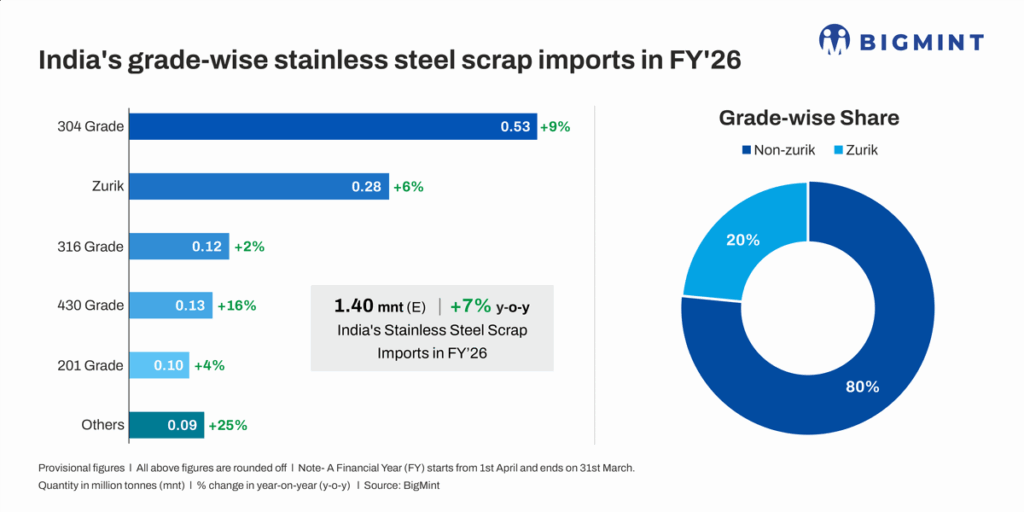

en.Wedoany.com Reported - India's stainless steel scrap imports in FY2026 (April 2025 to March 2026) are expected to increase by 7% year-on-year to 1.4 million tonnes, compared to 1.3 million tonnes in the previous fiscal year. The 300 series continues to dominate import categories, with domestic stainless steel capacity expansion supporting scrap demand, while declining nickel pig iron imports are prompting mills to shift towards scrap-based melting.

Among major grades, 304 scrap imports are projected to increase by 9% year-on-year to approximately 530,000 tonnes; 316 grade scrap imports are expected to grow by 2% to nearly 120,000 tonnes, primarily due to rising molybdenum prices and tightening global supply of high-quality raw materials. Zurik scrap imports are forecast to increase by 6% to 280,000 tonnes, supported by strong secondary stainless steel melting activity. 200 series scrap imports are expected to remain broadly stable at around 130,000 tonnes, as competition from finished product imports and margin pressure on low-nickel stainless steel may limit aggressive purchasing. 400 series scrap imports are projected to decline by 7% year-on-year to approximately 170,000 tonnes, with 430 grade scrap imports expected to drop significantly by 16% to nearly 110,000 tonnes, due to weak demand in the cutlery and white goods sectors and increased availability of domestic substitutes.

In terms of supply sources, the United States remains India's largest stainless steel scrap supplier, with shipments estimated at approximately 190,000 tonnes in FY2026, broadly stable year-on-year. However, growth from Asian suppliers has accelerated significantly, with Vietnam emerging as one of the fastest-growing suppliers, with shipments surging from nearly 110,000 tonnes in the previous fiscal year to approximately 180,000 tonnes. South Korean exports also rose markedly from 28,000 tonnes last year to around 180,000 tonnes, reflecting enhanced regional scrap availability and competitive pricing to India. Thai shipments remained broadly stable at approximately 110,000 tonnes, supplemented by incremental cargoes from Malaysia, Saudi Arabia, the UAE, and other Southeast Asian origins. Market sources noted that geopolitical uncertainties, freight rate volatility, and tightening supply in Western markets prompted Indian importers to increasingly focus on Asian sources throughout the year.

Key factors driving import growth include: rising domestic stainless steel production, with India's finished stainless steel output increasing by 12% year-on-year to approximately 4.44 million tonnes in FY2026 (compared to 3.9 million tonnes in the previous fiscal year), driven by stronger demand from infrastructure, railways, process industries, pipe and tube sectors, and export-oriented manufacturing, which in turn fueled scrap raw material demand; imported scrap remaining price-competitive, as despite higher freight and port handling costs, the average price of imported 304 scrap in FY2026 was approximately $1,280-$1,285/tonne CFR Mundra, equivalent to approximately Rs 117,000-117,500/tonne after accounting for related charges, while domestic 304 scrap prices averaged around Rs 113,000-113,500/tonne DAP Delhi, with imported scrap continuing to attract buyers due to superior quality, bulk availability, and supply stability; declining semi-finished product imports, with India's stainless steel billet imports dropping sharply by 49% year-on-year to approximately 59,000 tonnes in FY2026 (compared to around 110,000 tonnes last year), with Indonesia remaining the sole major supplier; and declining ferro-nickel and nickel pig iron imports, with ferro-nickel imports projected to decrease by 47% year-on-year to approximately 110,000 tonnes in FY2026 (compared to 210,000 tonnes in FY2025), including Indonesian shipments of around 100,000 tonnes, down 45% year-on-year, while India's nickel pig iron imports during the same period were estimated at approximately 130,000 tonnes. Industry participants believe that rising Indonesian ore prices, stricter RKAB approvals, revisions to the HPM pricing mechanism, and higher energy costs have eroded the competitiveness of imported ferro-nickel and nickel pig iron, prompting mills to increasingly rely on stainless steel scrap.

Looking ahead, India's stainless steel scrap imports are expected to remain firm in the near term, benefiting from continued domestic stainless steel capacity expansion, robust demand in the 300 series segment, and a growing preference for scrap-based melting amid alloy market volatility. However, buyers' procurement strategies are likely to remain cautious, given ongoing uncertainties surrounding LME nickel price fluctuations, freight rate volatility, geopolitical developments, and the evolution of Indonesian nickel policies. Buyers are expected to continue diversifying procurement sources to maintain supply stability and manage raw material costs more effectively.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com