en.Wedoany.com Reported - China's CRIC Research Center recently released a special research report titled "Summary and Outlook of China's Real Estate Market in the First Half of 2026 (Policy Chapter)." The report shows that housing prices in core cities have shown signs of stabilization, but the industry still faces challenges such as slower-than-expected market confidence recovery and high inventory in third- and fourth-tier cities. The second half of the year will enter a critical phase of "policy implementation and efficiency release."

The report points out that in the first half of 2026, China's central real estate policies focused on institutional precedence, two-way supply-demand adjustment, and structural financial support. A long-term framework for high-quality real estate development during the "15th Five-Year Plan" period was established from four dimensions: top-level institutional design, demand-side burden reduction, supply-side coordination of existing and new stock, and special fund support. The government work report released on March 5 made systematic arrangements for real estate, mentioning "destocking" for the first time in a decade and including "encouraging the acquisition of existing commercial housing primarily for affordable housing" in the report for the first time. The "15th Five-Year Plan" outline dedicated an independent chapter to real estate for the first time, explicitly proposing "promoting the sale of existing homes in an orderly and forceful manner." On May 22, the State Council issued the first national-level "Urban Renewal '15th Five-Year Plan'."

On the demand-side policy front, measures focused on reducing the cost of home purchases and ownership. The interest rate on existing provident fund loans was lowered from January 1, with the rate for first-home loans over five years reduced to 2.6%. The minimum down payment for commercial housing purchase loans was adjusted from 50% to no less than 30%. The tax refund policy for individual housing trade-ins was extended until the end of 2027. Supply-side policies featured "controlling new supply and revitalizing existing stock," with the Ministry of Natural Resources clarifying that new construction land would, in principle, not be used for commercial real estate development. On the financing side, loans for projects on the "whitelist" can be extended for up to five years, and the universal "three red lines" regulatory oversight was phased out. The journal *Qiushi* published articles on January 1 and June 18, reaffirming the foundational role of real estate in the national economy and proposing "accelerating the repair of household balance sheets."

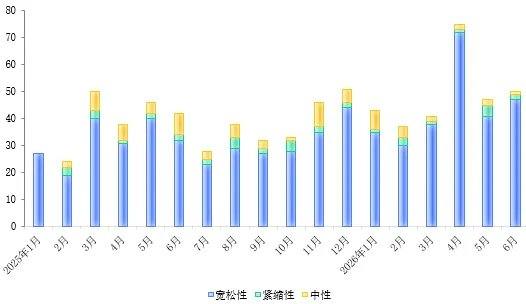

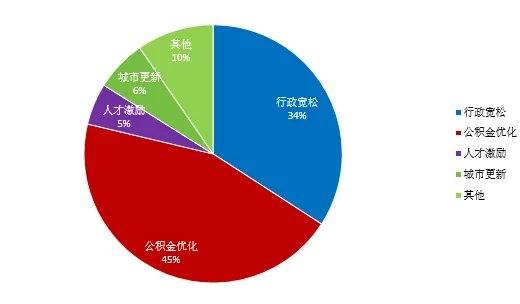

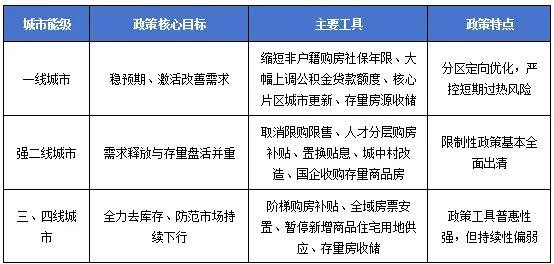

Regarding local policies, a total of 263 easing measures were introduced in the first half of 2026, accounting for 89.8% of all policies. Policy focus was concentrated on three main areas: provident fund optimization, home purchase subsidies and trade-in incentives such as "old-for-new" schemes, and urban renewal and existing stock revitalization support. First-tier cities had distinct policy emphases: Shenzhen's "April 29 Policy" lifted purchase restrictions in three core districts, Guangzhou's "Eight Measures of Sui" had the broadest coverage, Shanghai introduced a new "Seven Measures of Hu," Tianjin fully abolished purchase and sale restrictions in April, and Suzhou implemented relatively strong provident fund optimization rules. Third- and fourth-tier cities aimed primarily at reducing inventory, with state-owned asset platforms in over 80 cities across China initiating bulk listings and acquisitions of existing housing stock. As of early June, more than 70 cities had launched centralized acquisition programs, with over 120,000 units registered for intent and more than 18,000 units completing transfer and signing.

Regarding policies for the second half of the year, the report expects limited room for further LPR reductions, with monetary policy support shifting from "rate cuts and profit concessions" to "precise drip-feeding through structural tools." PSL and affordable housing relending are likely to become the primary policy vehicles. The acquisition of existing housing stock will enter a substantive purchase phase, with pricing mechanisms and housing suitability being key implementation bottlenecks. On provident fund system reform, the official revised regulations are expected to be implemented in the second half of the year. Policy focus in first-tier and core second-tier cities will shift from "stabilizing expectations" to "promoting improvement," while ordinary second-tier and third- and fourth-tier cities will continue to prioritize "destocking and risk prevention."

The report concludes that in the first half of 2026, China's real estate policies completed a systematic upgrade from "emergency corrections" to "institutional consolidation," marking a significant departure from the demand-stimulus-focused logic of 2022 to 2024. The core theme for the second half of the year revolves around "whether the established institutional framework can be effectively implemented." Indicators such as the conversion rate of acquisition and signing, the commencement rate of urban renewal projects, and marginal changes in the inventory destocking cycle will determine the actual level of policy efficiency release.