving. Driven by expectations of positive news, some smelting enterprises have proactively tightened shipment pace and suspended external quotations, essentially depleting the circulating low-priced supply in the market. Bullish sentiment among traders and holders continues to heat up. Superimposed on the support from steadily rising raw material costs for upstream tantalum ore, the market expects that subsequent prices for tantalum oxide and tantalum ingots will continue their steady upward trajectory.

Tin

On May 21, the average price of SMM 1# tin rose 3.82% from the previous trading day. Alongside the rise in tin prices, market wait-and-see sentiment intensified, and transactions were relatively quiet. From a fundamental perspective, on the supply side, most smelting enterprises focused on stable production in May; on the demand side, downstream procurement was cautious, mostly executed based on orders.

Rare Earths

In the spot market, on May 21, supported by demand from major factory purchases, the average price of praseodymium-neodymium oxide rose 1.81% from the previous trading day.

Institutional Voices

A research report from Sinolink Securities on May 18 pointed out that the central price of rare earths has been continuously rising since the beginning of the year, which may be significantly correlated with supply-side documents released from 2024 to 2025, as industry supply reform continues to advance. Exports for the full year 2025 decreased by 1% year-on-year, but exports have increased significantly since the beginning of 2026, indicating substantial overseas restocking demand. The rare earth sector will continue to evolve with both valuation and earnings rising, and 2026 is also a key year for resolving horizontal competition among key targets. Regarding tin, the institution believes that hidden tin ingot inventories are gradually drying up. Under macro liquidity replenishment or technology market spillover, tin prices are expected to strengthen, and the long-term supply-demand pattern for tin will be favorable. Regarding molybdenum, the current price of molybdenum concentrate is 5,210 yuan/mtu, up 10.50% month-on-month; the current price of ferromolybdenum is 324,000 yuan/ton, up 9.46% month-on-month. The degree of imported ore destocking is high, and domestic molybdenum prices have stabilized and rebounded. Steel tender volumes remain prosperous, the industry chain upstream and downstream is destocking, and the deadlock of "volume without price" for molybdenum is gradually breaking, further clarifying the upward channel. Molybdenum is also a defense-related metal, with inventories remaining low; increased overseas defense spending may further drive up molybdenum prices. Regarding tantalum, the tantalum industry is expected to benefit from a boom driven by high-end demand. Related targets include Dongfang Tantalum, Xinjinlu, and Jiangwu Equipment.

CITIC Securities released a research report on May 13 stating that in 2025 and the first quarter of 2026, performance growth in the metals industry generally accelerated, with tungsten, lithium, lead-zinc, and rare earth magnetic materials leading the gains, while aluminum, copper, nickel-cobalt-tin-antimony, and gold have performed relatively weakly since the beginning of the year. The current valuation of the metals sector remains at a reasonable level, with aluminum, copper, nickel-cobalt-tin-antimony, and gold valuations at relatively low levels, making a valuation recovery still anticipated. Industry dividends have slightly declined, but the predicted dividend yield for some individual stocks still exceeds 5%. Looking ahead to 2026, as liquidity shocks ease, supply disruptions occur frequently, and certain downstream sectors maintain high prosperity, it is recommended to continue focusing on allocation opportunities in lithium, copper, rare earths, strategic metals, aluminum, and gold sectors.

Guotai Haitong Securities believes that since 2024, rare earth prices have gradually bottomed out, the tone of slowing domestic quota indicators continues, and overseas rare earth development expectations are fermenting but actual progress may fall short of expectations. On the demand side, sectors such as Automotive Industry" target="_blank">new energy vehicles, home appliances, and wind power maintain the base, while humanoid robots form a long-term upward option, and the curtain on a supply-demand reversal has already risen. As a strategic domestic commodity, rare earths are expected to experience a dual boost in profitability and valuation.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com