en.Wedoany.com Reported - New Jersey's commercial and industrial rooftop solar potential is as high as 22 GW, yet the current utilization rate stands at only 7.2%. Among 88,429 commercial and industrial rooftops, only 7.2% have solar installations installed, meaning 17.5 GW of untapped capacity exists on rooftops that already meet load conditions, are connected to the grid, and have obtained commercial use permits—a figure more than four times New Jersey's total existing installed solar capacity. This phenomenon in New Jersey is not an isolated case but a true reflection of the potential in the commercial and industrial solar market.

Commercial solar developers often rely on referrals and repeat collaborations, leaving a large addressable market untapped. Data shows that adoption rates for large rooftops exceeding 50,000 square feet are below 30%. In building types such as distribution centers, pharmaceutical parks, cold chain facilities, and large retail stores, behind-the-meter solar offers the greatest advantages, yet most have never been approached for solar discussions. In northern New Jersey alone, there are approximately 50,000 commercial rooftops with nearly 14 GW of untapped electricity potential, requiring no new land use permits. Within the PSE&G service area, 48,422 sites hold 10.5 GW of unbuilt rooftop solar capacity, with Middlesex, Union, Bergen, and Hudson counties concentrating a large amount of untapped large-rooftop potential.

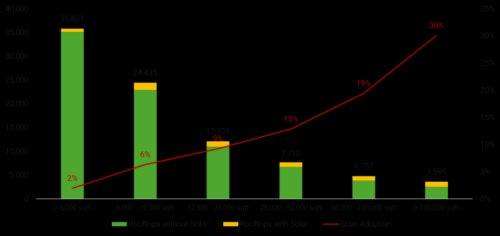

Commercial building owners' perceptions of energy volatility have changed significantly over the past three years. The 2022 Russia-Ukraine gas crisis led to historically high energy prices in Europe, triggering a wave of commercial and industrial rooftop solar adoption, shifting decision-making logic from environmental to financial. A missile attack on Qatar's Ras Laffan facility in March 2025 took approximately 17% of liquefied natural gas export capacity offline, exacerbating volatility in the global gas market. Companies signing commercial and industrial solar contracts in 2026 aim to lock in a fixed portion of their energy costs for the next 25 years, rather than merely achieving ESG goals. A developer dialogue approach centered on fuel risk exposure will significantly shorten sales cycles.

Grid interconnection is the true constraint on the growth of the commercial and industrial solar sector. In the PJM region, interconnection queue times for commercial-scale solar have significantly lengthened, with rule differences among a few state-level public utility commissions causing most of the delays. Anticipated regulatory changes for solar development in New Jersey may shift developer attention toward rooftops, intensifying competition for commercial-side interconnection queue positions. Over the next 24 months, developers who prioritize projects in utility areas with clear interconnection processes, submit interconnection applications early, and act on specific PJM queue dynamics will hold an advantage.

Geospatial AI platforms can map entire utility service areas, ranking rooftops by size and solar suitability, and filtering out sites that have not adopted solar. Developers can obtain a pre-screened list of the best rooftops before making their first cold call. In nearly every dense commercial market across the United States, similar structural gaps exist between actual rooftop potential and current solar adoption rates.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com