en.Wedoany.com Reported - The countdown is on for U.S. renewable energy project tax credit policies, putting pressure on clean energy buyers as Power Purchase Agreement (PPA) prices are poised to surge. A market insight report from LevelTen Energy warns that the July 4 "tax credit cliff" will rapidly drive up PPA contract offers, urging corporate procurement managers to accelerate action to avoid soaring project costs.

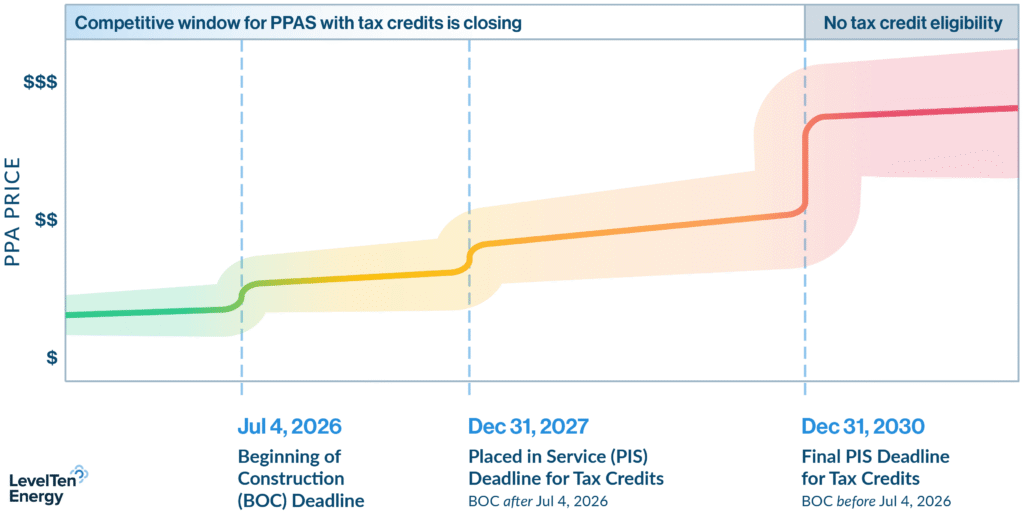

Nearly a year has passed since the Trump administration pushed through the "One Big Beautiful Bill Act" (OBBBA), which sets an aggressive timeline for phasing out federal wind and solar tax incentives. According to the bill's structural guidelines, utility-scale projects must begin construction by July 4, 2026, or be placed in service (PIS) by December 31, 2027, to qualify for full federal tax credits. All projects under construction must achieve PIS by December 31, 2030, to be eligible for remaining partial credits.

Although a recent ruling by a U.S. district court supports an alternative commencement test—allowing developers to qualify by demonstrating they have incurred 5% of total project costs—LevelTen warns that time constraints and execution capacity bottlenecks will prevent most developers from leveraging this workaround. The looming deadline means the pool of safe harbor projects eligible for tax credits is rapidly drying up.

With the fixed supply of mature assets being snapped up, market leverage is expected to shift significantly from buyers to developers. LevelTen's report shows that since last July, 50% of projects listed on its proprietary "Most Valuable Projects on the Market tracker" have been locked into exclusive agreements. "Supply is shrinking weekly, and prices are expected to rise unidirectionally through 2028 and beyond," warned report author Sarah Wolf. "Signing a contract today with a tax credit-eligible project means locking in terms that reflect current economic conditions before the no-tax-credit premium becomes the new normal in the PPA market."

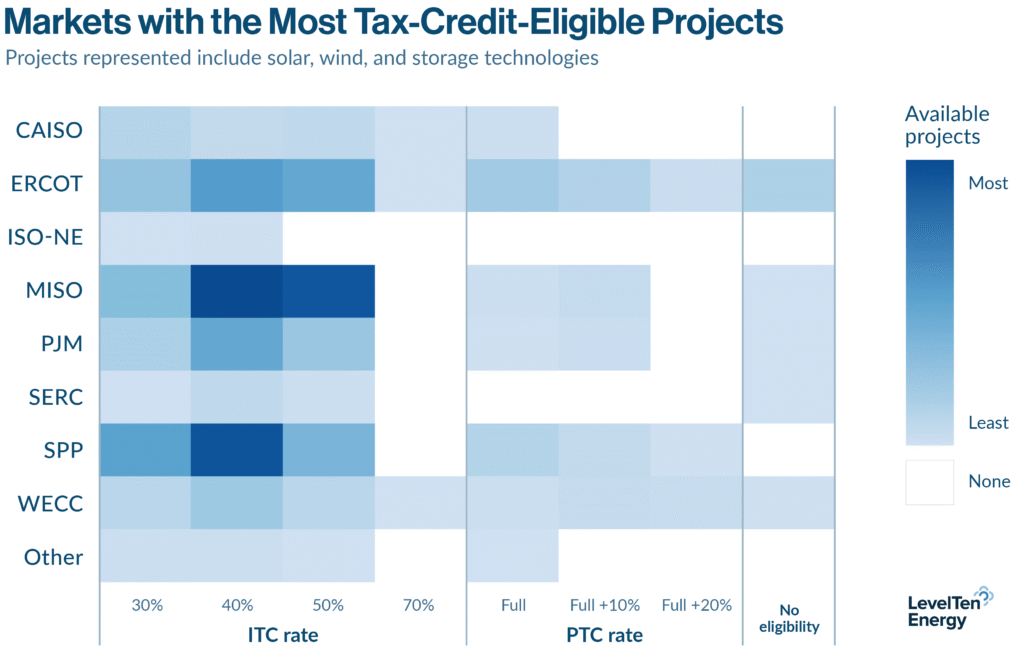

The report notes that MISO and SPP have emerged as key hotspots for remaining tax credit-eligible projects. In SPP, wind assets continue to maintain a significant Production Tax Credit (PTC) presence; ERCOT shows a strong mix of Investment Tax Credit (ITC) and PTC-eligible projects, reflecting its hybrid wind and solar landscape. Across nearly all major Independent System Operators (ISOs), developers are actively targeting additional tax incentives to optimize project finances. As developers prioritize marketing remaining safe harbor assets, actual pricing data for projects entirely without tax credits is scarce, but LevelTen's early transaction modeling reveals the post-cliff outlook: after OBBBA passed in late 2025, PPA offers for top-tier projects immediately rose 7% within a single quarter. Looking ahead to the expiration of the ITC/PTC framework, some developers are modeling baseline PPA price increases of 40% to 50% across all ISOs. In ERCOT, the premium is more severe, with early transaction data suggesting that without tax credits, PPA prices could more than double—soaring 120%, or an incremental cost increase of $66.21 per megawatt-hour.

Despite tightening supply, corporate buyers may hold a temporary competitive advantage over large tech hyperscalers. Data from the Corporate Energy Buyers Association (CEBA) shows that although over 13 gigawatts of clean energy have been contracted year-to-date, the number of corporate buyers has dropped 40% over the past year. This decline highlights a market dominated by large data center developers executing hyperscale PPAs. However, due to stringent regional grid constraints, certification capacity requirements, and precise colocation demands, data center development faces inherent geographic limitations. Beyond these dense data center zones, LevelTen indicates that high-quality, tax credit-eligible renewable energy assets remain accessible to standard corporate buyers. As the July 4 tax cliff marks the end of the current tax era, buyers who can lock in remaining safe harbor assets before they vanish from the market will gain a first-mover advantage.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com