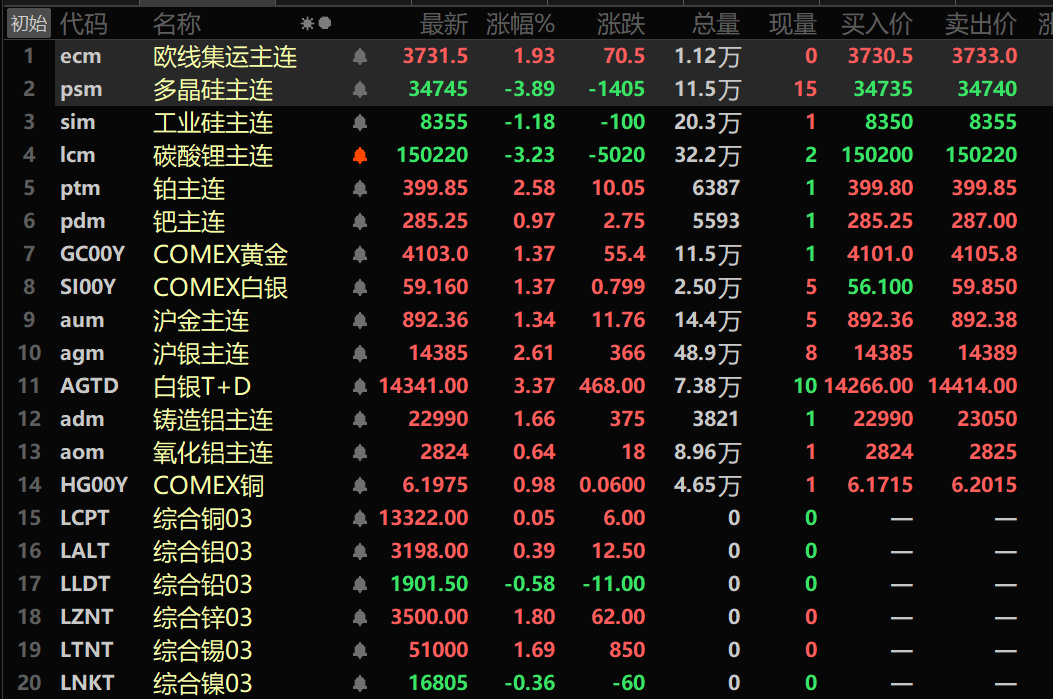

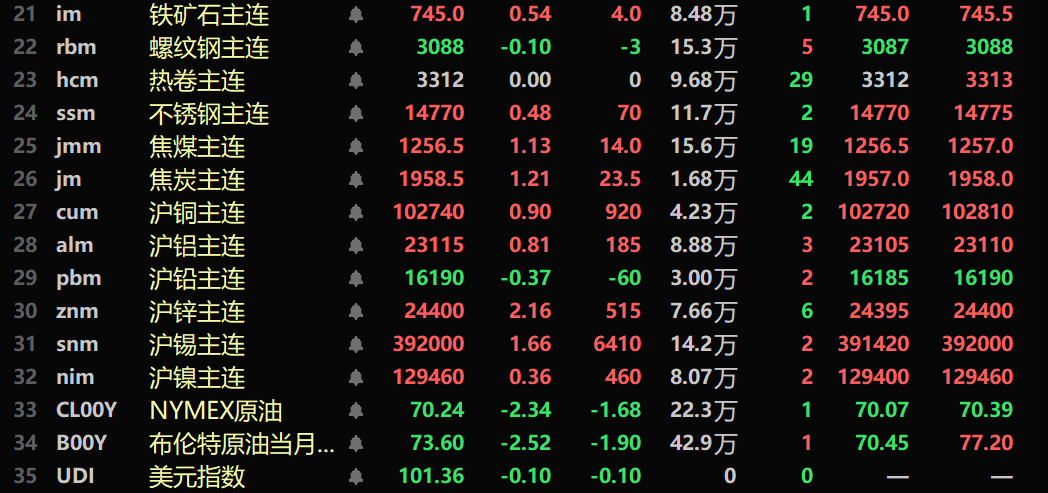

en.Wedoany.com Reported - Base metals markets showed a broad uptrend overnight. On the Shanghai Futures Exchange (SHFE), zinc led gains, rising 2.16%, copper up 0.9%, aluminum up 0.81%, tin up 1.66%; nickel up 0.36%, lead down 0.37%. Alumina main contract rose 0.64%, and cast aluminum main contract rose 1.66%. Most ferrous metals were in positive territory, with stainless steel up 0.48%, iron ore up 0.54%, rebar down 0.1%, and hot-rolled coil flat at 3,312 yuan/ton. In the coking coal and coke sector, coking coal main contract rose 1.13%, and coke main contract rose 1.21%.

On the London Metal Exchange (LME), base metals were broadly higher. LME copper edged up, aluminum up 0.39%, lead down 0.58%, zinc up 1.8%, tin up 1.69%, nickel down 0.36%.

In precious metals, COMEX gold rose 1.37%, posting a fourth consecutive weekly decline, down 3.37% for the week; COMEX silver rose 1.37%, falling for seven consecutive weeks, down 10.79% for the week. On the SHFE, gold main contract rose 1.34%, down 6.33% for the week; silver main contract rose 2.61%, down 15.23% for the week. Macquarie strategists said the market is focused on inflation trends and central bank policy moves; the easing of Middle East conflicts combined with the Fed's hawkish stance led to a pullback in gold prices. Macquarie forecasts an average spot gold price of $4,641 in 2026, up 35% year-on-year, but expects the average price to fall 9.5% to $4,200 in 2027, declining annually thereafter through 2030; the bank lowered its year-end spot gold forecast from $4,400 to $4,300. Macquarie believes that the tone of Fed Chair Warsh's first meeting was "hawkish," and under his leadership, the central bank has the ability to "drive or suppress" gold market prices; the shock from the Middle East situation is expected to drag on global growth in the third quarter, after which a rebound in global growth and the start of a monetary policy easing cycle should push gold prices lower as more investor funds shift from precious metals to other assets; investors have been taking profits and rotating into equities, creating room to re-enter the precious metals space, but a major macro event may be needed to rekindle investor interest in gold.

On the macro front, data from China's National Bureau of Statistics (NBS) showed that from January to May, industrial enterprises above a designated size achieved total profits of 3,143.96 billion yuan, up 18.8% year-on-year. Among them, profits in the electronics industry surged 103.9%, contributing 43.1% to the profit growth of all industrial enterprises; Yu Weining, chief statistician of the NBS's Department of Industry, said the electronics industry played a significant supporting role. Additionally, a series of seven Chinese standards for "Artificial Intelligence - Intelligent Agent Interconnection" were officially released, covering core areas such as overall architecture, identity management, and agent interaction. The People's Bank of China and the General Administration of Customs are soliciting public opinions on the "Measures for the Administration of Import and Export of Gold and Gold Products." The Ministry of Finance, the Ministry of Natural Resources, and the State Taxation Administration jointly issued a document, clarifying that from August 1, 2026, late payment penalties for mining rights transfer fees will no longer be levied; from the date of default, a penalty of 0.2% per day will be charged, not exceeding the principal amount of the overdue payment; late payment penalties incurred before the implementation date will continue to be paid according to the original regulations.

In the foreign exchange market, the US dollar index fell 0.1% overnight to 101.36, posting a second consecutive weekly gain, up 0.6% for the week. The CME FedWatch Tool showed the probability of one rate hike this year remained at 42%, while the probability of a second hike fell from 34% to 28%. A Reuters poll showed that 78 out of 102 economists expect the Fed to keep the federal funds rate unchanged at 3.50% to 3.75% in 2026. Artem Sakhbiev, a foreign exchange strategist at BCA Research, said the recent dollar rebound appears overdone and lacks support to break out of its trading range over the past year; the Fed's upward revision of its rate forecast and clear focus on inflation led to higher real yields and boosted the dollar, but this move has largely ended. According to Nick Timiraos, the "Fed whisperer," the selection process for the new president of the Federal Reserve Bank of Atlanta has hit a deadlock, with initial candidates failing to be confirmed, forcing the bank to restart the process. Fed official Neel Kashkari said signs of widespread inflation led him to forecast one rate hike this year in his projections earlier this month, with rates expected to remain unchanged in 2027; the Iran war pushed up oil prices, and the May PCE annual rate came in at 4.1%, with prices exceeding the Fed's 2% target for over five years. The US goods trade deficit widened to $105.8 billion in May, the highest in over a year, against expectations of a deficit of $85 billion; exports fell 5.4%, while imports rose 3.6%. Bank of England officials are concerned that record-high temperatures could push up food inflation, with the El Niño phenomenon expected to form later this year through 2027, potentially triggering a new wave of supply shocks.

This week, the market will focus on multiple data points, including the Eurozone June industrial sentiment index and economic sentiment index, the US Dallas Fed business activity index, China's June official manufacturing PMI, the UK's final Q1 GDP annual rate, France/Germany/Eurozone CPI, US ADP employment data, non-farm payrolls, ISM manufacturing PMI, and unemployment rate. Additionally, several central bank officials will speak this week, including Fed Chair Warsh, ECB President Lagarde, BOE Governor Bailey, and BOC Governor Macklem at the ECB Forum. Note trading hours: On July 1, the Hong Kong Stock Exchange will be closed for the Hong Kong Special Administrative Region Establishment Day, with southbound and northbound trading suspended; on July 3, the New York Stock Exchange will be closed for Independence Day, with CME precious metals, energy, forex, US Treasury, and equity index futures contracts ending trading early at 01:00 Beijing time on July 4, and ICE Brent crude oil futures contracts ending trading early at 01:30 Beijing time on July 4.

In the crude oil market, international oil prices fell overnight, with WTI crude futures down 2.34% and Brent crude down 2.52%; both posted a third consecutive weekly decline, with WTI down 7.4% for the week and Brent down 8.06% for the week. Brent spot crude prices fell back to pre-war levels, with near-month contracts showing a contango structure for seven consecutive days. Tariq Zahir, a managing member of Tyche Capital Advisors, said oil prices have fallen too fast and too hard, the ceasefire agreement remains fragile, and the situation in the Strait of Hormuz remains uncertain. Rich Privorotsky, head of Goldman Sachs' One-Delta business, noted that Iran has shown force near the Strait of Hormuz, some cargo ships have changed routes, and inventory backlogs in the Gulf region are gradually flowing into the market, limiting the probability of a significant upside in oil prices in the short term. Baker Hughes data showed that the number of active US oil rigs increased to 440 last week, rising for two consecutive weeks; active natural gas rigs increased to 573, the largest single-week increase since June 2022. A report from the US Energy Information Administration (EIA) showed that US refining capacity decreased by 263,000 barrels per day in 2025, a decline of 1.43%, mainly due to the conversion of a large Houston refinery and the closure of a Los Angeles, California refinery; Marathon Petroleum remained the largest US refiner with a capacity of 2.986 million barrels per day. Iraq's Oil Ministry said OPEC has gradually restored Iraq's pre-war production quota, which will support the recovery of the oil industry. Barclays lowered its Brent crude oil price forecast, cutting its 2026 estimate from $100 per barrel to $96, and its 2027 estimate from $88 to $85, citing the resumption of oil transport through the Strait of Hormuz, with current flows having recovered to about 80% of pre-war levels, though the normalization process is not yet complete.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com