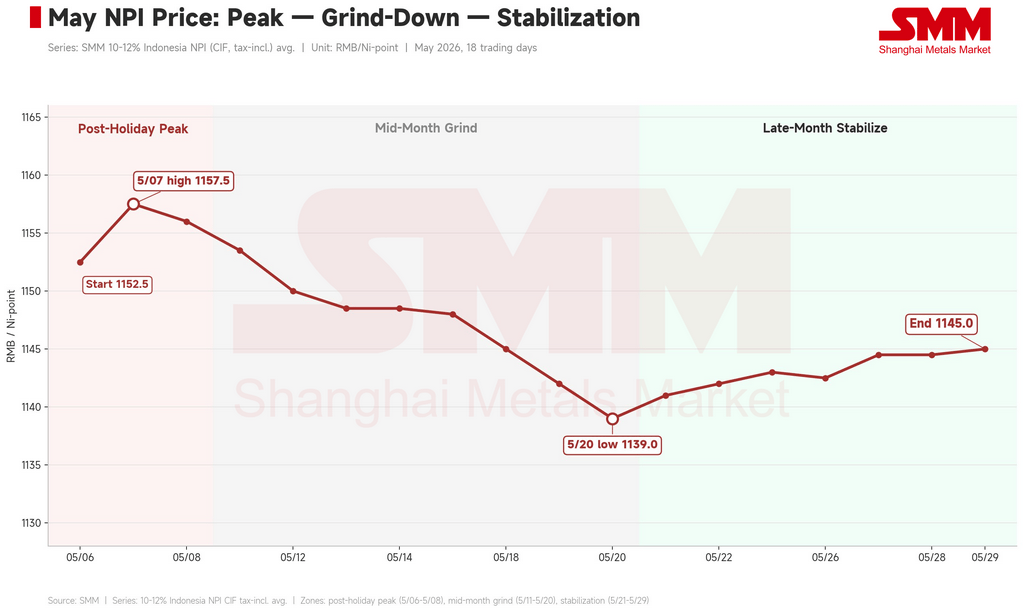

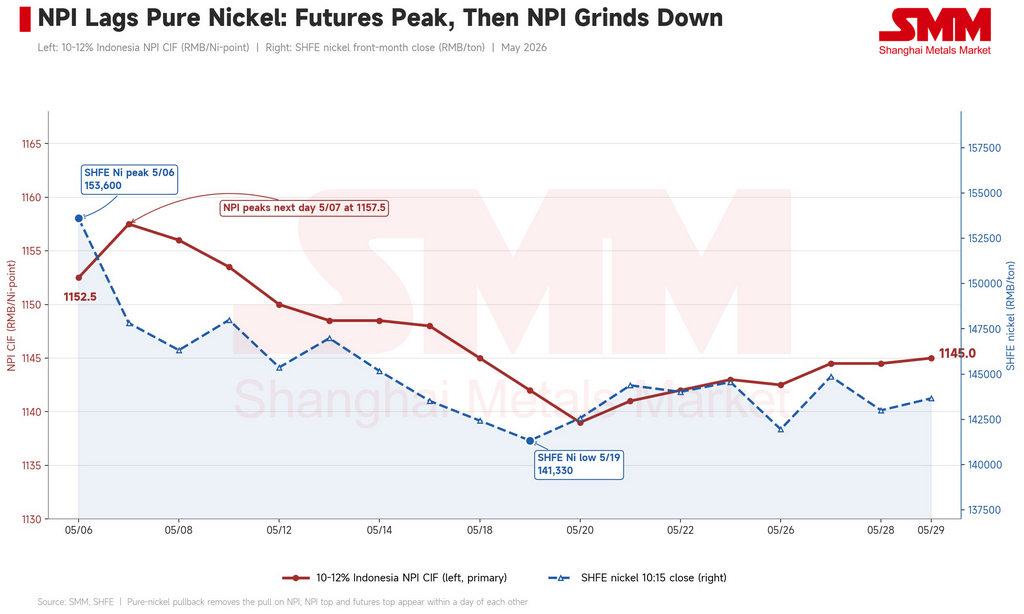

en.Wedoany.com Reported - China's high-grade nickel pig iron (NPI) prices edged down in May, with the 10-12% Indonesian high-grade NPI China CIF price slipping from 1152.5 yuan/Ni point (about $168) at the beginning of the month to 1145 yuan/Ni point (about $167) at the end, essentially giving back some of the gains from late April before entering a sideways trend. When the market reopened after the holiday, it attempted to extend the April rebound, opening at 1152.5 yuan/Ni point (about $168) on May 6 and hitting a monthly high of 1157.5 yuan/Ni point (about $169) the next day. The Shanghai Futures Exchange (SHFE) nickel contract concurrently climbed to 153,600 yuan/ton (about $22,420), pushing 304 cold-rolled coil (CRC) profit margins to 7.62%. All three peaked simultaneously—marking the ceiling for the month.

Thereafter, high-grade NPI continued to decline, hitting a monthly low of 1139 yuan/Ni point (about $166) on May 20, before recovering only in the final week to stabilize around 1145 yuan/Ni point (about $167) on policy news and production cut expectations. NPI is priced per "nickel point"—the price per ton per 1% nickel content, so the per-ton price for 10-12% grade is approximately 11 times the quoted figure. NPI is a low-grade nickel-iron alloy produced from laterite nickel ore, primarily in China and Indonesia, and is almost entirely used by stainless steel mills. Shanghai Metals Market (SMM) is a major Chinese commodity price assessment and research institution.

The May trend was not a linear decline but was dominated by three distinct phases. In the first week, a pulse-like rebound in refined nickel saw sellers raise offers to 1170-1200 yuan/Ni point (about $171-175). Mainstream smelters considered 1200 yuan/Ni point reasonable for NPI, as stainless steel had risen to 15,700 yuan/ton (about $2,290). Indeed, several hundred tons were traded at 1200 yuan/Ni point. However, these high prices were unsustainable—most trades at 1200 yuan/Ni point involved sellers hedging and closing positions, fearing nickel prices had peaked and taking the opportunity to clear inventory. These were primarily sold to intermediate traders and small mills, not driven by genuine demand. After the SHFE nickel contract hit a high of 153,600 yuan/ton on May 6, it fell to 147,800 yuan/ton (about $21,580) the next day. LME nickel also retreated from its high of $19,770/ton, and the speculative buying sentiment dissipated that same day. The 10-12% Indonesian CIF price peaked at 1157.5 yuan/Ni point on May 7, coinciding with the peak window for the nickel market.

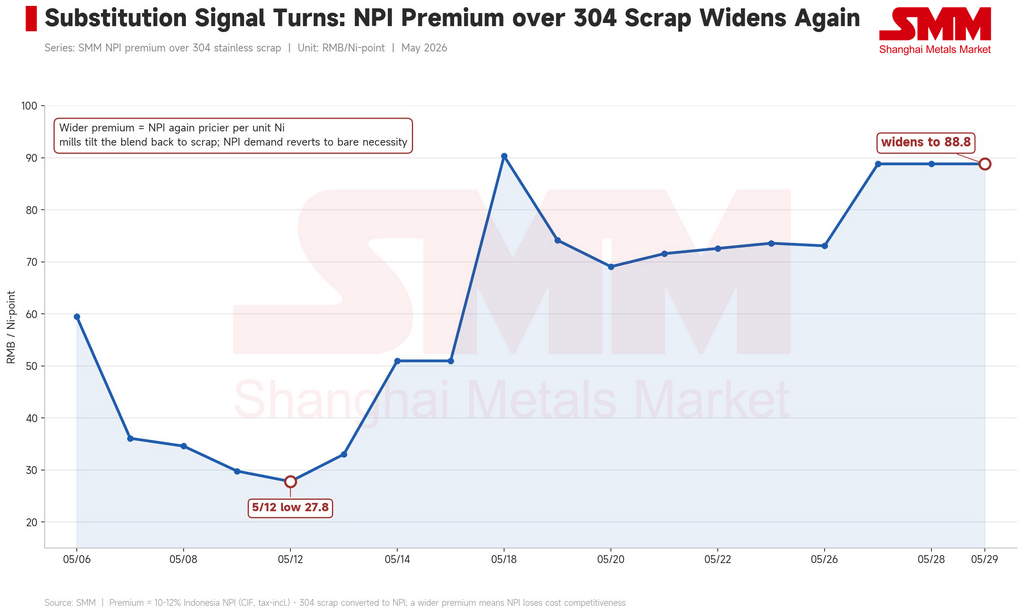

Mid-month, squeezed by futures, stainless steel, and scrap steel, was the main declining phase of the month. 10-12% Indonesian CIF fell from 1153.5 yuan/Ni point (about $168) to 1139 yuan/Ni point (about $166). The SHFE nickel contract dropped from 148,000 yuan/ton on May 11 to 141,300 yuan/ton (about $20,630) on May 19, a decline of about 8%. Stainless steel weakened, with Wuxi 304/2B spot prices falling from 15,550 yuan/ton (about $2,270) at the start of the month to 15,200 yuan/ton (about $2,220). The SHFE stainless steel contract fell from 15,710 yuan/ton to a low of 14,555 yuan/ton (about $2,125) on May 19. 304 CRC profit margins were compressed from 7.62% after the holiday to 5.40% on May 20. The scrap steel price spread normalized—the implied scrap nickel point cost in the market fell from 1132 yuan/Ni point (about $165) at the start of the month to 1128 yuan/Ni point (about $165) on May 19, with scrap steel once again dropping 200 yuan/ton (about $29). The premium of high-grade NPI over 304 stainless steel scrap expanded sharply from a monthly low of 27.8 yuan/Ni point (about $4) on May 12 to 88.84 yuan/Ni point (about $13) at the end of the month, prompting mills to shift their mix towards scrap and reduce NPI procurement to essential needs. During the same period, the Indonesian CIF price for 1.5% grade trade laterite ore rose from $70.75/wmt to $73.80/wmt. The Indonesian NPI FOB index held steady to slightly firm, and NPI smelting margins even turned from negative to positive, but cost alone could not support the uptrend.

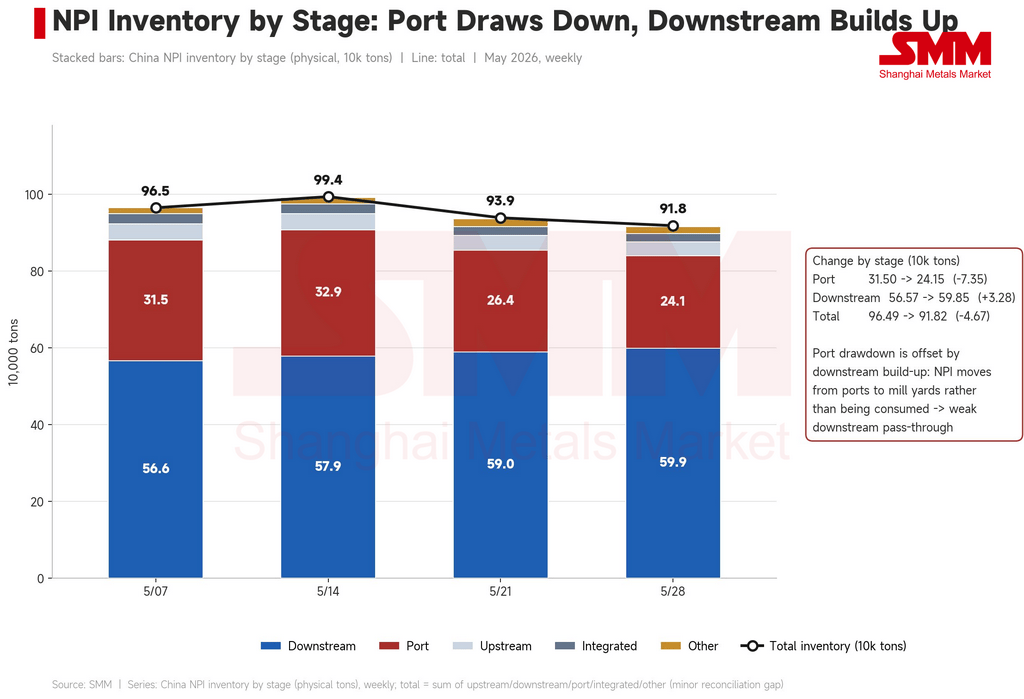

In the final week, the decline halted after May 21, with prices stabilizing and recovering slightly within the 1139-1145 yuan/Ni point range. Indonesian export and unified pricing policies were widely cited by sellers as a disruptive factor. They believed that if Jakarta's unified government pricing took effect, retail spot supply would decrease significantly. One trader even raised offers by 20 yuan/Ni point (about $3) on the day of the policy news, but most doubted the enforcement. Regarding production switching and cuts, a major Indonesian producer indicated it would convert some NPI production lines to high-grade nickel matte (HGNM) starting in June. Combined with production cuts at an integrated project due to power constraints and another large producer deferring some contract deliveries to July due to high inventory, the market formed a fairly strong expectation of reduced NPI inflows into China. However, inventory situations need to be viewed by segment: port inventories fell from 315,000 tons at the start of the month to 241,500 tons at the end, but downstream mill NPI inventories rose from 566,000 tons to 599,000 tons. Total inventories edged down slightly from 965,000 tons to 918,000 tons, with NPI increasingly accumulating at the mill level. 304 profit margins continued to compress that week to 4.96%, further tightening the absorption valve. At the end of the month, premiums for 11% grade trades were generally only 3-7 yuan/Ni point (about $0.4-1.0), far below the 10 yuan/Ni point (about $1.5) seen mid-month. The supply side propped up the bottom, while the demand side capped the top, leaving prices stuck in a high-level stalemate.

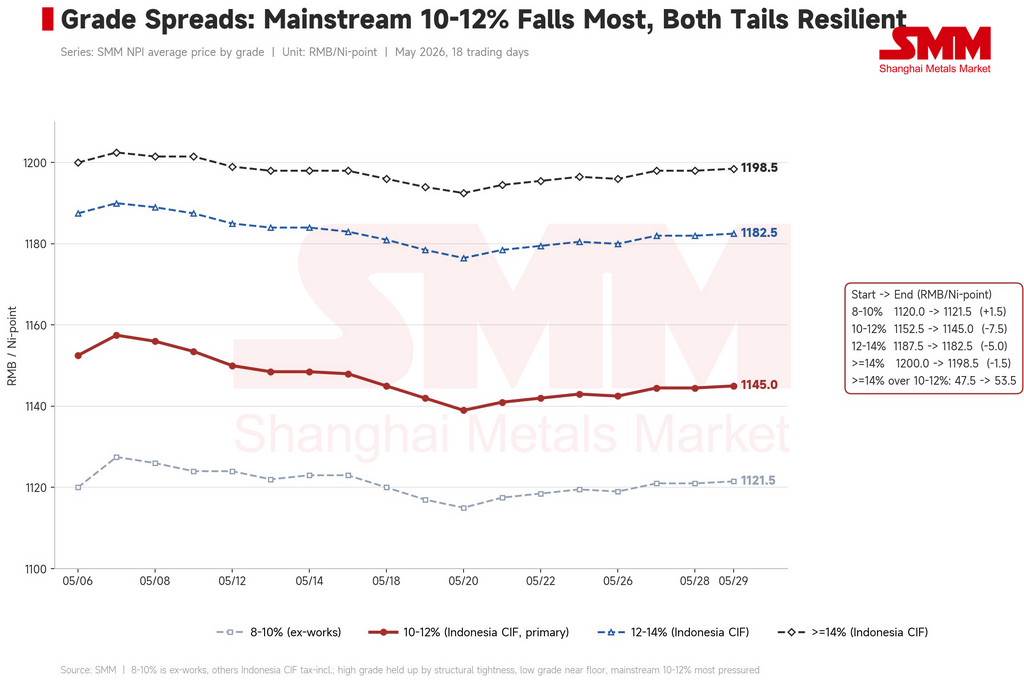

Among the various grades, mainstream 10-12% saw the largest decline, while the high and low ends held steady. Ex-works prices for 8-10% edged up slightly from 1120 yuan/Ni point to 1121.5 yuan/Ni point (about $164), essentially flat; 10-12% Indonesian CIF fell by 7.5 yuan; 12-14% fell by 5 yuan; ≥14% fell by only 1.5 yuan. The high end was supported by structural scarcity, with grades above 12% remaining tight throughout the month. Multiple sources reported fewer offers, with only one or two holding inventory. The premium of ≥14% over 10-12% expanded from 47.5 yuan/Ni point (about $7) at the start of the month to 53.5 yuan/Ni point (about $8) at the end, while the 12-14% premium edged up from 35 yuan/Ni point (about $5) to 37.5 yuan/Ni point (about $5.5). The low-end 8-10% was already at bottom levels, with 9-10% grade difficult to sell around 1100 yuan/Ni point (about $161). With no room for further decline, it merely stabilized at the bottom.

Looking ahead to June, the direction still depends on three external variables. First, whether stainless steel prices and mill profits can stop declining—304 CRC profit margins have already compressed from 7.62% at the start of the month to below 5%, and 304 spot prices fell from 15,550 yuan/ton to 15,200 yuan/ton. SMM's forecast for mid-May Indonesian 300-series production of 1.795 million tons has been realized (down 120,000 tons month-on-month from April), and 300-series inventories edged up slightly to 608,300 tons at the end of the month. Second, the cost of high-grade NPI relative to scrap steel—the premium at the end of the month has expanded to nearly 89 yuan/Ni point (about $13), re-establishing scrap's cost advantage. Third, the refined nickel market—the SHFE nickel contract stabilized at 143,000-145,000 yuan/ton (about $20,880-$21,170) at the end of the month. In the base case scenario, high-grade NPI is most likely to trade in a high but soft range of 1130-1160 yuan/Ni point (about $165-$169) in June. Upside risks include a synchronized rebound in stainless steel futures and spot prices, faster-than-expected implementation of Indonesian policies, and actual conversion to HGNM production. Downside risks include further weakening of stainless steel, a pullback in refined nickel, and the continued expansion of scrap steel's substitution advantage.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com