en.Wedoany.com Report, According to the SMM Steel Industry Chain Weekly Report, the ferrous metals market showed a pattern of rising and then falling back this week, and may continue to fluctuate at high levels in the short term. At the beginning of the week, the shift to coal-fired power generation in Asia due to tight natural gas supply, coupled with Indonesia's announcement to increase coal production and impose export taxes, drove up international coal prices, which transmitted to the domestic market and led the rise in coking coal and coke. Mid-week, changes in the Middle East situation and differing stances between the US and Iran led to market consolidation at high levels. In the latter half of the week, rumors about iron ore long-term contract negotiations weakened expectations of tightening supply, support from the cost side diminished, and prices retreated. In the spot market, speculative and procurement sentiment improved in the first half of the week, while rigid demand dominated in the latter half, with the futures-spot spread widening.

In terms of iron ore, prices rose and then fell back this week, significantly influenced by news flow. Looking ahead to next week, cyclone weather in Australia may reduce global shipments, while the resumption of blast furnaces supports increased hot metal production, suggesting demand may remain stable or slightly increase. However, risk factors such as the easing of Middle East conflicts and the finalization of long-term contract negotiations may weaken cost support. If these risks do not materialize, iron ore prices may still have room for a rebound. In the coke market, some steel mills plan to raise prices starting April 1, 2026, with wet-quenched coke increasing by 50 yuan/ton and dry-quenched coke by 55 yuan/ton. Coke plants are experiencing smooth shipments and low inventories, while rising costs enhance their willingness to raise prices. The resumption of production at steel mills is driving up hot metal output and increasing procurement willingness. Coking coal prices have stabilized and rebounded, with improved market sentiment. It is expected to operate strongly next week, and the first round of coke price hikes is anticipated to be implemented next week, indicating a short-term strong market.

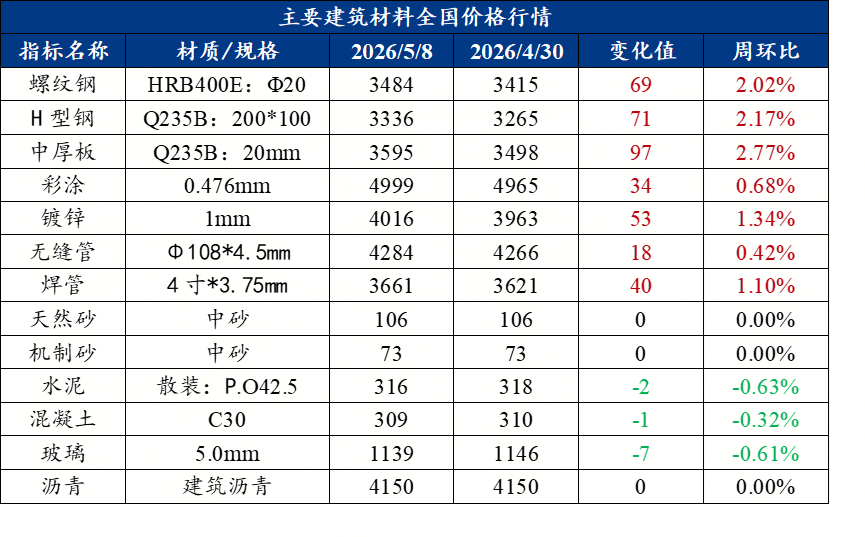

The fundamentals of the scrap steel market maintained a weak balance. Warmer weather and the resumption of processing enterprises increased supply, while the restart of electric arc furnace steel mills boosted demand. The operating rate of 50 electric arc furnace steel mills nationwide increased by 1.78% week-on-week to 40.42%. However, weak finished product markets are squeezing profits, leading companies to control procurement prices to protect margins. With both supply and demand increasing, prices are expected to fluctuate within a range next week. The average price of rebar this week was 3,145 yuan/ton, down 9 yuan/ton week-on-week. On the supply side, the resumption of blast furnaces and electric arc furnaces increased production, but profit pressures may slow the pace of output growth. On the demand side, some northern markets improved, but overall demand fell short of the same period last year, and inventory destocking was slower than expected. Market sentiment is pessimistic, with traders taking profits. If destocking remains slow, some regions may cut prices to sell off goods. Prices are expected to operate weakly in the short term.

Hot rolled coil futures rose first and then weakened this week, with the main contract closing at 3,299, down 0.27% on the day. Spot prices fluctuated by 10-20 yuan/ton, with average trading volume. News about iron ore negotiations affected ore prices, while coking coal and coke rose and fell back with crude oil fluctuations. Hot coil production fluctuated within a range, while downstream demand was lukewarm with low procurement willingness. SMM data shows that total hot coil inventory this week was 6.7821 million tons, a decrease of 89,100 tons week-on-week. Social inventory saw overall destocking but with regional divergence. Inventory pressure remains higher than in previous years, and fundamentals lack highlights. Prices are expected to consolidate sideways next week, following the cost side. Overall, the ferrous metals market, under the influence of raw material-side disturbances, may continue its high-level fluctuating trend in the short term.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com