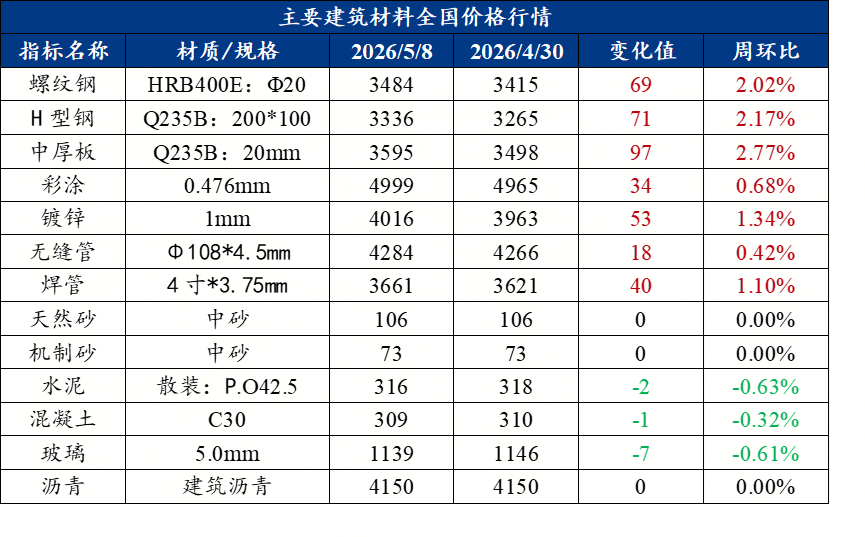

en.Wedoany.com Reported - Recently, the building raw materials market has shown a trend of narrow fluctuations, with the average price of rebar rising slightly month-on-month. Demand for cement and concrete is slowly recovering, but the capital arrival rate has declined month-on-month. The overall market sees strong expectations coexisting with weak reality. It is expected that this week, steel prices will remain high and volatile, cement prices will gradually stabilize, and the concrete market will operate weakly and steadily.

In terms of construction steel, the national average price for rebar was reported at 3,490 yuan/ton, up 13 yuan/ton week-on-week. Production volume was 2.014 million tons, an increase of 47,500 tons month-on-month but a decrease of 251,300 tons year-on-year. Factory inventories decreased by a cumulative 123,000 tons, with the East China, South China, and Southwest regions leading the decline. The contradiction between market supply and demand is not prominent, and sentiment is driving prices to operate on the stronger side. It is expected that this week, finished steel prices will remain high and volatile, supported by production controls and domestic-overseas price spreads.

Overall prices for medium and heavy plate were on the stronger side, with a national average of 3,604 yuan/ton, up 14 yuan/ton week-on-week. Steel mills have full order books for specialized plates used in shipbuilding and wind power, while general-purpose plate resources are tight. End-user procurement is mainly based on rigid demand. Total social inventory was 2.5018 million tons, a decrease of 68,900 tons month-on-month. It is expected that medium and heavy plate prices will continue to fluctuate with an upward trend this week.

In the cement market, the national average price remained flat. Shipment volume was 2.9145 million tons, up 7.5% month-on-month but still down 18.7% year-on-year. Direct supply of cement for infrastructure projects reached 1.75 million tons, up 6.7% month-on-month. The clinker inventory-to-capacity ratio was 58.51%, up 0.77 percentage points month-on-month, indicating sustained inventory pressure. As staggered peak production advances, supply will contract. It is expected that cement prices will gradually stabilize this week, with North China and Central China regions likely to see slight increases of 5 to 10 yuan/ton.

The capacity utilization rate in the concrete market was 6.89%, up 0.36 percentage points week-on-week. Shipment volume was 1.3799 million cubic meters, an increase of 5.57% week-on-week but a decrease of 14.57% year-on-year. Regional divergence is evident, with shipment volumes in East China, South China, and Central China all rebounding month-on-month, but capital and construction progress are still constraining demand release. It is expected that the concrete market trend this week will mainly involve testing lower prices while remaining stable, with stability in areas with localized rigid demand.

According to a survey by Bainian Construction, as of May 12, the capital arrival rate for sample construction sites was 54.96%, down 0.4 percentage points from the previous period. Apparent consumption of the five major steel product categories increased by 8.4% week-on-week, with construction steel consumption up 19.7% and flat steel consumption up 2.6%. However, the growth rate of construction steel procurement volume slowed in May, with only the Southwest region showing a month-on-month increase exceeding 10%, while increases in other regions were below 10%. Overall, the pace of demand recovery is slow, and the market still faces adjustment pressure going forward.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com