1. Market Definition and Analytical Method

This report uses the term wastewater treatment equipment to cover the mechanical, biological, chemical, membrane, thermal, electrical and digital systems required to collect, treat, reuse and manage municipal and industrial wastewater. It includes complete packaged plants as well as process units and components used in larger plants.

1.1 Equipment and service scope

- Pre-treatment and headworks: screens, grit removal, oil-water separation, equalization, dissolved air flotation and primary clarification.

- Biological treatment: activated sludge systems, sequencing batch reactors (SBR), moving bed biofilm reactors (MBBR), membrane bioreactors (MBR), anaerobic treatment and nutrient-removal processes.

- Tertiary treatment and reuse: filtration, ultrafiltration, reverse osmosis, ultraviolet disinfection, ozonation, activated carbon, advanced oxidation and brine/concentrate management.

- Sludge and resource recovery: thickening, centrifuges, belt presses, filter presses, digestion, biogas systems, drying and nutrient recovery.

- Core components: pumps, blowers, diffusers, mixers, valves, membranes, dosing systems, analyzers, sensors, drives and electrical control panels.

- Digital and lifecycle services: SCADA, process optimization, remote monitoring, spare parts, operator training, commissioning, maintenance and performance-based O&M.

1.2 Why this report does not rely on a single global market-size estimate

Public estimates for the global wastewater-treatment-equipment market vary widely because some include civil construction, chemicals, engineering, membranes, sludge systems or operating services, while others count only equipment sales. Reliable public data are insufficient to determine one exact, globally comparable equipment-market value. This report therefore uses traceable demand indicators: treatment gaps, public investment programs, regulatory deadlines, reuse targets, official project pipelines and procurement structures. Commercial market estimates should be treated as directional unless their definitions and data sources are disclosed.

2. Global Demand: The Opportunity Is a Treatment and Reuse Gap

2.1 Basic treatment remains incomplete

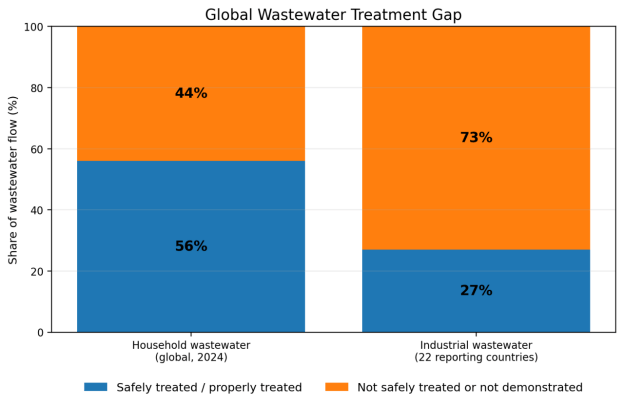

UN-Water's 2025 briefing estimates that 56% of household wastewater flows were safely treated in 2024. The remaining 44% represents both an infrastructure deficit and an operating-performance deficit. In some markets, the priority is sewerage and basic secondary treatment; in others, the need is rehabilitation, nutrient removal, disinfection, micropollutant control and reliable reuse quality. Industrial wastewater data are much weaker: the 2024 UN-Water update reported that only 27% of industrial wastewater was safely treated in the 22 countries providing data, and cautioned that these countries represented only 8% of the global population.

Figure 1. Global wastewater treatment gap

Source: UN-Water, Progress on Wastewater Treatment 2024 Update; UN-Water 2025 domestic wastewater briefing. Industrial data cover only 22 reporting countries and should not be interpreted as a global estimate.

2.2 Water reuse is becoming a core infrastructure category

UN-Water reports an untapped wastewater reuse potential of around 320 billion cubic metres per year, more than ten times current global desalination capacity. The World Bank's 2025 Scaling Water Reuse report argues that the strongest business cases occur where treated wastewater is close to large users, particularly urban centres and industrial parks. This favours projects that combine municipal effluent with industrial, district-cooling, landscaping, agricultural or aquifer-recharge off-takers.

For equipment suppliers, reuse projects expand the addressable scope from biological treatment to tertiary filtration, membranes, disinfection, advanced oxidation, high-recovery systems, water-quality instrumentation, distribution pumping and continuous compliance monitoring. They also create demand for contractual performance guarantees because the product is no longer simply discharged effluent; it is a substitute water supply with a defined quality and reliability requirement.

2.3 Replacement and upgrading can be more valuable than greenfield construction

In mature markets, the largest capital expenditure is often the replacement of aging assets, improvement of energy efficiency, control of nutrients and emerging contaminants, adaptation to storm flows, and digitization of existing treatment plants. These projects are technically demanding because new equipment must fit constrained sites and interface with legacy controls. They favour suppliers with retrofit engineering, modular skids, detailed process modelling and experienced commissioning teams.

3. What Is Changing in Procurement and Technology

From discharge compliance to fit-for-purpose water

Municipal and industrial buyers are increasingly specifying water quality for a particular end use. This strengthens demand for multi-barrier treatment and online monitoring.

From peak equipment efficiency to whole-plant energy intensity

Aeration, pumping and sludge handling are major operating-cost drivers. Buyers increasingly compare kWh per cubic metre, turndown performance and control logic rather than nominal motor efficiency.

From equipment warranty to process guarantee

Larger projects require guaranteed effluent quality, throughput, availability, energy use and chemical consumption. Suppliers must clearly define influent assumptions and exclusions.

From centralized plants to hybrid networks

Fast-growing cities and industrial zones often combine large centralized plants with decentralized or modular systems. Packaged MBBR, SBR and MBR solutions are gaining relevance where sewer networks lag urban development.

From sludge disposal to resource recovery

Anaerobic digestion, biogas, thermal drying, phosphorus recovery and reuse of treated biosolids can improve economics and reduce disposal risk, but require locally viable off-take and regulation.

From manual operation to data-assisted O&M

Online analyzers, remote alarms, predictive maintenance and process optimization are increasingly necessary where utilities face operator shortages or strict performance contracts.

4. Regional Market Opportunities

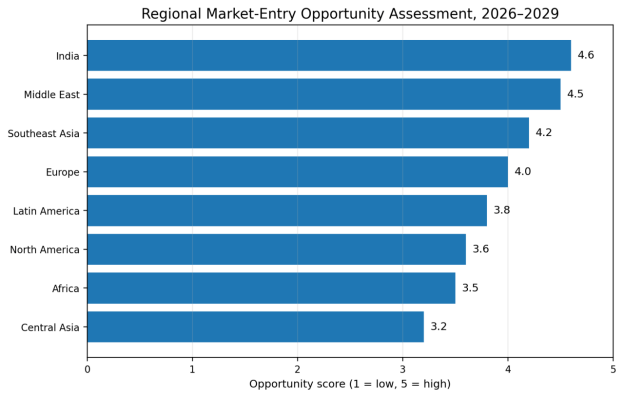

Regional opportunity scores in this report are qualitative analyst assessments rather than statistical market shares. They combine demand visibility, suitability for internationally supplied equipment, project accessibility, payment/financing conditions, localization barriers and service requirements.

Figure 2. Regional market-entry opportunity assessment

Source: Author assessment based on official investment programs, regulatory changes, water-stress conditions, multilateral development bank project activity and procurement barriers. Scores are directional, not market-size estimates.

4.1 Regional opportunity summary

|

Region |

Level |

Demand drivers |

Suitable offerings |

Preferred entry mode |

Key barriers |

|

India |

High |

Municipal capacity expansion, reuse, industrial parks, river-pollution programs |

SBR/MBBR/MBR, tertiary reuse, sludge dewatering, pumps/blowers, packaged plants |

Local EPC/DBO partner; local assembly for volume products |

Price pressure, tender qualification, payment timing, O&M capability |

|

Middle East |

High |

Severe scarcity, reuse, industrial and municipal PPP projects |

MBR, UF/RO, advanced disinfection, odor control, sludge systems, digital O&M |

Developer/EPC alliance; performance contract; local service centre |

Bankability, performance guarantees, local content, heat/salinity, long warranty |

|

Southeast Asia |

High–Medium |

Urbanization, industrial effluent, donor-financed sanitation, coastal pollution |

Modular plants, industrial pretreatment, biological systems, dewatering, automation |

Local integrator; ADB/World Bank procurement; industrial-park channels |

Fragmented regulation, land constraints, local service, FX and project delay |

|

Europe |

Medium–High |

Regulatory upgrades, nutrient and micropollutant removal, energy neutrality |

Advanced treatment, process controls, aeration upgrades, sludge/resource recovery |

OEM supply or local systems partner; CE-compliant local entity |

CE/EN compliance, references, lifecycle performance, competition, producer-responsibility rules |

|

Latin America |

Medium–High |

Urban sanitation backlog, circular economy, reuse in water-stressed cities |

Large municipal process equipment, reuse, sludge systems, automation |

Local EPC; IDB/World Bank projects; Spanish/Portuguese support |

Municipal credit, FX, political cycles, customs and maintenance funding |

|

North America |

Medium |

Aging assets, resilience, PFAS/emerging contaminants, energy upgrades |

Specialist components, controls, advanced treatment, retrofit systems |

OEM/private-label, local certification, distributor or acquisition |

Domestic content, UL/CSA/NSF, licensed engineering, litigation and warranty exposure |

|

Africa |

Medium |

Basic sanitation gaps, fecal sludge management, urban growth, donor finance |

Low-OPEX modular plants, fecal sludge systems, solar-compatible equipment, dewatering |

IFI tenders, local contractor, containerized systems, training-heavy model |

Payment and funding continuity, operator capacity, spares, logistics and security |

|

Central Asia |

Medium |

Municipal rehabilitation, mining and industrial wastewater, water scarcity |

Robust biological systems, dewatering, pumps, automation, cold-climate packages |

Local distributor/EPC; development-bank projects; regional service hub |

Public procurement, language, winterization, FX, import logistics |

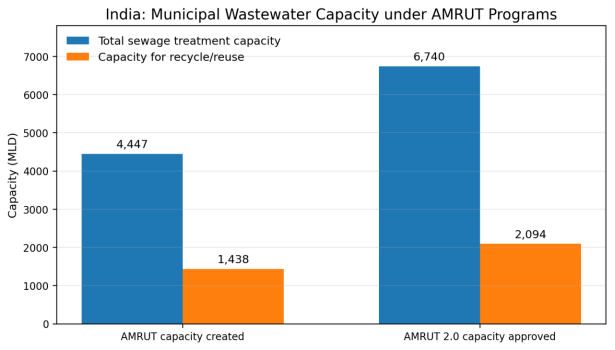

4.2 India: scale, reuse and project fragmentation

India offers one of the clearest near-term municipal project pipelines. In March 2025, the Ministry of Housing and Urban Affairs reported that 592 sewerage and septage projects worth INR 676.08 billion had been approved under AMRUT 2.0. These projects cover 6,739.92 MLD of new or augmented sewage-treatment capacity, including 2,093.96 MLD for recycle and reuse. Under the earlier AMRUT program, 4,447.11 MLD of capacity had been created, including 1,437.56 MLD for reuse.

The opportunity is distributed across numerous state and municipal authorities, which means a supplier needs bid intelligence, local technical documentation and a reliable EPC or O&M partner. Price competition is intense, but the lowest capital price does not always win when tenders include energy consumption, guaranteed outlet quality, multi-year operation or reuse requirements. Process packages that reduce civil works and commissioning risk can be differentiated.

Best-fit offerings include SBR and MBBR packages, MBR for reuse-constrained sites, tertiary filtration and disinfection, sludge dewatering, energy-efficient blowers, pumps, diffusers, online analyzers and packaged systems for smaller cities or institutions. The recommended entry model is local EPC integration first, followed by assembly or localized fabrication for tanks, skids and control panels once repeat orders justify it.

Figure 3. India wastewater capacity and reuse pipeline

Source: Government of India, Ministry of Housing and Urban Affairs / Press Information Bureau, 27 March 2025.

4.3 Middle East: reuse, performance and PPP procurement

The Middle East and North Africa had average annual water availability of only 480 cubic metres per person in 2023, less than 10% of the global average, according to the World Bank. Water scarcity makes treated wastewater a strategic supply rather than solely an environmental service.

Gulf markets are attractive for advanced municipal reuse, industrial water recycling, district cooling, landscaping and large PPP-style treatment plants. Buyers typically expect robust operation under high temperatures, salinity, variable influent and strict odor-control requirements. This supports demand for MBR, tertiary filtration, UF/RO, UV or ozone, advanced controls, sludge treatment and long-term O&M.

The commercial barrier is not demand but bankability. International developers and lenders require proven references, defined process guarantees, liquidated-damage exposure, spare-parts plans and long warranties. A new entrant should work through a prequalified developer, EPC contractor or local water company rather than bid as an equipment-only supplier. Local content and in-country service response should be planned before tender submission.

4.4 Southeast Asia: decentralized growth and industrial compliance

Southeast Asian demand is heterogeneous. Major cities need sewerage networks and central plants, while industrial parks, tourism zones, hospitals and peri-urban developments often need decentralized systems. ADB has identified wastewater management as a major regional priority and supports projects that expand urban wastewater services, including investments in Indonesian cities and other regional programs.

The strongest product-market fit is for compact modular biological systems, industrial pretreatment, dissolved air flotation, nutrient removal, sludge dewatering, pumping and monitoring. In electronics, food processing, palm oil, textiles and chemicals, industrial buyers may move faster than municipal utilities because export customers and local regulators require compliance.

Market entry requires country-specific local partners. A single Southeast Asia distributor is rarely sufficient because standards, languages, procurement and service networks differ. Suppliers should build two channels: local EPC/integrator relationships for municipal and developer projects, and sector-specific industrial partners for recurring equipment and service demand.

4.5 Europe: high-value upgrades under tighter rules

Directive (EU) 2024/3019 recasts the Urban Wastewater Treatment Directive and will replace the previous directive from 1 August 2027. It extends collection and treatment requirements to agglomerations above 1,000 population equivalent, with relevant deadlines beginning in 2035. It also strengthens water reuse, energy-neutrality and micropollutant-related obligations.

This creates opportunities in advanced nutrient removal, quaternary treatment, ozone, activated carbon, membranes, aeration optimization, online monitoring, energy recovery and sludge treatment. However, European utilities buy on demonstrated lifecycle performance, safety compliance and references. Low-price equipment without local engineering or certification is unlikely to penetrate critical process applications.

The most realistic routes are component supply to established OEMs, specialist technology partnerships, acquisition of a local integrator, or a regional service subsidiary. CE marking and relevant EN/IEC requirements are baseline expectations, but process references, cybersecurity, environmental documentation and service response determine commercial credibility.

4.6 North America: replacement and specialist technology

The US Clean Water State Revolving Fund has provided USD 181.4 billion through about 51,000 low-cost loans for water-quality infrastructure. The program finances municipal wastewater facilities, decentralized treatment, stormwater, water reuse and related projects.

The best opportunities for foreign suppliers are specialist components, private-label/OEM products, retrofit packages, membranes, analyzers, controls, energy-efficient aeration and emerging-contaminant treatment. Direct participation in public projects can be constrained by domestic-content requirements, approved-product lists, professional-engineering rules and strict liability expectations.

A credible entry strategy normally requires a local legal entity or distributor, North American product certification where applicable, inventory for critical spares, and local commissioning. Suppliers should avoid providing process guarantees until influent data, pilot requirements, contractual damages and insurance obligations have been independently reviewed.

4.7 Latin America: urban infrastructure and circular-economy projects

Latin American opportunities combine large-city sanitation programs with reuse and resource-recovery projects. In 2025, the World Bank approved a USD 200 million program for Peru to upgrade water and sanitation systems and support water reuse, aquifer recharge, energy cogeneration and nutrient recovery. The IDB has also approved sanitation financing in Brazil and supports circular-economy approaches across the region.

Large municipal projects can create demand for headworks, aeration, clarifiers, sludge dewatering, automation and tertiary treatment. Industrial reuse is attractive in mining, petrochemicals, food and beverage, pulp and paper, and water-stressed metropolitan regions. Brazil's Aquapolo project demonstrates the role of long-term industrial off-take in making reuse bankable.

Entry should be country-specific and language-ready. Spanish or Portuguese technical documentation, local electrical standards, customs planning and spare-parts support are essential. Credit and foreign-exchange risk should be separated from technical risk through confirmed letters of credit, multilateral-financed procurement or strong EPC counterparties.

4.8 Africa: basic sanitation, fecal sludge and low-OPEX systems

Africa has significant unmet sanitation and wastewater needs, but many projects are constrained by collection networks, utility finances and operating capacity. The African Water Facility and African Development Bank are supporting urban sanitation initiatives and wastewater projects that emphasize resource reuse, fecal sludge management and project preparation.

The most scalable offerings are not always conventional large activated-sludge plants. Containerized or modular systems, ponds and biofilm hybrids, fecal-sludge receiving and treatment, solar-compatible pumping, robust dewatering and simple remote monitoring may provide better lifecycle performance. Equipment must tolerate voltage instability, dust, heat, limited chemical supply and delayed spare-parts logistics.

A supplier should prioritize externally financed projects, strong private industrial customers and cities with committed O&M funding. Training, simplified maintenance, initial spare-parts kits and remote support should be priced into the contract rather than treated as optional extras.

4.9 Central Asia: rehabilitation and industrial niches

Central Asian markets offer municipal rehabilitation and industrial-water opportunities associated with mining, metallurgy, oil and gas, food processing and urban expansion. Development-bank procurement can improve transparency, but project cycles are long and documentation may be required in Russian and local languages.

Cold-climate design, freeze protection, robust pumps and blowers, sludge handling and automation are relevant. The recommended model is a regional distributor or EPC partner supported by a service hub and standardized winterization packages. Suppliers should verify sanctions, banking routes and end-user compliance before accepting orders.

5. Product and Supply-Chain Opportunities

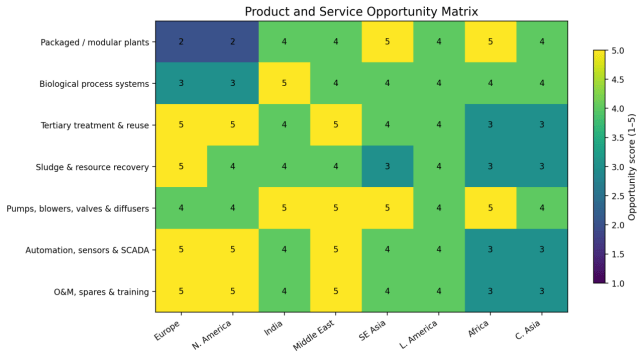

International opportunity is distributed across the treatment train. Complete plant exports are only one segment and often carry the highest project and guarantee risk. Components, modular process units, software, replacement parts and operating services can produce faster market entry and more repeatable revenue.

Figure 4. Product and service opportunity matrix

Source: Author assessment. Scores reflect demand visibility, product-market fit and accessibility for international suppliers; they are not market shares.

|

Segment |

Opportunity |

Demand rationale |

Best-fit applications |

Entry model |

Critical risk |

|

Packaged / modular plants |

High in emerging markets |

Fast deployment, limited civil works, repeatable design |

Industrial parks, hotels, hospitals, small cities, camps |

Local tanks/skids; retain process design and controls |

Influent variability, operator skill, limited redundancy |

|

Biological process systems |

High |

Core of municipal and industrial treatment |

SBR, MBBR, MBR, anaerobic and nutrient removal |

Process package + local civil/EPC |

Process guarantee and seasonal performance |

|

Tertiary treatment and reuse |

High and rising |

Reuse, micropollutants, high-quality discharge |

UF, RO, UV, ozone, carbon, AOP |

Partner with reuse off-taker and local integrator |

Fouling, concentrate disposal, energy and chemical cost |

|

Sludge and resource recovery |

Medium–High |

Disposal cost, energy recovery, circular economy |

Centrifuges, presses, digestion, drying, phosphorus recovery |

Equipment + service + off-take feasibility |

Feed variability, odor, biosolids regulation, revenue uncertainty |

|

Pumps, blowers, valves, diffusers |

High, recurring |

Replacement demand and plant energy optimization |

Municipal and industrial plants of all sizes |

Distributor/OEM/private label; local inventory |

Commodity price pressure and approved-vendor lists |

|

Automation, sensors and SCADA |

High in mature and premium markets |

Compliance, operator shortages, performance contracts |

Online analyzers, controls, remote optimization |

Local systems integrator and cybersecurity compliance |

Calibration, data integration and support continuity |

|

O&M, spares and training |

Strategically critical |

Protects performance and creates recurring revenue |

All project types |

Local technicians, remote support, service-level agreement |

Underpricing service obligations and response-time penalties |

5.1 Best opportunities for large suppliers

Large suppliers are better positioned for complete process packages, advanced reuse systems, sludge-resource-recovery lines, EPC/DBO alliances and long-term O&M. Their advantages are reference projects, bonding capacity, process guarantees, international insurance and the ability to support multi-country service networks.

5.2 Best opportunities for small and mid-sized suppliers

Small and mid-sized suppliers should focus on differentiated components or repeatable modules rather than competing for complete municipal plants. Attractive niches include high-efficiency blowers, diffusers, dosing skids, analyzers, compact DAF units, containerized biological systems, specialized membranes, dewatering equipment, odor control, remote monitoring and replacement parts. OEM/private-label arrangements can reduce certification and channel costs.

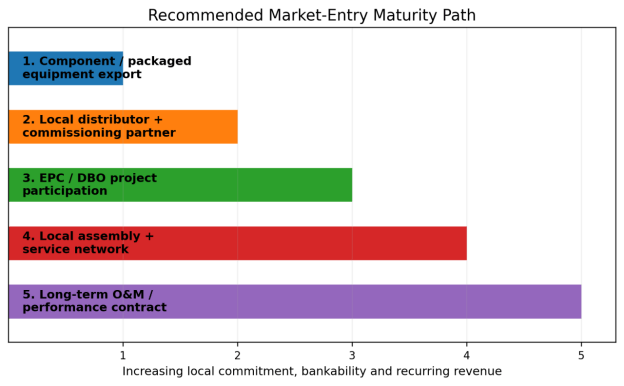

6. Project-Based Delivery and Market-Entry Pathways

Figure 5. Recommended market-entry maturity path

Source: Author framework based on typical international wastewater project structures.

|

Entry mode |

Best fit |

Advantages |

Main exposure |

Recommended use |

|

Direct equipment export |

Standard components, replacements, simple packaged units |

Fast, low fixed cost |

Low control over installation and service |

Stable industrial buyers; distributor-supported markets |

|

Distributor / integrator |

Components and modular systems |

Local access, qualification and service |

Margin sharing and partner dependence |

Fragmented emerging markets and retrofit sales |

|

OEM / ODM supply |

Pumps, blowers, valves, skids, controls, specialist modules |

Uses established brand and channel |

Lower brand visibility; technical IP management |

North America, Europe and global OEM platforms |

|

EPC partnership |

Process packages and major equipment lines |

Access to larger municipal/industrial projects |

Interface and guarantee risk |

India, Middle East, Southeast Asia, Latin America |

|

DBO / performance contract |

Complete treatment and long-term service |

Recurring revenue and stronger customer lock-in |

High working capital, performance and payment risk |

PPP/utility markets with bankable off-take |

|

Local assembly / manufacturing |

Volume equipment and repeatable skids |

Local content, shorter delivery, customs savings |

Fixed cost and quality-control burden |

Markets with repeat pipeline and localization rules |

6.1 How to move from selling equipment to participating in projects

- Develop a standardized technical offer with clear influent ranges, process assumptions, guaranteed outputs, energy estimates and exclusions.

- Build local commissioning capability before promising process performance. The installation and operator interface are part of the product.

- Use pilot units or reference plants to validate local wastewater characteristics, temperature, salinity, fouling and operator practices.

- Create a bid library: drawings, P&IDs, control philosophy, material certificates, welding records, quality plan, factory acceptance test procedures and spare-parts lists.

- Separate equipment scope, process guarantee and long-term O&M risk in contracts. Each risk should be priced and assigned to the party able to control it.

- Offer service-level agreements with defined response times, remote support and critical-spares availability. Recurring service should not be bundled at zero price.

- Use export credit insurance, confirmed letters of credit, parent guarantees or multilateral procurement to reduce payment risk on public projects.

7. Standards, Certification and Localization

Wastewater treatment equipment is not governed by one universal certification. Requirements depend on the component, pressure rating, electrical system, hazardous-area classification, drinking-water contact, discharge permit and public procurement rules. Suppliers should create a market-specific compliance matrix rather than attach every available certificate to every proposal.

|

Market |

Typical requirements |

Documentation / qualification |

Localization implication |

|

European Union |

CE marking; Machinery Regulation/Directive as applicable; Low Voltage and EMC; PED for pressure equipment; ATEX for hazardous areas; EN/IEC electrical standards; REACH/RoHS where applicable |

EU Declaration of Conformity, risk assessment, technical file, local language manuals, cybersecurity and environmental documentation |

Local service and references are often more important than nominal compliance alone |

|

United States |

UL/ETL for electrical panels where required; NSF/ANSI for relevant water-contact products; ASME for pressure vessels; NEMA; local electrical and building codes |

Approved submittals, professional engineering, domestic-content review, insurance and product liability |

Use local OEM/distributor and verify Build America, Buy America or state-specific rules |

|

Canada |

CSA or equivalent electrical certification; provincial requirements; ASME/CRN for pressure equipment where applicable |

Bilingual or local documentation depending on province; local engineering review |

Local certification planning should begin before shipment |

|

India |

BIS and Central/State Pollution Control Board requirements where applicable; tender-specific standards; local electrical and civil codes |

Tender qualification, performance references, local testing, GST/customs and service obligations |

Local fabrication and EPC partnership improve competitiveness |

|

GCC / Middle East |

Local utility and environmental authority specifications; IEC; SASO/SABER in Saudi Arabia for applicable products; hazardous-area and pressure-equipment requirements |

Arabic/English documentation, local registration, vendor prequalification, performance bonds |

Local content and in-country service are increasingly important |

|

Southeast Asia |

Country-specific electrical, environmental and import rules; IEC-based standards common but not uniform |

Local language manuals, authority approvals, industrial-estate standards |

Country-by-country partner and compliance review required |

|

Latin America |

National electrical and safety rules; IEC/ISO references; local environmental permits; pressure and hazardous-area rules |

Spanish/Portuguese documentation, customs classification, tax and local engineering |

Local importer of record and spare-parts plan are essential |

|

Africa / Central Asia |

Tender- and donor-specific standards; IEC/ISO frequently referenced; national environmental permits |

IFI procurement documents, local language, climatic design and training |

Robustness and maintainability should be documented as compliance attributes |

7.1 Localization should be selective

Localization does not always mean building a factory. It can begin with local commissioning, local-language documentation, regional spare-parts inventory, licensed control-panel fabrication, local skid and tank assembly, and training of service technicians. High-value process design, membranes, proprietary media, critical rotating equipment and software can remain centralized until volumes justify deeper localization.

8. Commercial Model, Pricing Logic and Bankability

8.1 Buyers evaluate total cost of ownership

Capital cost remains important, especially in price-sensitive tenders, but the most bankable offers quantify lifecycle performance. A credible proposal should state expected energy use, chemical consumption, sludge production, membrane or media replacement intervals, operator requirements, maintenance hours, critical-spares cost and availability. These assumptions should be linked to influent conditions and clearly separated from customer-controlled factors.

8.2 Performance guarantees need disciplined boundaries

- Influent flow, pollutant load, temperature, pH, salinity, toxic shocks and peak hydraulic conditions.

- Required effluent parameters and sampling protocol, including average, maximum and percentile values.

- Availability guarantee and exclusions for upstream failure, utility interruption or unauthorized operation.

- Energy and chemical guarantees, including the electricity tariff and chemical quality assumptions.

- Commissioning duration, biological seeding, ramp-up conditions and acceptance-test period.

- Liquidated damages, liability cap, warranty period and responsibility for civil, electrical and control interfaces.

8.3 Bankable project structures

The strongest reuse projects have a clear off-taker for recycled water and a tariff or payment mechanism that supports O&M. Municipal projects are more bankable when funding, land, sewer connections, influent supply and discharge permissions are secured before equipment procurement. Industrial projects are more bankable when the customer can compare reuse cost with freshwater, discharge fees and production risk. Suppliers should not accept performance exposure for missing networks, unstable inflow or unapproved reuse off-take.

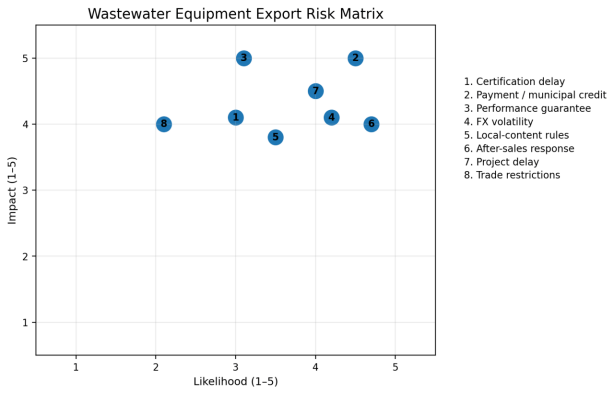

9. Risk Analysis and Mitigation

Figure 6. Wastewater equipment export risk matrix

Source: Author assessment. Likelihood and impact vary by country, customer and contract.

|

Risk |

How it appears |

Mitigation action |

Priority |

|

Process-performance risk |

Influent is outside design range; effluent guarantee fails |

Pilot testing, verified data, dynamic design range, exclusions and staged acceptance |

High |

|

Payment and municipal credit |

Delayed certification, budget interruption, weak utility finances |

LC, escrow, sovereign/parent guarantee, export credit insurance, milestone payments |

High |

|

Certification / approval delay |

Equipment cannot be energized, imported or accepted |

Pre-bid compliance matrix, local certification partner, sample review, schedule contingency |

High in mature markets |

|

Localization / origin rules |

Bid loses preference or funding eligibility |

Local assembly, compliant bill of materials, origin documentation, local supplier mapping |

Medium–High |

|

FX and inflation |

Margin erosion on long project cycle |

Currency matching, escalation clause, hedging, shorter quotation validity |

High in emerging markets |

|

Logistics and site interface |

Oversized equipment delay; civil/electrical mismatch |

3D interface review, shipment split, Incoterms clarity, site survey, local fabrication |

Medium–High |

|

After-sales and spare parts |

Plant downtime and warranty claims |

Critical-spares stock, SLA, remote diagnostics, trained local technicians |

High |

|

Policy and political change |

Tender cancellation, tariff or reuse-policy change |

Diversified pipeline, multilateral financing, termination compensation, compliance review |

Medium–High |

|

Trade controls and sanctions |

Banking or shipment becomes prohibited |

End-user screening, sanctions clauses, export-control review, alternative payment routes |

Market-specific |

|

Cybersecurity and data |

Remote system rejected or compromised |

Network segmentation, role-based access, secure updates, local data rules |

Rising |

10. Three-Year Market-Entry Roadmap

Phase 1: Market selection and offer standardization (0–6 months)

- Select two priority markets and one secondary market based on demand, access, payment and product fit; do not launch across eight regions simultaneously.

- Create market-specific compliance matrices, target-customer lists, tender calendars and partner due-diligence criteria.

- Standardize three export offers: a component/OEM range, a packaged modular system, and a process package for EPC integration.

- Prepare English and local-language technical submittals, reference sheets, process guarantees, commissioning plans and lifecycle-cost calculators.

Phase 2: References, channels and service capability (6–18 months)

- Appoint partners only after technical and financial due diligence; use performance-based territory rights rather than unconditional exclusivity.

- Secure two to four reference installations in target segments and collect operating data suitable for future bids.

- Train local technicians, establish remote monitoring and stock critical spare parts.

- Register with major EPC contractors, utilities, industrial parks and development-bank procurement systems.

Phase 3: Project participation and selective localization (18–36 months)

- Join EPC/DBO bids where the process package is differentiated and contractual interfaces are manageable.

- Localize control panels, skids, tanks or non-proprietary fabrication when it improves tender eligibility and delivery time.

- Introduce multi-year O&M, performance optimization and replacement-parts agreements.

- Consider a regional service hub, joint venture or acquisition only after the opportunity pipeline supports recurring utilization.

Conclusion

Wastewater treatment equipment has a durable global opportunity, but the opportunity is not uniform and should not be reduced to a headline growth rate. Basic treatment deficits create volume demand in India, Southeast Asia, Africa and parts of Latin America. Water scarcity creates premium reuse demand in the Middle East and selected industrial regions. Regulatory upgrades create high-value technology demand in Europe and North America. Across all markets, the commercial centre of gravity is moving from equipment supply toward guaranteed treatment performance, lifecycle cost and local service.

The most successful international suppliers will be those that choose markets according to product fit, enter through manageable modules or components, build local references, and progressively take on project and operating responsibility. A low factory price may open a conversation, but it will not by itself produce a bankable wastewater project. The decisive capabilities are process credibility, contract discipline, compliance, commissioning, data transparency, spare-parts availability and long-term operational support.

For the next three years, India and the Middle East should be considered priority markets for project development; Southeast Asia should be treated as a multi-country portfolio for modular and industrial solutions; Europe and North America should be approached through specialist, OEM and upgrade strategies; and Latin America, Africa and Central Asia should be developed selectively through funded projects and credit-protected counterparties. The practical goal is not to export the greatest number of machines. It is to build a repeatable portfolio of treatment outcomes that customers, EPC partners and financiers can trust.