en.Wedoany.com Reported - The Latin American Steel Association (Alacero) forecasts that the region's apparent steel consumption in 2026 will grow by only 0.5% year-on-year to 75.6 million tons, with an expected increase of 2.5% to 77.5 million tons in 2027. In an interview published via the Fastmarkets platform, the association's Executive Director, Ezequiel Tavernelli, stated that this outlook contrasts with steel production performance, which remains near its lowest levels in the past 15 years.

In February of this year, the association had projected a 2.8% growth in Latin America's apparent steel consumption for 2026, but has now revised its forecast down by 2.3 percentage points. Alacero estimates that total crude steel production in Latin America in 2025 was approximately 55.7 million tons, below the level during the COVID-19 pandemic in 2020 and one of the weakest performances in historical data. Finished steel production follows a similar trend, totaling 42 million tons in 2025, with a slight increase to 42.2 million tons expected in 2026, despite the region's steel consumption remaining relatively resilient.

"We are not facing a consumption collapse. The problem is that production continues to decline while imports keep rising," Tavernelli said in an exclusive interview with Fastmarkets in early June.

According to Alacero data, the region's apparent steel consumption has remained around 74 to 75 million tons for years, but imports have increased from approximately 20 million tons a few years ago to over 30 million tons currently. In 2025, the import penetration rate as a share of the region's consumption reached a record 41%. Tavernelli noted that for every ten kilograms of steel consumed in Latin America, four kilograms are imported, with most of these materials coming from countries benefiting from government support and idle capacity.

Inventory adjustments are a key factor limiting growth in 2026. Alacero's expectations for Argentina, Colombia, and several smaller Latin American markets are weaker, primarily due to sluggish construction activity and inventory adjustments following a surge in imports in 2025. Tavernelli explained that imports were strong in the region in 2025, but a significant portion of the materials was not directly used for consumption, leading to an expected near-zero growth in steel consumption in 2026.

In terms of demand structure, construction remains the largest steel-consuming sector in Latin America, accounting for about 50% of the region's demand, with housing and infrastructure activity levels being particularly important for the market outlook. The automotive industry accounts for 18% of demand, making it the second-largest consuming sector, although its production lost momentum in the second half of 2025. Metal products account for another 14% of demand, while machinery represents 13%, one of the best-performing industrial sectors last year, driven by growth in Brazil, Argentina, and Chile. Household appliances and electrical equipment each account for 2%, with other transportation applications making up the remainder. Alacero expects industrial activity to gradually improve, despite mixed performance across sectors, as investment, infrastructure spending, and economic growth are poised to gain momentum.

The association forecasts an improvement in 2027, with regional steel demand growing by 2.5%. Brazil and Mexico remain the main drivers of growth, supported by recently implemented trade measures and industrial policies; Argentina may benefit from investments in energy and mining projects; and Colombia is also expected to return to growth. Tavernelli stated that the expected improvement should not be viewed merely as a recovery from a weak year. He noted that per capita steel consumption in Latin America remains around 100 kilograms, compared to 180 to 250 kilograms in developed economies, with countries like China and South Korea consuming more during their industrialization phases. He believes the region still has significant growth potential through infrastructure development and industrial expansion.

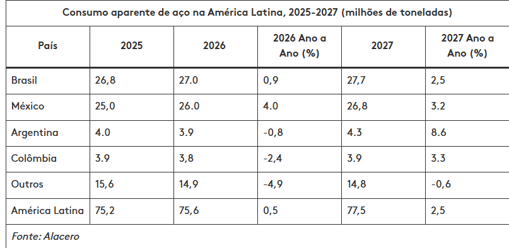

At the country level, Alacero forecasts that Brazil's apparent steel consumption will grow by 0.9% in 2026 to 27 million tons, followed by a further 2.5% increase to 27.7 million tons in 2027. Mexico is expected to see the most significant growth, with demand rising by 4.0% to 26 million tons in 2026 and an additional 3.2% to 26.8 million tons in 2027. In contrast, Argentina's steel demand is expected to decline by 0.8% in 2026 to 3.9 million tons, before rebounding by 8.6% in 2027; Colombia's consumption is forecast to fall by 2.4% to 3.8 million tons, with a 3.3% recovery the following year. Demand in smaller Latin American markets is expected to decline by 4.9% in 2026.

Alacero views global steel overcapacity as the greatest threat facing the region. According to data from the Organisation for Economic Co-operation and Development (OECD) cited by the association, global steel overcapacity is expected to increase from 640 million tons in 2025 to 721 million tons in 2027. More than half of the world's crude steel production comes from China. Tavernelli pointed out that while China's domestic steel demand continues to decline, production remains near 1 billion tons annually, generating significant surplus capacity available for export. "China alone has over 200 million tons of steel production exceeding domestic demand, which is roughly four times Latin America's annual steel output." He added that Chinese steel companies' investments in Southeast Asia, along with growing exports from countries such as Vietnam, South Korea, Egypt, and Turkey, are collectively exacerbating the problem.

Alacero welcomes trade measures taken by countries such as Brazil, Mexico, Colombia, and Peru, believing they help mitigate unfair trade imports. However, Tavernelli warned that Latin America remains vulnerable to trade diversion, as the United States and Europe continue to strengthen barriers against subsidized steel imports. "We are concerned about countries in the region that lack adequate self-defense. Steel that can no longer access other markets will continue to seek less protected export destinations." He noted that Fastmarkets' assessment for hot-rolled coil imports, CFR main South American ports, was $650-690 per ton on Friday, June 19, down $15-20 from $665-710 per ton the previous week.

In Alacero's view, rising imports are fueling a broader deindustrialization process in Latin America, with manufacturing's share of GDP declining over the past decades and exports increasingly reliant on raw materials rather than higher-value-added manufactured goods. Tavernelli stated that the industry's challenges extend beyond steel prices and trade flows, touching on broader issues of industrial competitiveness. "We have the raw materials, energy resources, industrial base, and talent to become one of the strongest steel-producing regions in the world. But we need a level playing field for local industry to grow alongside the region's economic development."

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com