Executive Summary

Zero liquid discharge is shifting from a compliance-only solution toward a water-security and production-resilience investment, but the economics remain highly site-specific. The market is expanding because industrial operators face tighter discharge limits, greater exposure to water stress and rising costs for freshwater, sewer discharge and off-site brine disposal. However, full ZLD is not automatically the optimal answer. Where a permitted liquid outlet or economical disposal route exists, MLD or selective recovery can deliver most of the water benefit at materially lower energy and capital intensity.

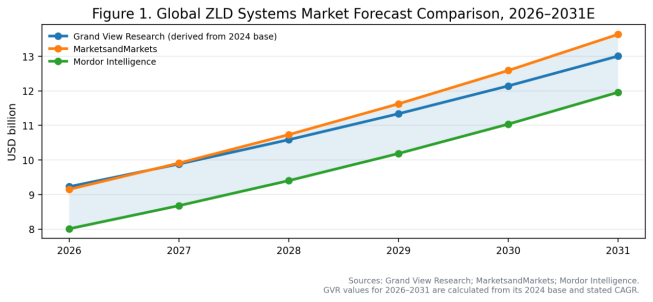

Current public market estimates form a relatively coherent planning range despite different definitions. Harmonised to 2026, three major research providers imply a global ZLD systems market of roughly USD 8.0–9.2 billion. Their 2031 projections cluster around USD 12.0–13.7 billion, equivalent to a high-single-digit annual growth profile. The most defensible planning assumption is therefore not a single point estimate, but a 2026–2031 base-case CAGR of approximately 7–8.5%.

Asia Pacific and North America are nearly balanced at the top of the market. Grand View Research estimates 2024 revenue of USD 2.89 billion in Asia Pacific and USD 2.62 billion in North America. MarketsandMarkets, using a different segmentation, identifies North America as the leading region with about one-third of revenue. The apparent disagreement is small and reflects methodology: both sources indicate that the two regions together account for roughly two-thirds of global demand.

Thermal equipment remains the largest value pool because evaporation and crystallization perform the final concentration and solids-production steps that define true ZLD. MarketsandMarkets estimates that evaporation/crystallization represented 45.7% of market value in 2025. The fastest technology development, however, is occurring upstream: high-recovery reverse osmosis, electrodialysis, osmotically assisted processes, selective precipitation and better pretreatment are being used to reduce the flow reaching the thermal section.

Energy and fouling risk determine project economics. Moving a feed from conventional treatment to 70–90% recovery is often technically manageable; pushing the remaining concentrate to dry or semi-dry solids is disproportionately more expensive. Research published in Nature Water found ZLD/MLD recoveries spanning 32.6–98.6%, with steep energy and cost trade-offs at the high-recovery end. The commercial objective should therefore be minimum lifecycle cost at the required discharge endpoint—not maximum nominal recovery in isolation.

The most attractive end-use segments are chemicals and petrochemicals, power generation, mining and metals, textiles, semiconductors and selected high-value manufacturing processes. These sectors combine high-salinity streams, regulatory exposure, constrained disposal routes and an economic need for reliable process water. Municipal ZLD remains comparatively limited because conventional discharge and centralized treatment are usually cheaper, except in inland desalination or highly constrained reuse projects.

The competitive market is divided between integrated water companies, thermal-process specialists, membrane and brine-concentration innovators, and regional EPC suppliers. Veolia, Aquatech, GEA, Alfa Laval, Saltworks and other specialists compete on process guarantees, materials selection, anti-scaling strategy, automation, energy integration and reference plants. Long-term service capability is increasingly as important as equipment efficiency because a ZLD plant can become a production bottleneck if feed chemistry or scaling behaviour is mischaracterised.

The strategic conclusion is clear: ZLD demand should continue to rise through 2033, but winning products will not be generic “zero-discharge packages.” The market will reward modular and chemistry-specific designs that minimize thermal load, recover reusable water, manage mixed salts, use waste heat where available and provide verifiable performance across seasonal and production-driven changes in wastewater composition.

1. Scope, Definitions and Methodology

1.1 What is being measured

A ZLD installation is a complete Wastewater Treatment Equipment train designed to recover usable water and convert the remaining dissolved and suspended matter into a non-liquid residue. The train commonly includes equalisation, oil and solids removal, softening or selective precipitation, biological or advanced oxidation treatment where organics are present, membrane pre-concentration, thermal evaporation, crystallisation and solids dewatering.

Market studies differ in whether they count only new capital equipment or also engineering, construction, chemicals, replacement components and long-term service. Some use “conventional ZLD” and “hybrid ZLD” categories; others segment by filtration and evaporation/crystallisation. The report preserves each provider’s published scope and uses ranges rather than forcing unlike definitions into one total.

1.2 Analytical method

- Market size and CAGR are cross-checked across Grand View Research, MarketsandMarkets and Mordor Intelligence. Derived values are explicitly labelled.

- Official sources—including UN-Water, WRI, the U.S. EPA, the European Commission and India’s environment ministry—are used for water stress, wastewater treatment and regulatory context.

- Technology and operating claims are grounded in peer-reviewed literature, government technical reports and supplier documentation. Vendor statements are treated as product evidence, not independent market statistics.

- Forecasts marked 2030E, 2031E or 2033E are estimates. They should be interpreted as scenario ranges rather than observed outcomes.

|

Boundary |

Included in this report |

Excluded or treated separately |

|

ZLD systems |

Pretreatment, membrane concentration, evaporation, crystallisation, solids handling, controls, engineering and service |

Municipal wastewater treatment without a brine or no-discharge requirement |

|

MLD systems |

Included where market sources combine MLD and ZLD, but identified analytically as a lower-recovery endpoint |

Ordinary water reuse systems that continue to discharge a material liquid concentrate |

|

Recovered products |

Water reuse and salts/by-products where technically and commercially realistic |

Unverified claims that mixed salts automatically generate positive revenue |

|

Market value |

Provider-published system-level revenue envelope |

Standalone revenue for every pump, membrane, chemical or vessel used in the train |

2. Global Market Size and Forecast

2.1 A high-single-digit market with a meaningful definition spread

Grand View Research values the market at USD 8.045 billion in 2024 and projects USD 14.848 billion by 2033, a 7.1% CAGR. MarketsandMarkets’ latest public summary projects USD 9.15 billion in 2026 and USD 13.65 billion in 2031, an 8.3% CAGR. Mordor Intelligence estimates USD 8.01 billion in 2026 and USD 11.96 billion by 2031, an 8.34% CAGR. The close growth rates but wider endpoint values indicate that scope—not demand direction—is the main source of disagreement.

Figure 1. Global ZLD Systems Market Forecast Comparison, 2026–2031E

Sources: Grand View Research [1], MarketsandMarkets [2] and Mordor Intelligence [3].

|

Source |

Published base |

Forecast endpoint |

CAGR |

Interpretation |

|

Grand View Research |

USD 8.045bn (2024) |

USD 14.848bn (2033E) |

7.1% |

Broad system market; 2026 and 2031 values in Figure 1 are derived from the stated CAGR. |

|

MarketsandMarkets |

USD 9.15bn (2026) |

USD 13.65bn (2031E) |

8.3% |

Includes process, capacity, application, system and end-use segmentation. |

|

Mordor Intelligence |

USD 8.01bn (2026) |

USD 11.96bn (2031E) |

8.34% |

Highlights hybrid membrane–thermal configurations and APAC industrial growth. |

A reasonable planning envelope is USD 8.0–9.2 billion for 2026 and USD 12.0–13.7 billion for 2031E. The midpoint is useful for strategic planning, but project pipelines should be segmented by industry and region because a single large power, mining or petrochemical installation can materially affect annual equipment orders.

2.2 Where the value sits

MarketsandMarkets estimates that evaporation/crystallisation accounted for 45.7% of market value in 2025. This is consistent with system economics: the thermal section contains high-value heat-transfer equipment, compressors, circulation pumps, vapour bodies, crystallisers, centrifuges or filters, corrosion-resistant metallurgy and process controls. The upstream filtration share is more fragmented across membranes, pretreatment systems and chemical conditioning.

The replacement cycle also differs by component. Membranes, pumps, seals, heat-exchanger surfaces and instrumentation generate recurring aftermarket demand, while the evaporator shell and crystalliser represent long-lived capital assets. Suppliers that can combine design guarantees with service, cleaning optimisation and feed-chemistry management capture more lifecycle value than equipment-only vendors.

3. Structural Demand Drivers

3.1 Water stress is moving reuse from ESG language to production risk

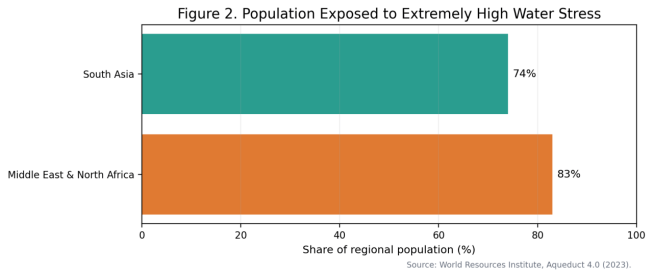

WRI’s Aqueduct 4.0 analysis identifies the Middle East and North Africa and South Asia as the most exposed large regions, with 83% and 74% of their populations respectively living under extremely high water stress. Industrial plants in these regions cannot assume that freshwater supply and discharge capacity will expand in line with manufacturing output. Water recovery therefore becomes part of capacity planning, especially for power, refining, chemicals, mining, textiles and electronics.

Figure 2. Population Exposed to Extremely High Water Stress

Source: World Resources Institute, Aqueduct 4.0 [5].

The strongest business case is created when three conditions overlap: water is expensive or unreliable; liquid discharge is restricted or costly; and the treated water can replace a process-quality intake. ZLD economics are weaker where freshwater is abundant, discharge permits are stable and brine can be disposed of safely at low cost.

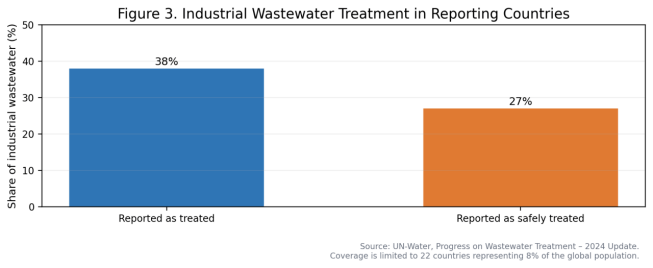

3.2 The industrial wastewater treatment gap remains large

UN-Water’s 2024 update shows that industrial reporting is still extremely limited. Across 22 reporting countries representing only 8% of the global population, 38% of industrial wastewater was reported as treated and 27% as safely treated. This evidence should not be extrapolated into a global market size, but it confirms that the addressable need for better Wastewater Treatment Technology remains substantial.

Figure 3. Industrial Wastewater Treatment in Reporting Countries

Source: UN-Water, Progress on Wastewater Treatment – 2024 Update [4].

ZLD will address only a small portion of this treatment gap because it is a high-intensity endpoint. Most untreated industrial wastewater first requires basic collection, biological treatment or conventional physico-chemical treatment. ZLD becomes relevant after those steps when salinity, toxicity, reuse requirements or disposal constraints make liquid concentrate unacceptable.

3.3 Regulation creates projects, but timing remains jurisdiction-specific

In the United States, the EPA’s 2024 steam-electric rule established zero-discharge requirements for specified coal-power wastewater streams. A December 2025 rule extended certain compliance deadlines to no later than 31 December 2034 without removing the zero-discharge requirements. This extends the project-development window but does not eliminate the underlying treatment need.

In India, ZLD has long been applied in selected textile and tannery clusters, and official filings reference requirements for large-scale textile units. The implementation experience also highlights a central risk: water can be recovered while mixed-salt disposal remains unresolved. A system should therefore not be considered circular merely because liquid discharge has been eliminated.

The European Union is not imposing a universal ZLD mandate. Instead, the revised Industrial Emissions Directive and the 2025 Water Resilience Strategy strengthen pressure on large industrial installations to reduce water demand, improve efficiency and expand reuse. This favours ZLD and MLD in high-risk sites, but European projects will face strict scrutiny of energy consumption and cross-media impacts.

4. Technology Architecture and Process Economics

4.1 ZLD is a sequence of concentration barriers

The central engineering principle is to remove contaminants and recover water at the lowest practical energy level before applying heat. Conventional Reverse Osmosis Technology is highly effective for moderate-salinity streams, but scaling salts, silica, organics and osmotic pressure limit recovery. Advanced membrane concentration, electrodialysis and selective precipitation can extend the non-thermal envelope, reducing the flow sent to evaporation and crystallisation.

|

Stage |

Primary function |

Typical decision variables |

Failure modes |

|

Feed segregation & equalisation |

Prevent incompatible streams from entering one treatment train |

Flow variability, pH, COD, oil, suspended solids, temperature |

Shock loads, unstable chemistry, oversized downstream equipment |

|

Pretreatment / selective removal |

Remove hardness, silica, metals, organics and scale precursors |

Chemical dose, sludge volume, reagent purity, by-product value |

Under-dosing, excess sludge, residual organics, filter plugging |

|

Membrane pre-concentration |

Recover water before thermal treatment |

Feed TDS, osmotic pressure, recovery, membrane compatibility |

Scaling, organic fouling, irreversible compaction, concentrate instability |

|

Brine concentration / evaporation |

Reduce concentrate volume and produce distillate |

Steam/electricity price, MVR efficiency, heat integration, materials |

Scaling, corrosion, foaming, compressor downtime |

|

Crystallisation & solids separation |

Convert dissolved salts to wet cake or dry solids |

Crystal habit, supersaturation, purge rate, mother liquor recycle |

Fine crystals, mixed-salt accumulation, poor dewatering |

|

Water polishing & reuse |

Match recovered water to process specifications |

Conductivity, organics, ammonia, boron, temperature |

Reuse loop contamination, off-spec production water |

4.2 Membrane–thermal hybrids are the main direction of innovation

The commercial value of advanced Water Treatment Membrane Technology is not that it removes the need for thermal treatment in every project. Its value is that each additional cubic metre recovered before the evaporator reduces thermal equipment size and energy use. Osmotically assisted reverse osmosis, low-salt-rejection reverse osmosis, ultra-high-pressure RO, electrodialysis and membrane distillation are being developed for this role.

Recent vendor literature shows the practical direction. Saltworks reports hybrid ultra-high-pressure RO/NF brine concentrations exceeding 200,000 mg/L NaCl in selected applications, compared with roughly 130,000 mg/L for standalone ultra-high-pressure RO. Such claims are feed-specific and require independent pilot validation, but they demonstrate how specialised Membrane Modules are moving closer to the saturation boundary.

Peer-reviewed analysis supports the broader principle but also cautions against universal performance claims. A 2024 Nature Water study found ZLD and MLD recoveries ranging from 32.6% to 98.6%, with increasingly steep energy, land and cost trade-offs. The optimal endpoint depends on ion composition, disposal route, heat source and product-water value.

4.3 Thermal concentration remains the unavoidable core of true ZLD

Mechanical vapour recompression, multi-effect evaporation and forced-circulation crystallisation are the established routes for high-salinity feeds. MVR converts electrical energy into recycled latent heat and is attractive where electricity is available and stable. Multi-effect systems can use low-grade steam or waste heat. Forced-circulation designs tolerate higher solids and scaling risk but require robust pumping and metallurgy.

Thermal selection should be based on the complete heat and mass balance. A low headline specific-energy figure may exclude pretreatment, cooling, solids handling, cleaning and standby operation. Similarly, waste heat is not “free” if its temperature, availability or production schedule does not match the ZLD load.

|

Technology route |

Best-fit feed / site |

Economic advantage |

Main limitation |

|

RO / NF pre-concentration |

Moderate TDS, controlled scaling chemistry |

Lowest-cost water recovery before thermal treatment |

Osmotic pressure, scaling and organics limit recovery |

|

ED / EDR / selective electrodialysis |

Ionic streams with manageable organics and hardness |

Potentially high recovery with selective ion control |

Power use increases with salinity; membrane selectivity and fouling |

|

OARO / LSRRO / UHP-RO hybrids |

High-salinity brines after strong pretreatment |

Reduces evaporator feed and thermal duty |

Higher pressure, process complexity and limited broad reference base |

|

MVR evaporator |

Medium-to-large continuous brine flow |

Recycles latent heat; compact relative to ponds |

Compressor power, scaling, corrosion and turndown |

|

Multi-effect evaporator |

Sites with low-grade steam or waste heat |

Uses thermal integration to reduce utility cost |

Larger footprint and dependence on heat availability |

|

Forced-circulation crystalliser |

Final solids production under high TDS |

Handles slurry and completes true ZLD |

Highest cost/energy section; crystal and mother-liquor management |

|

Evaporation ponds / solar concentration |

Arid sites with land and suitable climate |

Low purchased-energy requirement |

Large land area, weather dependency, seepage and long residence time |

5. End-use Industry Analysis

5.1 The best markets combine regulatory pressure with recoverable water value

Power generation historically created many landmark ZLD installations because cooling-tower blowdown, flue-gas desulfurisation wastewater and ash-related streams can face discharge restrictions. The segment remains material, but the U.S. compliance timetable has shifted and coal retirements complicate project timing. New power demand from data centres and manufacturing may extend plant lives, while water scarcity continues to support reuse investments.

Chemicals and petrochemicals are structurally attractive because plants produce variable high-salinity wastewater, often at sites where production continuity justifies high reliability spending. Mining and metals projects face remote locations, water scarcity and difficult brines containing sulphate, hardness and metals. Textiles and tanneries can have strong regulatory drivers but often struggle with mixed salts and fragmented plant scale.

Semiconductor and electronics manufacturing has high water-quality requirements and strong reuse incentives, but ZLD treatment is only one part of a complex water system. Segregating concentrated fluoride, ammonium, solvents and metal-bearing streams is usually more valuable than routing all wastewater into a single end-of-pipe plant.

|

End-use sector |

Demand intensity (1–5) |

Primary driver |

Commercial judgement |

|

Chemicals & petrochemicals |

5.0 |

High-salinity and variable process effluent; production continuity |

High-value market where feed characterisation and corrosion design determine success. |

|

Power generation |

4.5 |

Zero-discharge rules, cooling water reuse, FGD and ash streams |

Large projects, but regulation and asset-retirement timelines must be assessed plant by plant. |

|

Mining & metals |

4.5 |

Remote water scarcity, mine water and metallurgical brines |

Strong opportunity with difficult logistics and high metallurgy requirements. |

|

Textiles & tanneries |

4.5 |

Cluster regulation, colour/COD control and salt-bearing wastewater |

Large need, but mixed-salt disposal and operator capability can undermine economics. |

|

Semiconductors & electronics |

4.0 |

Ultra-pure-water demand, reuse targets and segregated high-strength streams |

High willingness to pay for reliability; requires specialised chemistry and redundancy. |

|

Pharmaceuticals & specialty chemicals |

3.5 |

Complex organics, solvents and high-value water reuse |

Selective stream treatment often outperforms a single centralized ZLD train. |

|

Food & beverage |

3.0 |

Water reuse and discharge fees |

Organic load usually requires biological treatment; ZLD applies mainly to saline side streams. |

|

Municipal / inland desalination |

2.5 |

No economical brine outlet |

Technically important but cost-sensitive; MLD or regional brine management may be preferable. |

The ratings are an analyst assessment of project intensity, not market shares. High scores reflect the probability that disposal constraints and water value can support ZLD economics; they do not imply that every plant in the sector requires zero liquid discharge.

6. Regional Market Outlook

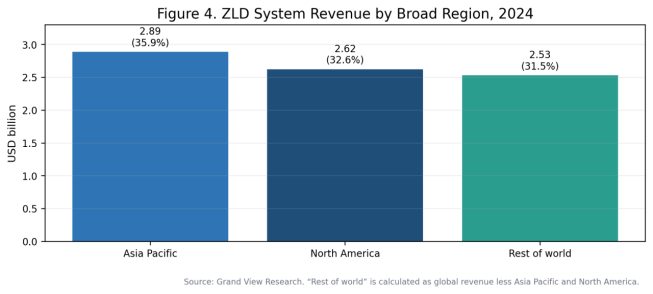

6.1 Asia Pacific and North America form the core market

Figure 4. ZLD System Revenue by Broad Region, 2024

Source: Grand View Research [1].

Grand View Research places Asia Pacific slightly ahead of North America in 2024, while MarketsandMarkets places North America first at 32.4% in 2024/2025 depending on the public summary. The difference is within a narrow band. Strategically, Asia Pacific offers the larger industrial expansion pipeline, while North America offers high project values, mature engineering ecosystems and strong mining, power and resource-processing demand.

|

Region |

Demand drivers |

Constraints |

2026–2033 outlook |

|

Asia Pacific |

Industrial expansion, textile and electronics manufacturing, water stress, local discharge restrictions |

Wide variation in enforcement, power cost and operator capability |

Largest volume opportunity; strongest growth in high-recovery hybrid systems and modular industrial plants. |

|

North America |

Power ELGs, mining, oil & gas, inland desalination, high disposal costs |

EPA deadlines extended; permitting and project cycles can be long |

Large replacement and retrofit market; demand remains strong but timing is uneven. |

|

Europe |

IED 2.0, water resilience, chemicals, mining and circular-resource policies |

High electricity prices and strict cross-media assessment |

Selective ZLD/MLD adoption focused on water efficiency, reuse and resource recovery. |

|

Middle East & North Africa |

Extreme water stress, desalination brine, refining, petrochemicals and mining |

High salinity, difficult disposal and dependence on project finance |

High strategic need; strongest economics where waste heat and recovered water have clear value. |

|

Latin America |

Copper/lithium mining, pulp & paper, drought-exposed industrial corridors |

Remote sites, grid constraints and political/permitting risk |

Project-led opportunity concentrated in mining countries and water-stressed basins. |

|

Africa |

Mining, industrial parks and limited discharge infrastructure |

Financing, service networks, power reliability and spare-parts access |

Smaller near-term market; modular systems and lifecycle service are critical. |

6.2 Resource recovery will be regional and chemistry-specific

Recovered sodium chloride, sodium sulphate, gypsum, lithium or other minerals can improve project economics, but only when purity, scale and local offtake justify additional separation. Mixed salts commonly fail product specifications and remain a disposal liability. Regional market assessments should therefore distinguish “salt production” from “solidification for disposal.”

7. Competitive Landscape

7.1 Competition is based on integration and risk transfer

Integrated water companies compete for turnkey projects and long-term service contracts. Thermal-process specialists sell evaporation, crystallisation and solids-recovery expertise. Membrane innovators seek to lower the thermal duty, while regional EPC firms compete on fabrication, local procurement and price. The most defensible advantage is a reference base on chemically similar feeds—not a generic claim of high recovery.

|

Company / group |

Positioning |

Relevant capabilities |

Competitive observation |

|

Veolia Water Technologies / HPD |

Integrated global water and thermal-process supplier |

HPD evaporation/crystallisation, OPUS pretreatment, large power and petrochemical references |

Strong bankability and reference plants; premium engineering and long project cycles. |

|

Aquatech |

Industrial water and ZLD specialist |

Integrated membrane, evaporation and crystallisation systems; power, refining and industrial reuse |

Strong project integration; competes on performance guarantees and complex feeds. |

|

GEA |

Thermal separation and process equipment specialist |

MVR/falling-film evaporation, crystallisation, solids separation and custom metallurgy |

Strong process engineering and fabrication; often integrated into broader EPC trains. |

|

Alfa Laval |

Heat-transfer and separation equipment supplier |

Evaporation, heat exchangers, decanters and industrial process integration |

Benefits from installed base and energy-integration expertise. |

|

Saltworks Technologies |

Modular brine-management specialist |

UHP RO/NF, modular MVR and multi-effect evaporator-crystallisers, automation |

Differentiated modular approach; application envelope should be validated by pilot testing. |

|

Gradiant and advanced-membrane specialists |

High-recovery membrane and digital-water positioning |

Counterflow RO, selective separations, AI-enabled operations and reuse systems |

Potential to reduce thermal load; long-term durability and reference depth remain key diligence items. |

|

Regional EPC and equipment manufacturers |

Price and local delivery competitiveness |

Pretreatment, RO skids, evaporators, crystallisers, tanks, piping and civil works |

Can be highly competitive where local service is strong; quality and process guarantee vary widely. |

7.2 The equipment opportunity is wider than the plant integrator market

Specialised opportunities exist in high-pressure pumps, corrosion-resistant alloys, heat exchangers, anti-scalants, cleaning systems, online ion analysis, conductivity and TOC monitoring, centrifuges, filter presses and automation. Equipment suppliers should position products around validated operating windows and serviceability rather than simply labelling them “ZLD compatible.”

8. Procurement and Total Cost of Ownership

8.1 Feed chemistry is the first commercial specification

The most common procurement error is to define capacity only in cubic metres per day. Two streams with the same flow can require entirely different systems if their chloride, sulphate, calcium, silica, COD, ammonia, solvents, oils or temperature differ. A representative sampling campaign across production cycles is more valuable than an early vendor price.

|

Cost / risk driver |

Effect on CAPEX or OPEX |

Required diligence |

|

Thermal feed flow |

Directly drives evaporator and crystalliser size and energy use |

Maximise economical pre-concentration; compare mass flow, not only water recovery. |

|

Scaling chemistry |

Reduces heat transfer, membrane flux and plant availability |

Speciation modelling, pilot testing, cleaning strategy and redundancy. |

|

Corrosion and metallurgy |

Can dominate equipment cost and lifecycle failure risk |

Chloride/temperature envelope, pH, oxygen, alloy selection and weld quality. |

|

Energy price and source |

Determines MVR electricity cost or steam-based OPEX |

Hourly tariffs, power quality, waste-heat availability and carbon cost. |

|

Mixed-salt disposal |

May remain a recurring waste cost after water recovery |

Leachability, landfill classification, storage, transport and offtake contracts. |

|

Feed variability / turndown |

Creates off-design energy use and unstable crystallisation |

Equalisation volume, control philosophy, bypass strategy and minimum stable load. |

|

Service and spare parts |

Determines downtime exposure |

Local technicians, compressor/pump spares, membrane lead time and remote monitoring. |

8.2 Procurement should compare guaranteed mass balances

Bids should be normalised around feed composition, annual operating hours, recovered-water quality, solids moisture, chemical consumption, electricity and steam, cleaning frequency, availability and disposal assumptions. A vendor offering 98% recovery with wet mixed salt is not automatically superior to one offering 95% recovery with a smaller thermal train and a manageable brine outlet.

|

Procurement item |

Minimum requirement |

|

Design basis |

Hourly and daily flow profile; full ionic analysis; COD/TOC; oil; silica; hardness; metals; temperature; variability and upset cases. |

|

Performance guarantee |

Recovered-water flow and quality, liquid purge, solids moisture, annual availability, energy and chemical consumption. |

|

Pilot evidence |

Test duration sufficient to observe scaling, organics, cleaning recovery and mother-liquor accumulation. |

|

Materials and corrosion |

Documented alloy selection, corrosion allowance, welding procedure and inspection plan. |

|

Control philosophy |

Automated mass balance, scaling indicators, conductivity/ion monitoring, alarm management and remote support. |

|

Waste endpoint |

Defined classification, transport, landfill or product offtake; no assumption that mixed salt has value. |

|

Lifecycle support |

Commissioning, operator training, critical spares, membrane/compressor service, performance audit and optimisation. |

9. Risks and Constraints

Full ZLD can transfer environmental impact from water to energy, carbon emissions, chemicals and solid waste. A technically compliant plant may still be economically or environmentally inefficient if it consumes high-carbon electricity, produces unstable mixed salts or runs at low availability. The correct benchmark is the whole-site water and waste balance.

|

Risk |

Probability |

Impact |

Mitigation |

|

Feed chemistry differs from design samples |

High |

High |

Extended sampling, pilot testing, conservative equalisation and contractual feed envelope. |

|

Scaling/fouling exceeds design rate |

High |

High |

Selective pretreatment, cleaning validation, online monitoring and spare capacity. |

|

Energy prices rise or waste heat is unavailable |

Medium–high |

High |

Sensitivity analysis, hybrid membrane concentration, flexible operating schedule and heat integration. |

|

Mixed salt has no buyer |

High |

Medium–high |

Treat salt revenue as upside only; secure disposal route before final investment. |

|

Regulatory deadline or plant life changes |

Medium |

High |

Stage-gated investment, modular capacity and scenario planning. |

|

Vendor performance guarantee is incomplete |

Medium |

High |

Mass-balance guarantee, liquidated damages, acceptance testing and reference checks. |

|

Plant becomes a production bottleneck |

Medium |

Very high |

Redundancy, buffer storage, bypass/emergency disposal plan and local service capability. |

A further strategic risk is over-specification. Some sites adopt ZLD because it is perceived as the most sustainable option, even when MLD plus a controlled concentrate-disposal route would use less energy and create lower total environmental impact. Project approval should include a transparent alternatives analysis.

10. Outlook to 2033

The base case is continued high-single-digit market growth, with revenue rising faster than installed flow capacity because projects increasingly include advanced pretreatment, high-pressure membrane stages, corrosion-resistant materials, automation and service contracts. Thermal equipment will remain central, but its share of treated volume should decline as membrane and selective-separation technologies push more recovery upstream.

Five developments are likely to shape the market through 2033:

- Hybrid MLD/ZLD designs will replace one-size-fits-all thermal trains, with the final recovery target selected against disposal and energy economics.

- High-recovery membrane processes will move from demonstration to broader industrial references, particularly where feed chemistry is stable and pretreatment is strong.

- Resource recovery will become more selective. Projects will target specific salts, metals or nutrients rather than treating all crystallised solids as saleable product.

- Digital mass-balance control, predictive cleaning and ion-specific monitoring will become standard in larger plants because availability has direct production value.

- Carbon intensity will enter procurement. Waste heat, low-carbon power, thermal integration and avoided freshwater pumping will increasingly be included in lifecycle assessment.

The decisive market judgement is that ZLD is becoming more important but not more generic. The best-performing suppliers will be those that understand feed chemistry, minimise the thermal load and accept measurable lifecycle guarantees. Buyers should resist evaluating systems by recovery percentage alone and instead compare the cost, energy, waste and reliability of the complete treatment endpoint.

Appendix: Data Notes and References

Data notes

- All monetary values are nominal U.S. dollars as reported by the cited source. No inflation adjustment has been applied.

- Grand View Research’s 2026–2031 line in Figure 1 is calculated from its published 2024 market value and 7.1% CAGR. The calculation does not replace the provider’s own detailed forecast.

- Regional shares in Figure 4 use Grand View Research’s 2024 global, Asia Pacific and North America values. “Rest of world” is a residual calculation.

- UN-Water’s industrial wastewater statistics are based on limited reporting coverage and must not be treated as a global average.

- Technology performance depends on feed composition, pretreatment, recovery target, plant scale and operating conditions. Vendor product claims require project-specific pilot validation.

- The five embedded Wedoany product links were matched to the user-provided product-link database. Independent live-page validation was not available in the document-generation environment.

References

[1] Grand View Research — Zero Liquid Discharge System Market Size Report, 2033. 2024 market value, 2033 forecast and regional revenue.

[2] MarketsandMarkets — Zero Liquid Discharge Systems Market, Global Forecast to 2031. 2026–2031 market forecast, process and regional shares.

[3] Mordor Intelligence — Zero Liquid Discharge Systems Market. 2026–2031 market forecast and technology commentary.

[4] UN-Water — Progress on Wastewater Treatment: 2024 Update. Industrial and domestic wastewater treatment reporting.

[5] World Resources Institute — Aqueduct 4.0 and Highest Water-Stressed Countries. Regional exposure to extremely high water stress.

[6] U.S. EPA — Steam Electric Power Generating Effluent Guidelines, 2024 Final Rule. Zero-discharge requirements for specified coal-power wastewater streams.

[7] U.S. EPA — Steam Electric Power Generating Effluent Guidelines, Deadline Extensions Rule. December 2025 deadline extensions and February 2026 update.

[8] European Commission — Industrial and Livestock Rearing Emissions Directive (IED 2.0). Current EU industrial-emissions framework.

[9] European Commission — European Water Resilience Strategy. Industrial water efficiency and reuse direction.

[10] Ministry of Environment, Forest and Climate Change, India — Note on Implementation of ZLD in Textile and Tannery Industries. Indian ZLD policy and implementation context.

[11] Tong, T. and Elimelech, M. — The Global Rise of Zero Liquid Discharge for Wastewater Management. Technology pathways, drivers and energy challenges.

[12] O’Connell et al. — Analysis of Energy, Water, Land and Cost Implications of ZLD/MLD. 2024 analysis of recovery and cost/energy trade-offs.

[13] U.S. Department of Energy / OSTI — Comparative Techno-Economic Assessment of OARO and Membrane Distillation. High-salinity membrane concentration economics.

[14] Veolia Water Technologies — HPD Evaporation and Crystallization. Commercial thermal ZLD process capabilities and references.

[15] GEA — Zero Liquid Discharge. Integrated membrane, MVR evaporation, crystallisation and solids separation.

[16] Saltworks Technologies — Zero and Minimal Liquid Discharge. Commercial modular membrane and thermal brine-management approaches.