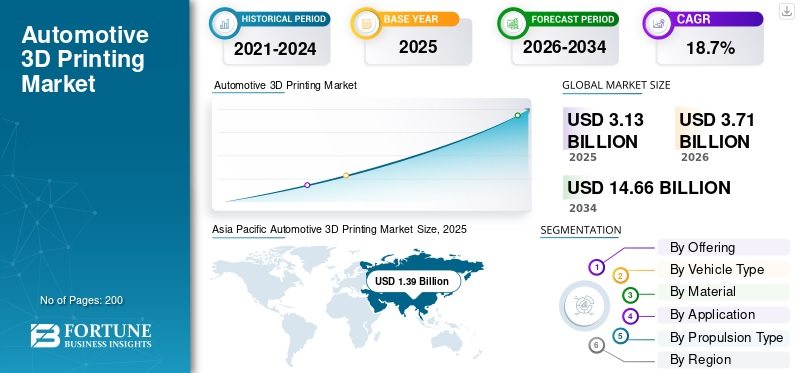

en.Wedoany.com Reported - A report by market research firm Fortune Business Insights shows that the automotive 3D printing market is entering a period of rapid growth. Driven by factors such as rapid prototyping, enhanced design flexibility, and optimized costs for small-batch production, the market size is projected to grow from $3.13 billion in 2025 to $14.66 billion by 2034, with a compound annual growth rate (CAGR) of 18.7% during the forecast period.

The report indicates that 3D printing is increasingly integrating with digital manufacturing systems such as CAD, digital twins, and Industry 4.0 platforms, enabling seamless connection from design to production. Automakers are enhancing quality control and efficiency through connected manufacturing environments, propelling 3D printing to become one of the key technologies for smart factories. End-use part manufacturing is the fastest-growing application segment, with an expected CAGR of 20.0%. As material strength and process reliability improve, 3D printing is moving from prototyping to small-batch, customized production stages.

In terms of product composition, hardware (printers, materials, post-processing systems) dominated the market in 2025, benefiting from sustained investment in industrial-grade equipment and technological upgrades. Software is the fastest-growing segment, with a CAGR of 20.2%, reflecting the increasing importance of simulation optimization, workflow management, and digital twins in manufacturing processes. Regarding materials, polymers are the most widely used, applied in prototyping, interior parts, and functional testing; metals lead in growth rate (CAGR 19.2%), driven by demand for lightweight structural components and powertrain parts in electric vehicles.

By powertrain type, internal combustion engine vehicles still held the largest market share in 2025, due to the vast existing vehicle fleet and platform upgrade needs. Electric vehicles represent the fastest-growing segment (CAGR 19.5%), with platform development, battery component prototyping, and lightweighting needs accelerating 3D printing penetration. Regionally, the Asia-Pacific region held a 44.41% global market share in 2025, with China leading development through high production volumes, rapid electric platform updates, and a dense supply chain ecosystem. India is the fastest-growing country (CAGR 21.2%), with OEMs and startups actively adopting 3D printing to shorten development cycles and reduce prototyping costs. Europe and North America rank as the second and third largest markets, with Germany and the U.S. maintaining leadership within their respective regions.

The report notes that the market is in a state of moderate competition, with key players including Stratasys, 3D Systems, EOS, HP, Desktop Metal, GE Additive, Materialise, Renishaw, SLM Solutions, and others. These companies are building competitive barriers by improving printing speed, precision, and material compatibility, offering integrated "hardware + materials + software + post-processing" solutions, and establishing strategic partnerships with automotive OEMs. The report concludes that automotive 3D printing is shifting from a "prototyping tool" to a "manufacturing tool." Under the trends of electrification, lightweighting, and customization, its role will evolve from an R&D aid to a core link in the supply chain, with standardization, quality certification, and software integration capabilities becoming key to future competition.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com