en.Wedoany.com Reported - Last week, the raw material market for China's home appliance sector showed clear divergence: Steel prices continued to weaken, with sentiment indices for cold-rolled and galvanized sheets declining notably. In non-ferrous metals, prices of electrolytic aluminum and electrolytic copper retreated from highs, with electrolytic aluminum falling 2.4% and electrolytic copper dropping 1.91%. According to the latest production plan report for three major white goods released by ChinaIOL, the total combined production plan for air conditioners, refrigerators, and washing machines in July 2026 is 29.17 million units, down 7.1% from the actual production volume in the same period last year.

In the steel market, fundamental data for cold-rolled coils showed that the operating rate of 29 cold-rolled coil producers monitored by Mysteel was 82.98% last week, flat week-on-week. The capacity utilization rate of steel mills was 86.40%, down 0.27% week-on-week. Actual weekly production was 874,500 tons, down 2,800 tons week-on-week. Steel mill inventories stood at 403,900 tons, up 11,100 tons week-on-week. Although the capacity utilization rate for cold-rolled products has been declining recently, it remains at a relatively high level, with steel mills still showing production enthusiasm. Weekly output for sample enterprises is expected to remain in the range of 860,000 to 880,000 tons this week. Market traders reported a clear off-season effect. Despite covert price cuts to accelerate shipments, transaction performance was poor. Market inventories rose slightly, reflecting a pattern of strong supply and weak demand. In terms of transactions, the black futures market fluctuated weakly last week, with most market prices experiencing slight declines. Currently, market demand is in the off-season, and traders remain cautious about the outlook, with average transaction performance during the week. Overall, the national cold-rolled coil market is expected to fluctuate weakly this week.

For galvanized sheets, Mysteel survey data last week showed that the overall operating rate of national galvanized sheet producers was 89.32%. The capacity utilization rate was 66.67%, up 2.29% week-on-week. Weekly production was 1.1777 million tons, up 40,500 tons week-on-week. Steel mill inventories were 594,900 tons, up 4,600 tons week-on-week. Social inventories were 1.5545 million tons, up 30,000 tons week-on-week. Total inventories were 2.1494 million tons, up 34,600 tons week-on-week. The hot-rolled coil futures market performed weakly last week, with most market prices following the uptick, but trading sentiment weakened. Merchants repeatedly lowered quotes but still struggled to boost shipments. As the off-season for home appliance demand approaches in July-August, galvanized sheets, as a key raw material, will face increased sales pressure. Many merchants have recently focused on destocking, and order volumes for the future have been appropriately reduced. In terms of price performance, prices in cities such as Hefei, Nanjing, Shenyang, Changchun, Fuzhou, and Lanzhou remained stable, while prices in other cities fell by 10-90 yuan/ton. Cities like Ningbo, Jinan, Zhengzhou, Xi'an, and Kunming saw declines of over 50 yuan/ton.

Regarding steel mill dynamics, according to Mysteel's full-sample survey of hot-rolled coils, the estimated total impact volume for hot-rolled coils last week was 21,000 tons. The actual total impact volume this week was -64,000 tons, and the estimated total impact volume for next week is 18,700 tons. This week, one steel mill in Hebei began maintenance, and another in Hebei resumed production (this week's statistical period: June 18, 2026 to June 24, 2026; next week's statistical period: June 25, 2026 to July 1, 2026).

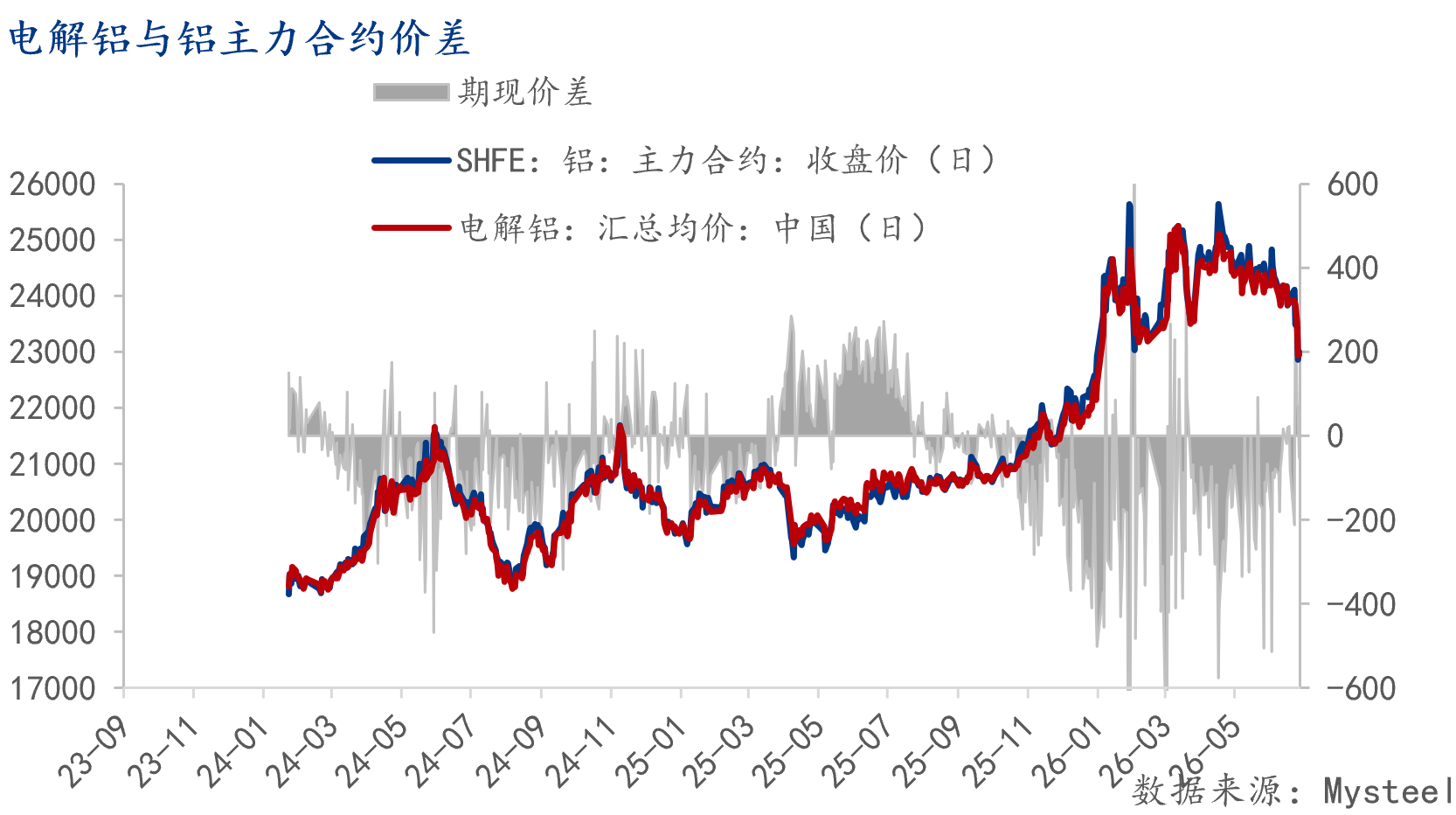

In the non-ferrous metals market, electrolytic aluminum prices fluctuated and retreated from highs overall in June, with spot prices ranging from 23,800 to 24,330 yuan/ton. Aluminum prices continued to weaken, making it difficult for recyclers to replenish inventories. Scrap aluminum inventories were low, with most being high-priced stockpiles, leading to weak willingness to sell. Downstream recycled aluminum plants actively replenished at lower prices, but due to tight supply and high prices in the scrap aluminum market, recent arrivals were poor, forcing them to purchase at high prices. Tax rectification efforts continue across regions, and the scope of "reverse invoicing" controls is likely to expand further. The shortage of raw materials for alloy ingot plants is difficult to alleviate, with production cuts persisting. ADC12 prices are prone to rise rather than fall. The accelerated decline in aluminum prices has further narrowed the price spread between bright aluminum wire and scrap aluminum, leading to more instances of electrolytic aluminum replacing scrap aluminum in production.

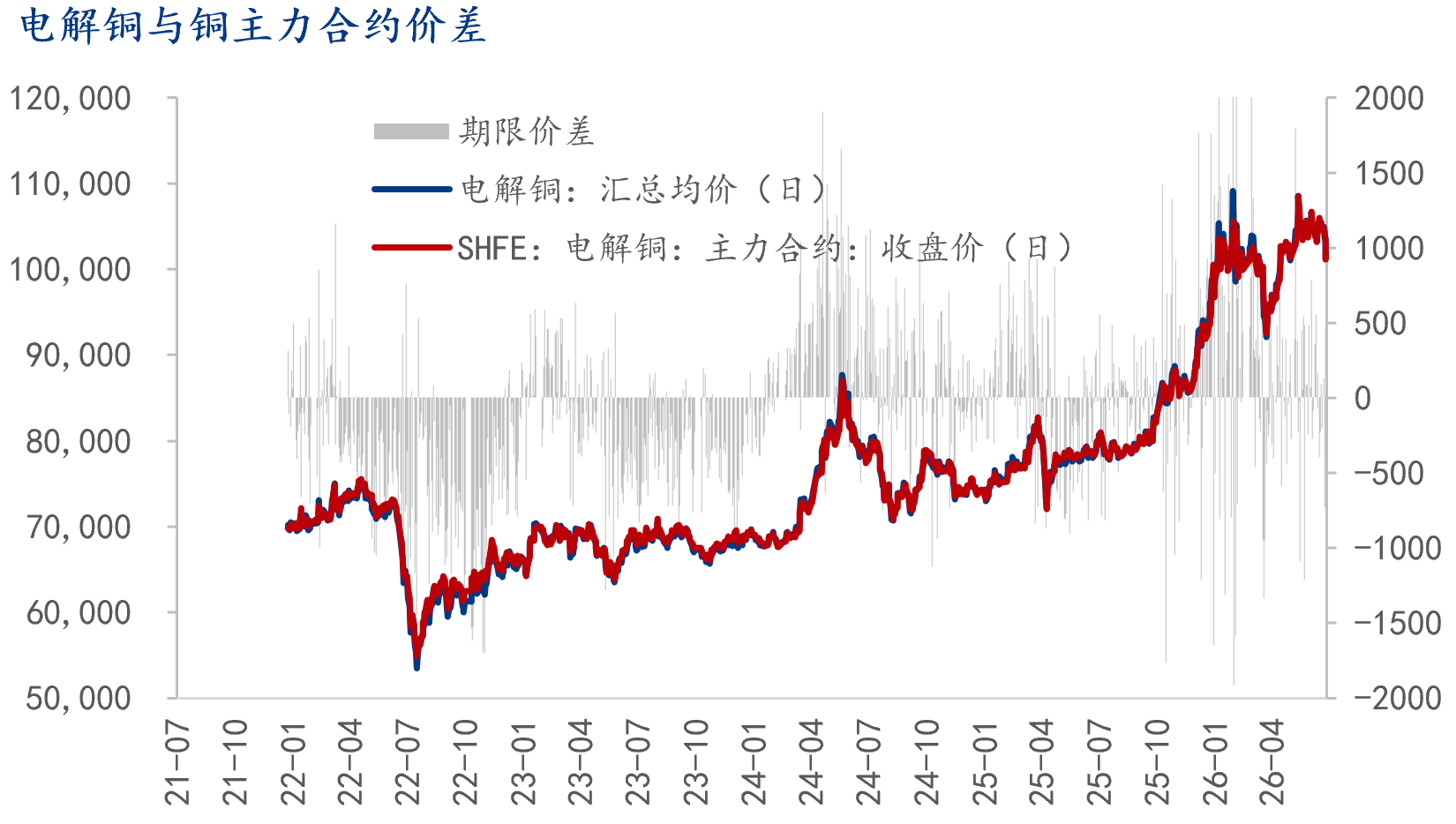

In the electrolytic copper market, domestic inventory of electrolytic copper stood at 212,600 tons, up 6,800 tons from the 18th and down 3,100 tons from the 22nd. Inventories in the Shanghai market first increased and then decreased. Recently, arrivals of domestic and imported copper have increased, but as copper prices fell during the week, downstream enterprises showed decent demand for replenishment at lower prices, leading to an overall decline in inventories. In the short term, copper prices are weakening, leaving room for further improvement in downstream consumption. However, with the import price ratio recovering, imports are expected to increase, and inventories are likely to decline slightly. Inventories in the Guangdong market continued to accumulate. As shipments from some smelters increased, warehouse inflows rose. However, the decline in spot premiums and copper prices also stimulated some downstream demand during certain periods, limiting the extent of inventory accumulation. Last week, copper prices shifted downward, and spot premiums and discounts weakened simultaneously. As the end of the half-year approaches, some holders showed a need to recover funds, engaging in low-price sales during the day to cash out, which later narrowed the spot discount. This week, as the month-end approaches, some holders have reduced sales activities. Meanwhile, with copper prices at low levels, downstream demand for purchases still has room to improve, and spot premiums and discounts are expected to stabilize and rise.

In industry highlights, the latest production plan report for three major white goods released by ChinaIOL shows that the total combined production plan for air conditioners, refrigerators, and washing machines in July 2026 is 29.17 million units, down 7.1% from the actual production volume in the same period last year. By product, the production plan for household air conditioners in July is 13.95 million units, down 13.4% from the actual production volume in the same period last year; refrigerators are planned at 7.93 million units, up 0.8% from the actual production volume in the same period last year; and washing machines are planned at 7.29 million units, down 1.7% from the actual production volume in the same period last year. Additionally, many parts of Europe have been experiencing sustained high temperatures. On the 24th, France's national average temperature reached 30 degrees Celsius, the highest since records began in 1947. Some areas in the UK recorded temperatures exceeding 36 degrees Celsius on the 24th, breaking the country's June daily high temperature record since 1957. The persistent heatwave has caused at least two deaths from heatstroke in Spain. A research report from Century Securities indicates that the current penetration rate of the European air conditioning market is low. This extreme heatwave is expected to activate local consumer demand, driving a recovery in terminal air conditioning sales and potentially accelerating stocking pace in offline channels. The global trend of frequent high-temperature weather continues to solidify the demand for overseas refrigeration equipment, providing incremental space for the air conditioning industry's overseas expansion. Air conditioning leaders with global layouts and high overseas business proportions are well-positioned to capitalize on these advantages.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com