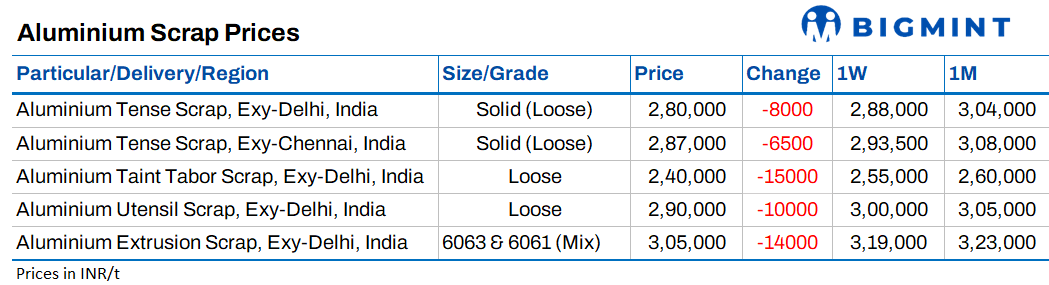

en.Wedoany.com Reported - India's imported scrap aluminum prices fell sharply week-on-week, dragged down by weakening London Metal Exchange (LME) aluminum prices and sluggish demand from domestic buyers.

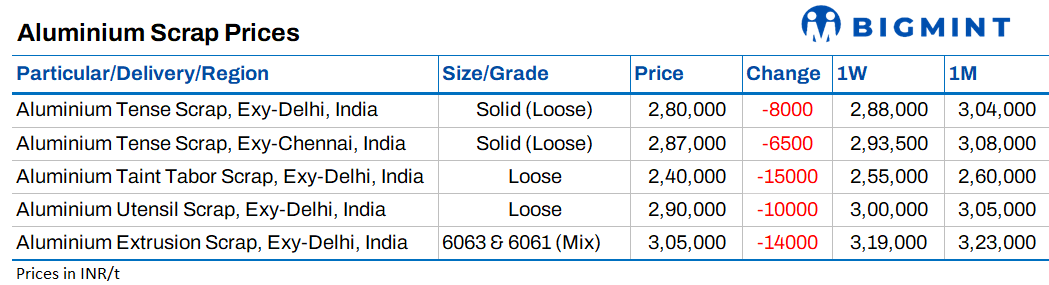

According to the latest assessment by commodity data platform BigMint for CFR Nhava Sheva delivery, UK-origin Zorba 95-5 scrap aluminum prices fell by $135/ton week-on-week to $2,750/ton, while US-origin Tense 6-7% scrap aluminum prices dropped by $140/ton week-on-week to $2,525/ton. Weak buying interest and bearish sentiment in the global market continued to weigh on import prices.

LME three-month aluminum prices moved lower week-on-week, closing at $3,091/ton on June 30, down $180/ton from $3,271/ton on June 23, a decline of 5.5%. During the same period, LME aluminum inventories decreased by 6,500 tons (down 2.1% week-on-week), from 311,725 tons to 305,225 tons, indicating continued destocking in warehouses. One reason for the decline in LME aluminum prices was the easing of geopolitical tensions in the Middle East, which reduced the supply risk premium that had supported prices in recent weeks. Expected improvements in aluminum shipments from major Gulf producers, coupled with a stronger US dollar, dampened investor sentiment and triggered profit-taking, pushing the three-month aluminum contract to its lowest level in nearly three months.

Imported scrap aluminum prices continued to decline this week, reflecting lower domestic scrap aluminum prices as weaker LME aluminum prices dampened market sentiment. Against the backdrop of easing geopolitical tensions and improved global supply prospects, the primary aluminum market experienced a correction, prompting buyers to adopt a cautious stance. Market activity was dominated by on-demand purchasing, with participants avoiding building inventories in anticipation of further price corrections. Despite the overall price weakness, market sources noted that supply of certain scrap aluminum grades remained tight, indicating persistent supply constraints in specific areas.

In the short term, imported scrap aluminum prices are expected to see only moderate adjustments, following the trend in the primary aluminum market. However, due to new supply-side risks emerging in major exporting regions, the medium- to long-term outlook remains supportive of prices. The UAE has implemented a four-month ban on exports of certain ferrous metals, aluminum, and copper scrap as part of a strategy to retain recyclable raw materials for domestic processing and downstream manufacturing. Although the UAE accounts for only about 6% of India's scrap aluminum imports, it remains a strategically important supplier due to geographical proximity, competitive freight costs, and shorter transit times. Any long-term restrictions could tighten regional scrap supply.

A more significant development is unfolding in Europe, which accounts for nearly 20% of India's scrap aluminum imports. The European Commission earlier this year postponed its proposal to restrict aluminum scrap exports to September 2026 to allow for further consultation with industry stakeholders. However, recent market reports indicate that the EU is now preparing to impose a 15% tax on aluminum scrap exports, with the proposal expected to be submitted on September 9. If approved by EU member states, this would mark the first time the EU has levied a fee on aluminum scrap exports, reflecting its broader goal of retaining secondary raw materials to strengthen domestic recycling and downstream manufacturing. While these measures have not yet been finalized, they have already influenced market sentiment. The prospect of tighter scrap supply from two strategically important sourcing regions is expected to limit the downside for imported scrap aluminum prices. Therefore, although prices may remain under pressure in the short term due to weak LME aluminum prices, any correction is likely to be moderate. Looking ahead, market participants are expected to closely monitor EU policy developments, as the formal decision in September could tighten global scrap supply and provide new support for scrap aluminum and secondary aluminum alloy prices.

On the domestic front, trading activity has also weakened. As global aluminum prices softened, the domestic market saw significant declines, particularly in foundry-grade scrap aluminum prices, which fell sharply week-on-week in both southern and northern regions amid weak demand and cautious purchasing sentiment. According to BigMint's latest assessment, China-origin 553# silicon metal prices fell by $65/ton week-on-week, from $1,435/ton to $1,370/ton CFR Mundra. This was due to weak demand from downstream polysilicon and aluminum alloy industries, which led to softer Chinese export offers, coupled with ample supply, pressuring the market.