en.Wedoany.com Reported - Yan Qing, Deputy General Manager of Guangxi Yusheng Germanium High-Tech Co., Ltd., analyzed the current status and future trends of China's germanium industry at the 2026 SMM (14th) Small Metals Industry Conference – Rare and Dispersed Metals Industry Forum.

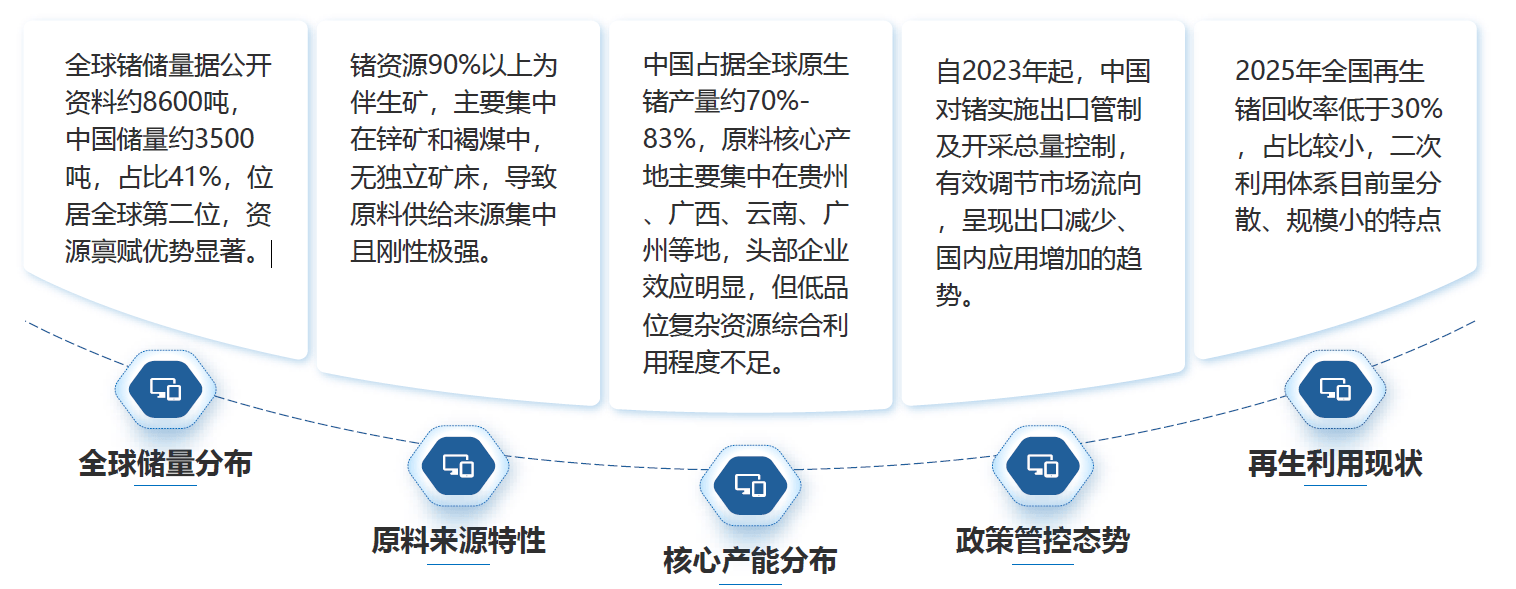

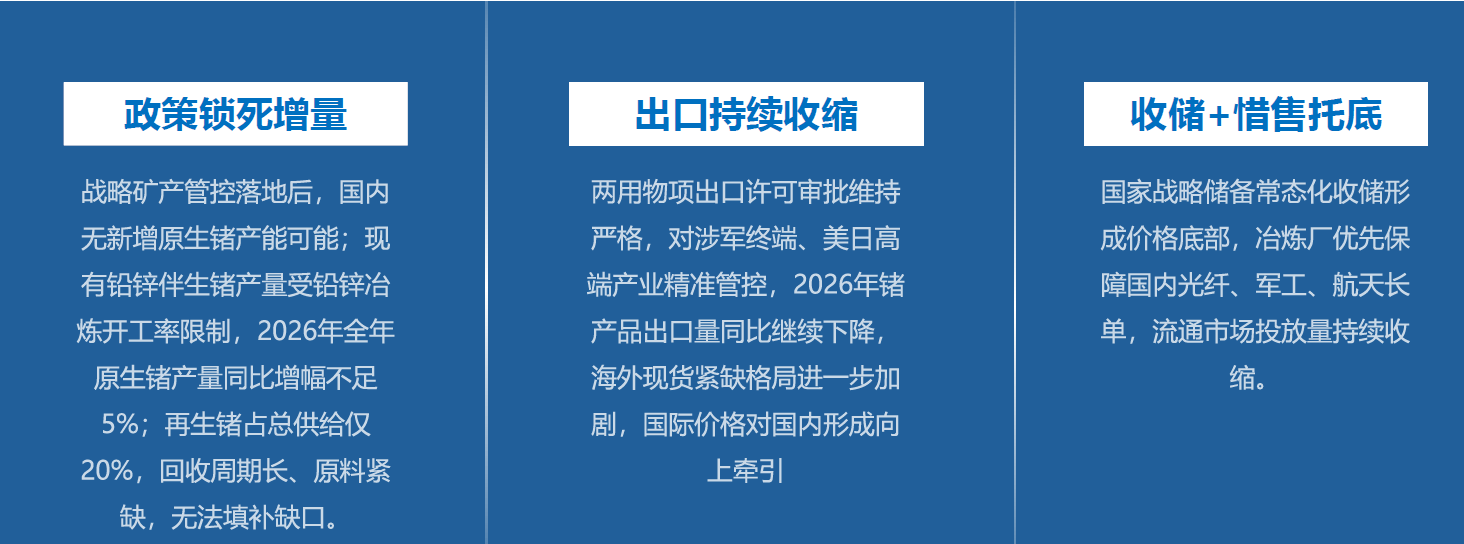

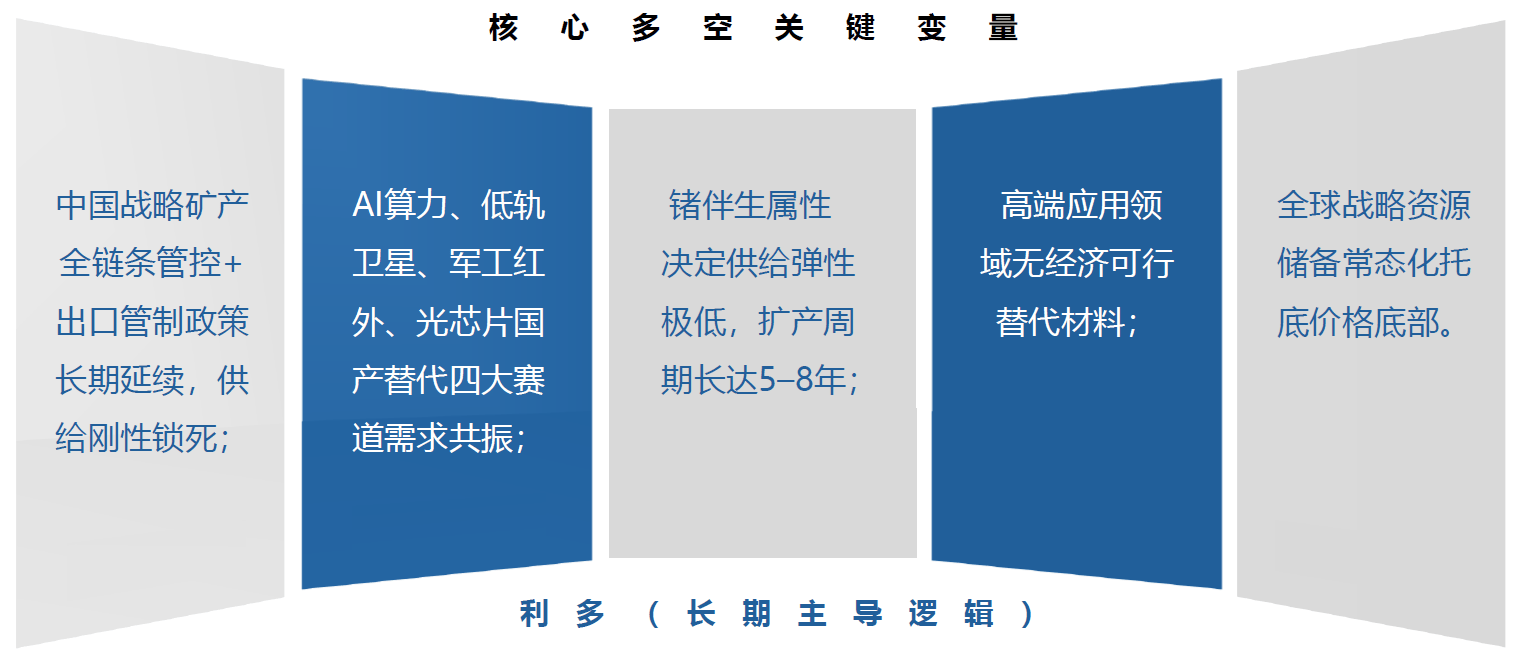

Yan Qing pointed out that the current germanium industry features a highly concentrated resource and supply structure, presenting rigid constraints. In terms of demand structure, domestic consumption in the infrared optics field (military night vision, thermal imaging, security, and autonomous driving) grew by 13% year-on-year in 2025; the optical fiber communication field (5G/data center optical modules and fiber preforms) saw an annual growth rate of about 10%; in the commercial aerospace and photovoltaic sectors, demand for germanium in low-orbit satellite solar cells is expected to become an emerging growth point in 2026; in the semiconductor field, germanium is used in SiGe chips, radiation detectors, and quantum computing, but China still lags in ultra-high-purity germanium purification technology. Due to the dual impact of tightening supply and surging demand, germanium prices have accumulated a 110% increase over the past two years, with a significant supply-demand gap in the market. As of mid-June 2026, the mainstream spot price of domestic 5N high-purity germanium ingots in East China ranged from 26,000 to 28,000 yuan/kg, an accumulated increase of over 85% from 15,000 yuan/kg at the end of 2025; the spot price on the European MB free market exceeded $6,000/kg, maintaining a price gap of more than double between domestic and international markets. Fiber-grade germanium tetrachloride saw a nearly 300% increase within the year, while 6N semiconductor-grade ultra-high-purity germanium rose by 55% to 75%. The new "Implementation Regulations of the Mineral Resources Law," effective June 15, classified germanium as a national-level strategic mineral, upgrading supply-side rigid constraints to a "national resource strategy." In 2026, global primary germanium production is estimated at 190 to 210 tons, with total demand at 230 to 250 tons, resulting in a supply-demand gap of 40 to 50 tons for the year, accounting for nearly 20% of total production. Domestic social circulating inventory stands at just over 30 tons, with smelters generally reluctant to sell and supporting prices.

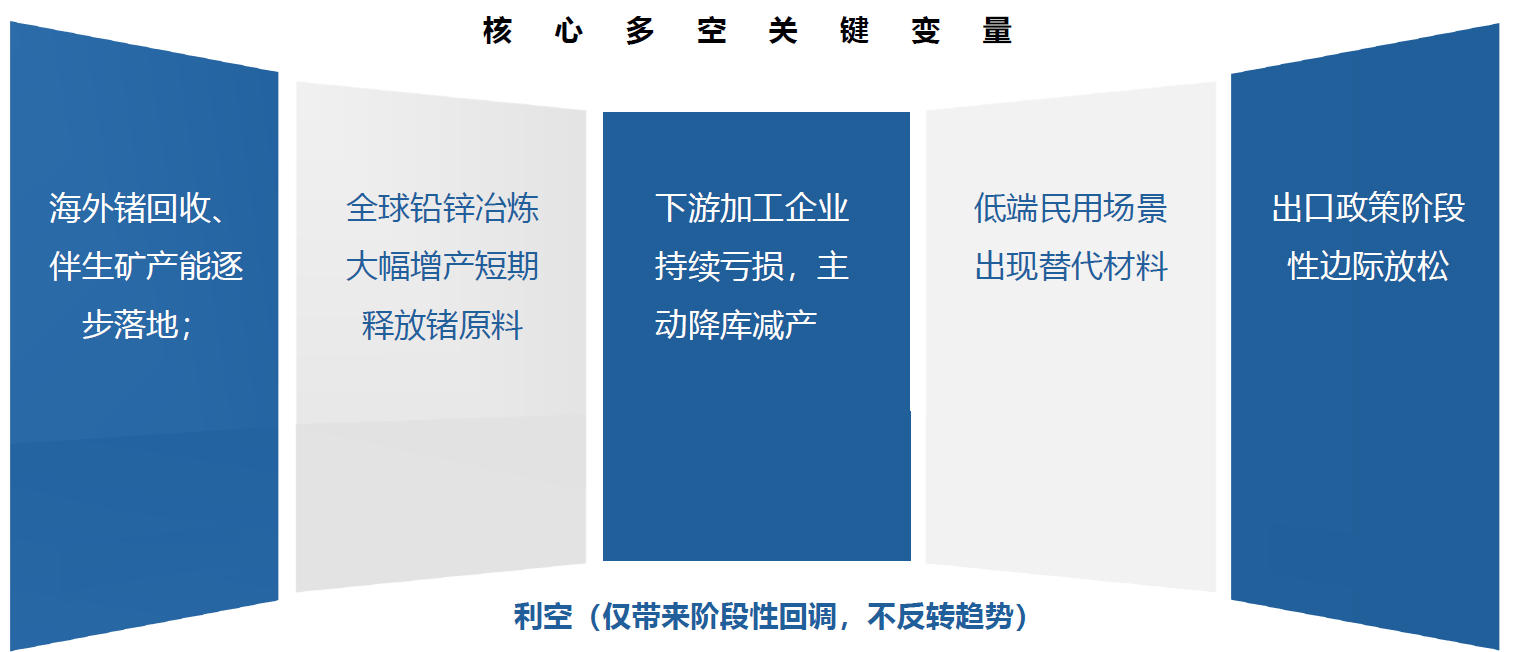

In the short term, supply-side rigid constraints remain unchanged. On the demand side, satellite photovoltaics represent the fastest-growing segment, with dense launches of low-orbit satellite constellations and the upgrade from 4-inch to 6-inch substrates increasing germanium usage per satellite by 50%, driving demand growth in this field to over 40% in 2026; military infrared demand is rigid with no substitution risk; optical fiber communication accounts for 40% of demand, with germanium tetrachloride as a fiber dopant having no economically viable alternative, leading to an annual demand growth rate of 20% to 30% in this field; in the semiconductor optical chip sector, the domestic substitution of indium phosphide high-speed optical chips is accelerating, and the iteration to 1.6T optical modules doubles germanium usage per module. In the short term, the operating center for domestic 5N germanium ingots is expected to be 26,000 to 28,000 yuan/kg, with the international market stabilizing above $6,000/kg, spot premiums expanding to 10%-15%, and potentially reaching $7,000/kg within the year. Factors such as concentrated maintenance shutdowns in lead-zinc smelting, production cuts and inventory reductions by downstream processing enterprises due to losses, and phased marginal easing of export quotas may cause periodic corrections, but the upward trend remains unchanged.

In the medium to long term, from 2027 to 2029, the price center will systematically rise, with the gap continuing to widen. On the supply side, overseas projects can only contribute an additional 10 to 30 tons before 2029, while domestic environmental protection and resource controls continue to tighten. Demand is expected to grow at a compound annual rate of 15% to 20%, with AI computing infrastructure, 6G optical fiber, and commercial aerospace entering large-scale construction phases. Institutions estimate that the global supply-demand gap will expand to 50 to 70 tons by 2027. At that time, the price center for domestic ordinary 5N germanium ingots will rise to 28,000 to 32,000 yuan/kg, with premiums for 6N and above electronic-grade and military-grade high-purity germanium continuing to widen; international prices will remain in the $6,000 to $8,000/kg range for the long term.

Yan Qing assessed that germanium ingots are in a major upward cycle characterized by short-term high-level fluctuations, medium-term center elevation, and long-term high-level divergence. The core driver has shifted from "export control event catalysis" to a triple underlying logic of "supply rigidity + industrial rigid demand + national strategy." Only after 2029, when overseas production capacity and recycling capacity are released intensively, will prices see a moderate correction, but resource scarcity and strategic attributes determine that the long-term price floor will be significantly higher than historical ranges. Risk disclaimer: The above is a deduction of industry supply-demand logic and does not constitute trading or investment advice; the small metals market has a small volume and is prone to sharp short-term fluctuations due to trade policies and concentrated stocking sentiment.

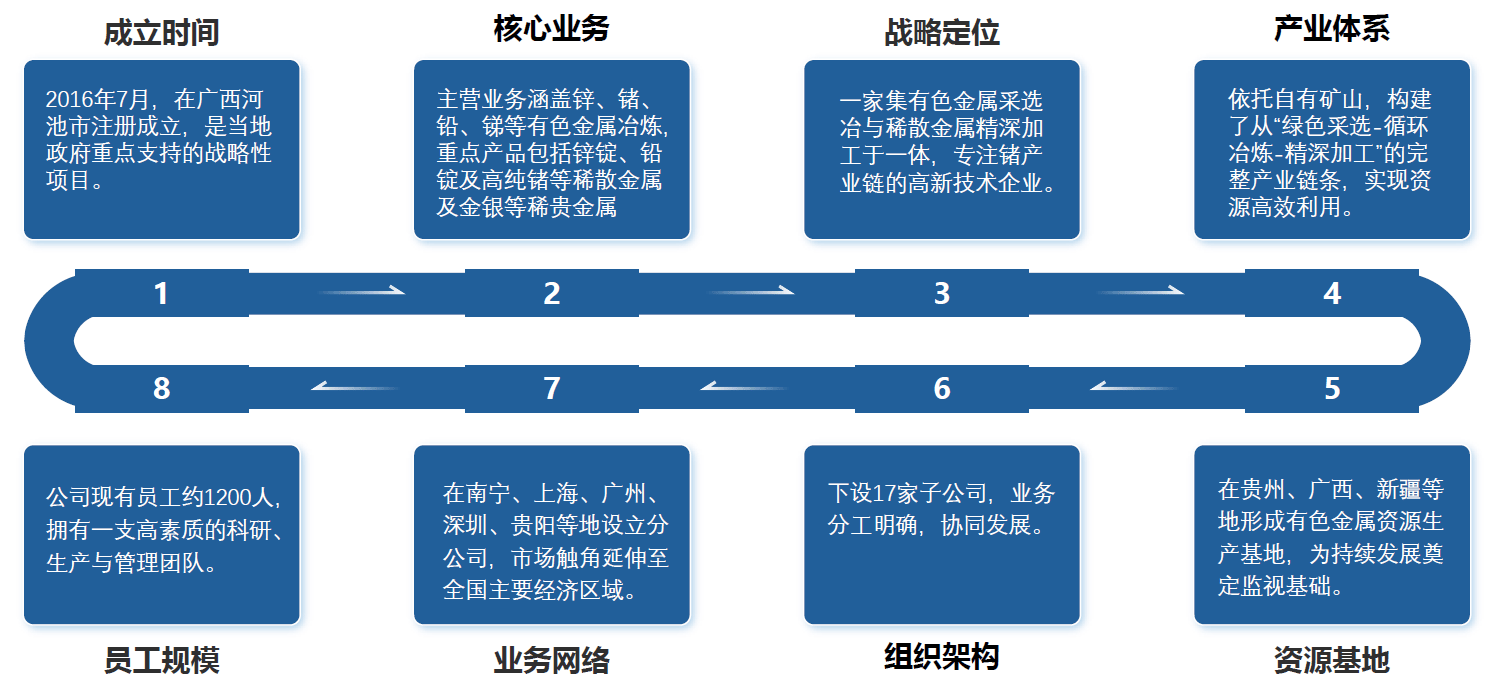

Guangxi Yusheng Germanium High-Tech Co., Ltd. is a high-tech enterprise focusing on rare and dispersed metals. Phase I of the project is located in Jinchengjiang District, Hechi City, Guangxi, with a total investment of 1.5 billion yuan, commencing production in October 2021, with an annual output of 100,000 tons of zinc ingots and 50 tons of high-purity germanium. Phase II of the project has a signed total investment of 3.5 billion yuan, planning to add an annual production capacity of 150,000 tons of zinc and 100,000 tons of lead-antimony, with an additional annual output value exceeding 7 billion yuan after full operation.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com