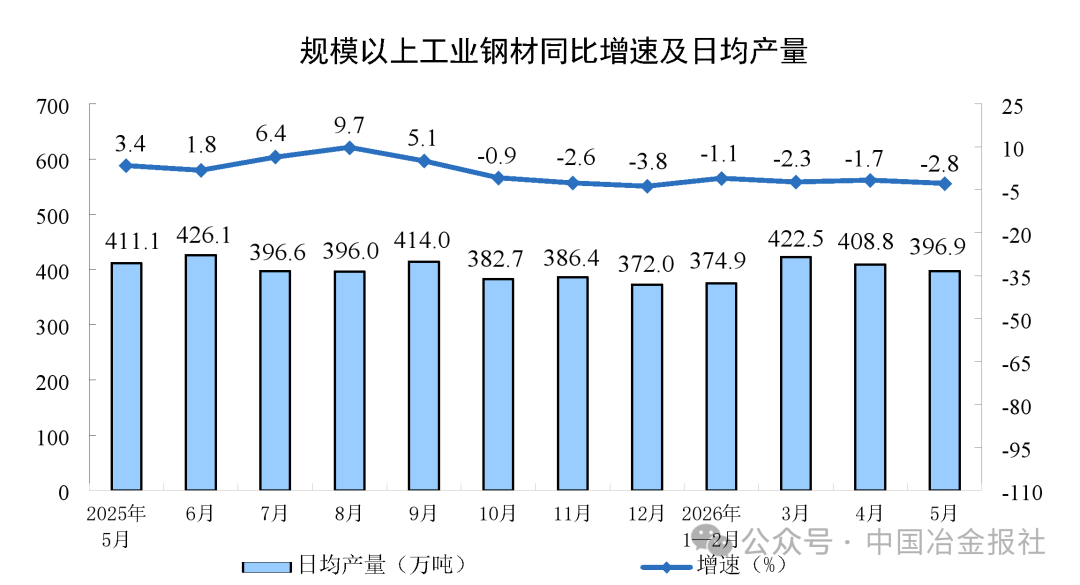

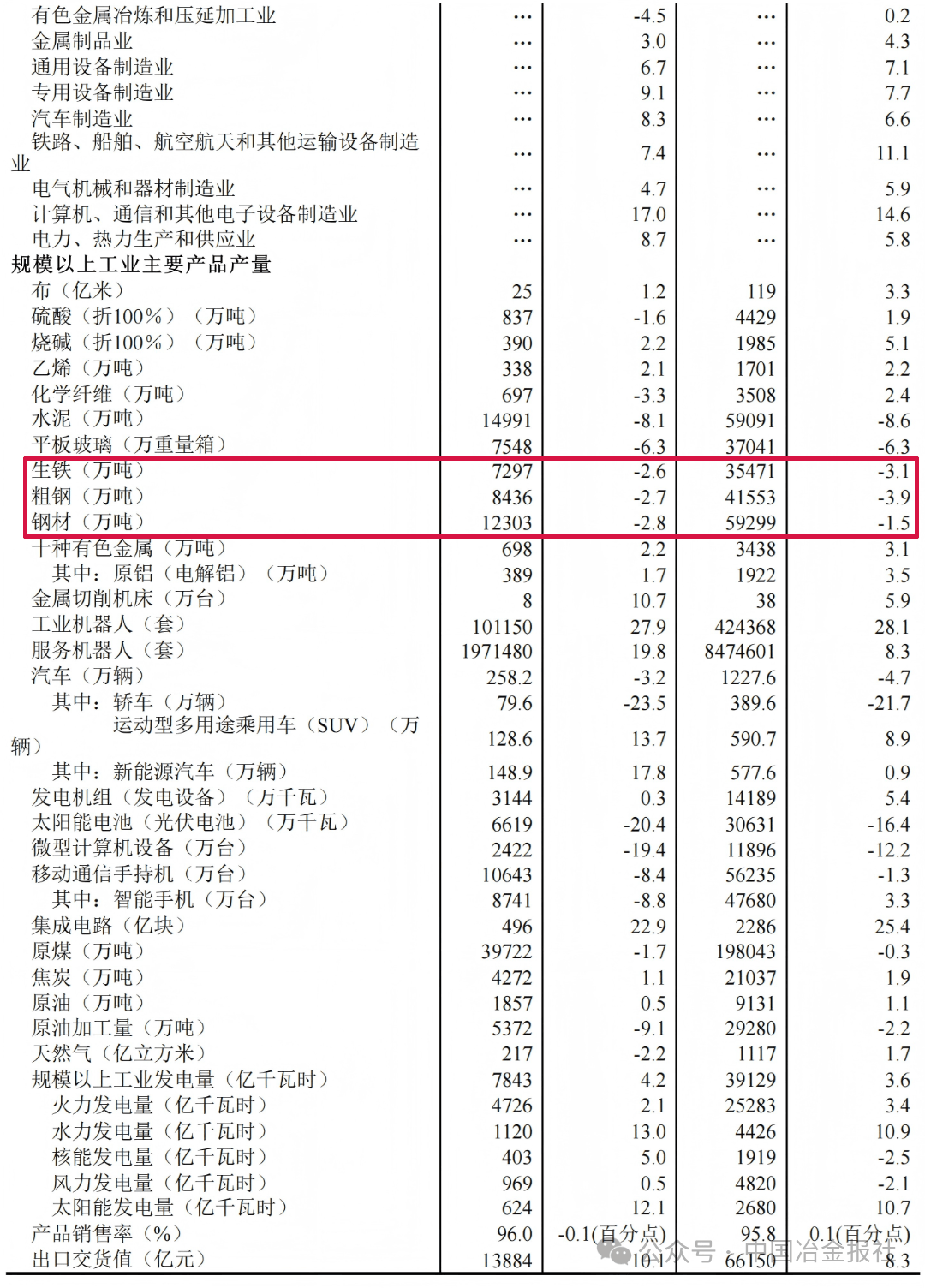

en.Wedoany.com Reported - Data released by China's National Bureau of Statistics in mid-June 2026 shows that from January to May 2026, China's crude steel output stood at 415.53 million tons, down 3.9% year-on-year; steel product output reached 592.99 million tons, down 1.5% year-on-year; and pig iron output was 354.71 million tons, down 3.1% year-on-year. In May alone, crude steel output was 84.36 million tons, down 2.7% year-on-year; steel product output was 123.03 million tons, down 2.8% year-on-year; and pig iron output was 72.97 million tons, down 2.6% year-on-year.

Looking at monthly data, China's average daily crude steel output in May was approximately 2.72 million tons, down from April. During the same period, the added value of the ferrous metal smelting and rolling processing industry grew by 1.8% year-on-year, with a 1.6% increase in May alone, indicating that overall production activity in the sector still maintained some resilience, though the growth rate slowed compared to earlier periods. NBS data also showed that from January to May, China's fixed asset investment grew by 3.2% year-on-year, of which infrastructure investment rose by 5.6%, real estate development investment fell by 8.0%, and construction-related demand had a limited pulling effect on steel consumption.

In 2025, China's crude steel output was 1.009 billion tons, down 0.8% year-on-year. Output in the first five months of 2026 continued its downward trend, with the decline widening to 3.9%, reflecting a situation where steel enterprises are actively or passively reducing production amid pressure on the demand side. According to data from the China Iron and Steel Association, as of late May 2026, steel product inventory at key statistical steel enterprises was about 15.8 million tons, up from the beginning of the year, indicating ongoing destocking pressure. Industry analysis points to the persistent decline in real estate investment, the slowdown in infrastructure investment growth, and structural changes in manufacturing steel demand as the main reasons for the drop in crude steel output.

On the market front, China's steel prices have generally shown a volatile downward trend since 2026. According to data from Mysteel, the average price of domestic rebar at the end of May was about 3,650 yuan per ton, down about 8% from the beginning of the year. Imported iron ore prices also fell in tandem, with the price index for 62% grade iron ore dropping to about $95 per ton, down about 15% from the start of the year. The divergence between falling raw material costs and declining steel prices has continuously narrowed profit margins for steel enterprises. According to NBS data, total profits in the ferrous metal smelting and rolling processing industry fell by about 30% year-on-year from January to April. Industry self-discipline in production control and supply-demand rebalancing remain core challenges facing the steel sector.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com