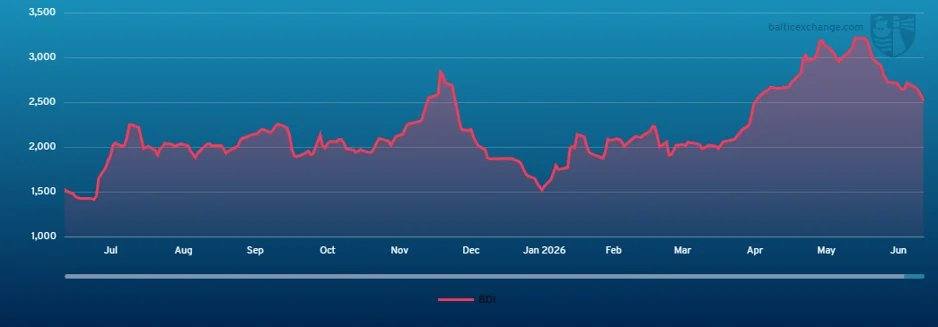

en.Wedoany.com Reported - The Baltic Dry Index (BDI) declined again last week, closing at 2,524 points on June 26, 2026, down from 2,722 points a week earlier.

The Capesize market experienced a tough week, with early cautious optimism quickly replaced by widespread weakness across both ocean basins. The week started with relative balance, supported by a strong close the previous Friday, increased activity in the South Atlantic from Brazil and West Africa, and steady participation from Pacific miners. However, as cargo volumes dwindled and available tonnage continued to increase, market resilience faded. Major miners remained present in the Pacific, but not enough to support rates, with the C5 route falling from $11.65 to $10.20 by the weekend. The Atlantic market was initially supported by inquiries from South Brazil and West Africa, with C3 levels firming, but subsequently came under pressure from reduced cargo volumes and an increasing number of ballasting vessels, with C3 rates dropping from $32.50 to $28.00. The North Atlantic showed relative resilience, supported by sporadic transatlantic and front-haul inquiries, but failed to reverse the overall negative trend. The BCI 182 5TC fell from $36,946 to $33,014 over the week, putting the market on the defensive.

The Panamax/Kamsarmax market had a tentative start to the week, with the P5TC declining amid mixed sentiment in the Atlantic and a weaker Pacific market. Atlantic activity improved mid-week, with an 82,000 dwt vessel fixing a transatlantic cargo from the East Coast of South America at $32,000, and a similar vessel later achieving $34,000. In front-haul business, an 83,000 dwt vessel delivering in India fixed early at $20,000, rising to $21,000 for an 82,000 dwt vessel by the weekend. Tightening tonnage in Northern Europe and increased cargo volumes in transatlantic and front-haul trades supported sentiment, pushing the P5TC higher later in the week. The Pacific market stabilized after early weakness, with owners resisting lower rates. A 75,000 dwt vessel delivered in South Korea fixed at $12,900 for an Australia round voyage, while an 80,000 dwt vessel delivered in China fixed at $14,250 for an Australia to Singapore-Japan voyage. Period activity slowed, with a 78,000 dwt vessel delivered in the Far East fixing for one year at $15,750.

The Supramax/Handysize segment was subdued this week, with the Atlantic remaining the stronger region, though activity levels in the US Gulf gradually diminished towards the weekend. The South Atlantic showed slight resilience, with limited reported fixtures. A 63,000 dwt vessel fixed from the Continent with scrap to the East Mediterranean at $23,000. Downward pressure emerged in the Asian region, with slow inquiry for coal from the south. A 57,000 dwt vessel delivered in the Philippines fixed via South China for redelivery in Bangladesh with clinker at $18,000. Additionally, a 63,000 dwt vessel fixed at $18,500 for a North Pacific round voyage, delivery North China. Backhaul business was relatively slow, with a Supramax fixing at $21,500, delivery China via the Gulf of Aden to the Mediterranean. Period demand was slow, with a 63,000 dwt vessel delivered in India fixing short period at $21,000.

The Handysize market remained stable to firm this week, supported by tight tonnage and steady demand in the South Atlantic and US Gulf regions. A 38,000 dwt vessel fixed from Fazendinha to the Continent at $24,000. The Continent and Mediterranean were largely stable, supported by scrap demand. A 31,000 dwt vessel fixed from Liverpool to Jorf Lasfar with scrap at $17,000. In Asia, conditions were broadly balanced but quiet, with a 30,000 dwt vessel delivering Kaohsiung on June 25/26 for a trip to the West Coast of India at $17,000.

In the clean product tanker market, the LR2 TC1 route (75kt Middle East/Japan) index rose 18.88 points to WS509.44; the TC20 route (90kt Middle East/UK-Continent) rate increased from $9.38 million to $9.93 million; the TC15 route (80kt Mediterranean/East) index edged down $37,000 to $4.32 million, with TCE slightly above $20,300/day. The LR1 TC5 route (55kt Middle East/Japan) index added 18.75 points to WS528.13; the TC8 route (65kt Middle East/UK-Continent) index fell $21,385 to $8.26 million. The MR TC17 route (35kt Middle East/East Africa) index rose from WS542.14 to WS554.22 mid-week before retreating to WS540. Continent MR freight rates fell, with the TC2 route (37kt ARA/US Atlantic Coast) down 11.25 points to WS125.31, TCE at $4,355/day. US Gulf MR rates continued to decline, with the TC14 route (38kt US Gulf/UK-Continent) index down 12.86 points to WS137.14, TCE at $7,673/day; the TC21 route (38kt US Gulf/Caribbean) fell $32,143 to $553,571, TCE dropping to $10,700/day; the MR Atlantic triangle combined TCE fell from $20,244/day to $16,836/day. Handymax Mediterranean rates bottomed out, with the TC6 route (30kt Cross-Mediterranean) steady at WS170, TCE at $14,378/day; the TC23 route (30kt Cross-UK-Continent) fell 16.94 points to WS187.5, TCE at $15,229/day.

In the VLCC market, the TD3C route (270,000 mt Middle East Gulf to China) index fell sharply by 33% to WS318.89, with TCE near $313,000/day; the TD34 route (Oman to China) was assessed at WS220, down 24 points from last Friday. In the Atlantic, the TD15 route (260,000 mt West Africa to China) rate edged down to WS188.44, TCE at $165,289; the TD22 route (US Gulf to China) rose $238,889 to $21,361,111, with TCE slightly above $146,600/day.

In the Suezmax segment, the TD20 route (130,000 mt Nigeria/UK-Continent) rate rose about 56 points to WS238.61, TCE at $115,400/day; the TD27 route (Guyana to UK-Continent) rose from WS168 to WS234, TCE slightly above $114,000/day; the TD33 route (145,000 mt USG/UKC) rose 54 points to WS198. The Black Sea TD6 route (135,000 mt CPC/Augusta) rate strengthened to WS266, TCE at $169,700/day.

In the Aframax market, the North Sea TD7 route (80,000 mt Cross-UK-Continent) rate edged up 5 points to WS145, TCE near $47,400/day. The Mediterranean TD19 route (80,000 mt Cross-Mediterranean) fell 33.28 points to WS153.5, TCE slightly above $33,240/day. The Atlantic market strengthened, with the TD26 route (70,000 mt East Coast Mexico/US Gulf) rising from WS174.72 to WS193.06, TCE around $41,300/day; the TD9 route (70,000 mt Covenas/US Gulf) rising from WS169 to WS191, TCE slightly above $42,100/day; the TD25 route (70,000 mt US Gulf/UK-Continent) rising 28.33 points to WS191.94, TCE slightly above $40,513/day. For Vancouver exports, the TD28 route (80,000 mt crude Vancouver to China) rose $80,000 to $3,130,000, TCE around $47,300/day; the TD29 route (80,000 mt crude Vancouver to US West Coast) rose 4.5 points to WS230.5.

The LNG market faced downward pressure, with most routes declining. The BLNG1 Australia-Japan route fell $5,200 week-on-week to $75,000/day; the BLNG2 US Gulf-Continent route bucked the trend, edging up $1,600 to $90,100/day; the BLNG3 US Gulf-Japan route fell $1,800 to $99,200/day. Period market sentiment weakened, with six-month rates down $1,600 to $99,800/day, one-year rates down $2,400 to $77,633/day, and three-year rates down $1,300 to $78,900/day.

The LPG market continued to face pressure with subdued activity. The BLPG1 Ras Tanura-Chiba route closed at $211.25, with TCE earnings at $205,504/day; the BLPG2 Houston-Flushing route fell $14.75 week-on-week to $90.25, with TCE earnings down $21,119 to $92,027/day; the BLPG3 Houston-Chiba route fell $21.92 to $158.08, with TCE earnings down $19,620 to $73,574/day.

The container market was relatively quiet this week. On the Pacific routes, FBX01 (China/East Asia to US West Coast) rose $89 from last Friday to $6,180, up $2,955 since early June; FBX03 (China/East Asia to US East Coast) fell $208 to $7,869, up $2,787 since the start of the month. On the North Europe route, FBX11 (China/East Asia to North Europe) fell $58 week-on-week to $4,782, up $1,814 since early June; the Mediterranean route FBX13 (China/East Asia to Mediterranean) was largely flat, closing at $6,455, up $2,091 since the start of the month.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com