en.Wedoany.com Reported - Barry O'Shea, CEO of Highland Copper, recently explained that the copper market is entering a new phase shaped by the combined influence of geopolitics, energy policy, and digital infrastructure investment, with its strategic importance surpassing its traditional role in industrial cycles. Highland Copper is advancing the fully permitted Copperwood copper development project in Michigan's Upper Peninsula, and O'Shea's perspective combines the macro backdrop shaping the industry with the practical operations of a development-stage mining company.

Traditional drivers of copper demand, including urbanization, GDP growth, and industrial expansion, remain intact. On top of this, national security considerations and the accelerated buildout of energy and digital infrastructure are creating a new layer of demand. The U.S. Department of Defense has identified copper as the second most widely used metal in defense applications. Meanwhile, the electrification of transportation and energy systems, grid modernization, and the construction of AI data centers each generate demand scales that did not exist a decade ago. Electric vehicles and alternative energy systems use roughly three to four times the copper of their conventional counterparts, and data centers also require substantial copper in their physical infrastructure. O'Shea noted that copper's growing strategic significance is tied to supply vulnerabilities exacerbated by limited U.S. domestic production relative to national demand, with import patterns becoming unreliable due to shifting geopolitical relationships. The U.S. policy response has focused on incentivizing domestic development through grants and concessional debt instruments.

The pace at which supply can actually meet demand growth is a critical constraint. Mining projects in the U.S. typically take about 20 years to go from the first exploration drill to full production, high-grade deposits are increasingly depleted, and new projects often involve lower-grade ore bodies in more complex operating environments. O'Shea believes that even with incentive prices, supply-demand dynamics will remain tight. Policy reforms may marginally shorten timelines, but the structural lag caused by long capital cycles in mine development and multi-year regulatory processes is difficult to change quickly. Companies with late-stage, permitted projects are well-positioned to benefit from a market environment where new supply cannot be easily or quickly generated.

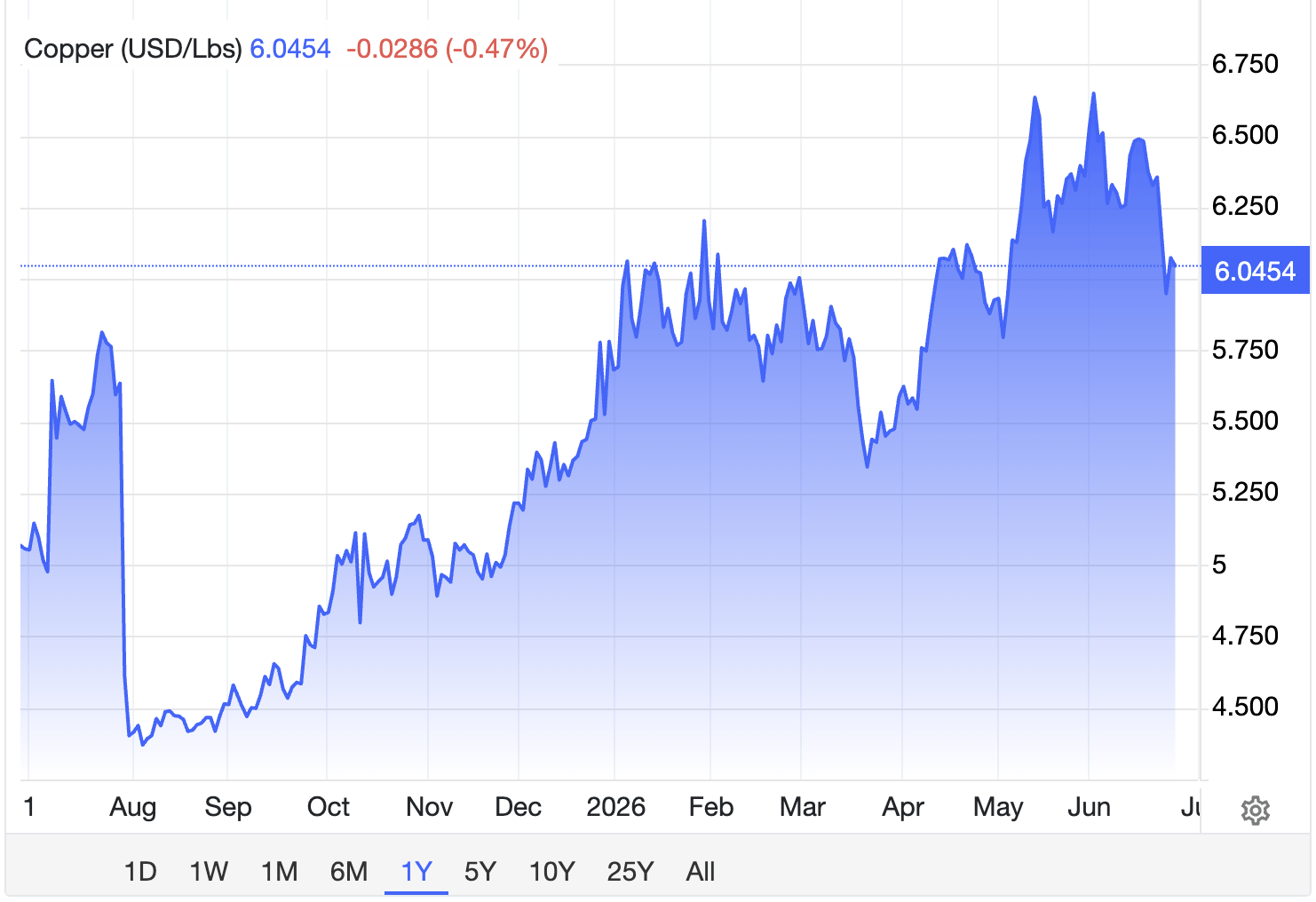

The Copperwood project is located in a historic mining district in Michigan's Upper Peninsula with established infrastructure. Operating on private land, it is exempt from the full federal National Environmental Policy Act review process, an operational advantage. Regulatory oversight is handled by the state of Michigan, which has stringent but workable environmental standards. The project has received 22 resolutions of support from local governments, townships, and counties, and has earned its social license to operate through early site work and reclamation activities. The project's capital expenditure is approximately $400 million, with a copper grade of 1.5%. Highland Copper expects to complete an updated feasibility study and make a formal construction decision in the first quarter of 2027, using a long-term copper price assumption of $5 per pound. At the time of the interview, the spot copper price was around $6 to $6.50 per pound.

The capital environment for domestic copper development has improved significantly. Highland Copper has applied for grants and debt financing from the Department of Defense and the Export-Import Bank of the United States, and has engaged with the White House Office of Strategic Capital and the National Energy Dominance Council. The company has been included alongside major operators like Rio Tinto in White House publications, identified as a project critical to U.S. domestic copper supply. On the private side, mining stocks are becoming more attractive to institutional capital, with many mining companies improving their balance sheets. Strategic capital may also come from large technology companies with significant copper demand, seeking to independently secure their supply chains.

Market consensus on the long-term copper price has risen from $3.75 to $4 per pound two to three years ago to $5 per pound, supported by spot prices of $6 to $6.50 per pound. O'Shea sees $5 as a reasonable floor for project evaluation. He draws an analogy to the gold industry, noting that companies that maintain financial discipline during periods of weak prices can generate strong cash flows when prices rise. O'Shea stated that the market has not yet fully priced in the scarcity of copper supply.

The interview content offers valuable insights for investors evaluating the copper industry. Copper metal faces a structural supply deficit that cannot be quickly resolved by price increases alone. Demand is being driven by multiple concurrent themes, including defense, electrification, grid modernization, and AI infrastructure, elevating its strategic importance. For development-stage companies with permitted projects in stable jurisdictions, improved government financial support, rising institutional interest, and a more favorable long-term price environment may represent significant opportunities, with the key lying in execution and overcoming the engineering, financing, and construction challenges between advanced development assets and cash-flowing mines.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com