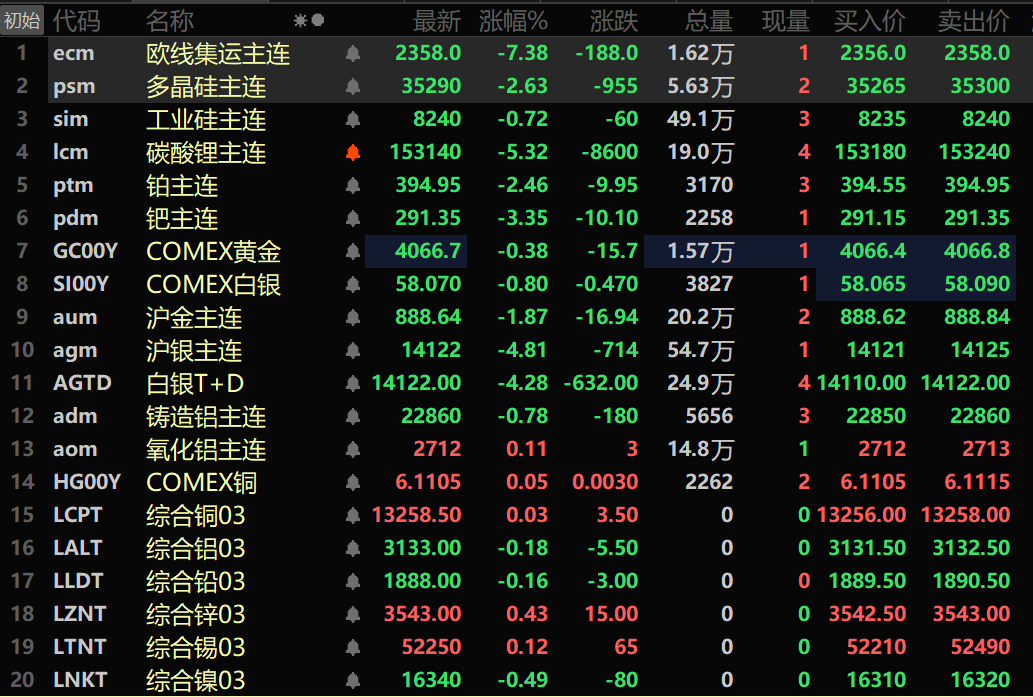

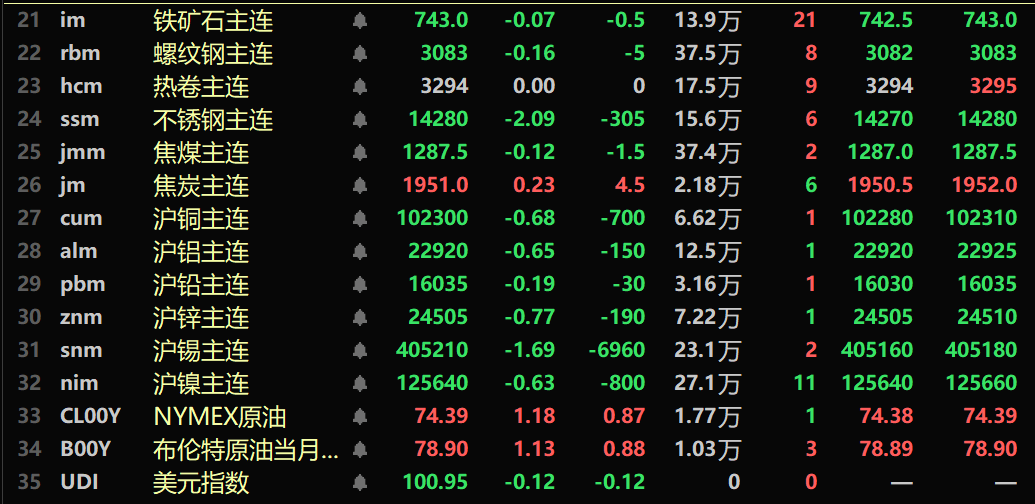

en.Wedoany.com Reported - As of the midday close on July 9, China's base metal futures broadly declined, with Shanghai Tin leading the losses, down 1.69%, while Shanghai Copper and Shanghai Aluminum fell 0.68% and 0.65%, respectively. Shanghai Zinc, Shanghai Nickel, and Shanghai Lead dropped 0.77%, 0.63%, and 0.19%, respectively. Among other varieties, the main contract for Lithium Carbonate plunged 5.32%, Polysilicon futures fell 2.63%, and Industrial Silicon declined 0.72%. Most ferrous metals turned lower, with Stainless Steel falling significantly by 2.09%, Rebar edging down 0.16%, and Hot Rolled Coil flat at 3,294 yuan per ton. Coking coal and coke diverged, with the main contract for Coking Coal down 0.12% and the main contract for Coke up 0.23%.

In overseas metals, as of 11:41 Beijing time, the London Metal Exchange (LME) saw mixed results. LME Zinc and LME Tin rose 0.43% and 0.12%, respectively, while LME Copper edged higher. LME Aluminum, LME Lead, and LME Nickel fell 0.18%, 0.16%, and 0.49%, respectively.

In precious metals, as of the same time, COMEX gold and silver futures fell 0.38% and 0.8%, respectively. China's main Shanghai Gold contract declined 1.87%, and the main Shanghai Silver contract fell 4.81%. The main futures for Platinum and Palladium dropped 2.46% and 3.35%, respectively. Additionally, the main contract for Europe-bound container shipping closed at 2,358 points at midday, down 7.38%.

In the spot market, Guangdong No. 1 electrolytic copper spot quotes for the current month contract showed premium copper at a premium of 100 yuan per ton, up 10 yuan per ton from the previous trading day; standard copper at a premium of 40 yuan per ton, up 20 yuan per ton; and wet-process copper at a discount of 30 yuan per ton, up 20 yuan per ton. The average price of Guangdong No. 1 electrolytic copper was 102,475 yuan per ton, down 430 yuan per ton from the previous trading day; the average price of wet-process copper was 102,375 yuan per ton, down 425 yuan per ton. Spot market feedback indicated that Guangdong inventories have declined for six consecutive days, mainly due to persistently low arrivals.

On the macroeconomic front, data from the National Bureau of Statistics showed that in June 2026, the national Consumer Price Index (CPI) rose 1.0% year-on-year, with urban areas up 1.0% and rural areas up 0.8%; food prices fell 1.6%, while non-food prices rose 1.5%. The Producer Price Index (PPI) rose 4.1% year-on-year and fell 0.3% month-on-month. The purchasing price index for industrial producers rose 6.4% year-on-year and fell 0.2% month-on-month. Dong Lijuan, chief statistician of the Urban Department of the National Bureau of Statistics, interpreted the above data. On the same day, the People's Bank of China conducted a net withdrawal of 278.5 billion yuan through a 10 billion yuan 7-day reverse repurchase operation.

The U.S. Dollar Index edged down 0.12% to 100.95. Minutes from the Federal Reserve's June meeting showed officials expressed concerns about upside risks to inflation. The minutes noted that at the June 16-17 meeting, a few participants saw a case for an immediate rate hike, but "most participants" believed there were scenarios where inflation would fall back to the Fed's 2% target on its own, while others argued inflation would remain persistently high. "Almost all" participants holding the latter view believed a rate hike would be necessary if such a scenario materialized. Ultimately, "all participants" supported keeping interest rates unchanged. According to CME's FedWatch data, the market expects a 69.0% probability that the Fed will keep rates unchanged in July, with a 31.0% probability of a cumulative 25-basis-point hike; by September, the probability of keeping rates unchanged is 31.1%, with a 51.9% probability of a cumulative 25-basis-point hike and a 17.0% probability of a cumulative 50-basis-point hike. Additionally, Fed Chairman Kevin Warsh will testify before the House Financial Services Committee and the Senate Banking Committee on July 14-15, respectively, on the semi-annual monetary policy report.

In the crude oil market, escalating tensions in the Middle East sparked concerns over supply disruptions, extending oil price gains for a second consecutive trading day. As of 11:41, U.S. crude oil and Brent crude oil futures rose 1.18% and 1.13%, respectively. Ship tracking data showed that traffic through the Strait of Hormuz had nearly ground to a halt, with observable transits mainly concentrated on routes near the northern part of the waterway approved by Iran, while the U.S.-backed Oman corridor remained quiet. Kpler data showed that in the three weeks since the U.S. and Iran reached a provisional agreement to reopen the Strait of Hormuz, the average daily transit volume of commodity carriers was 34 vessels, peaking at 59 on June 24. Goldman Sachs expects that if the 60-day negotiations continue and Iranian oil waivers are restored, Persian Gulf oil flows will recover by the end of July, requiring an additional 6.6 million barrels per day of throughput through the Strait of Hormuz. If negotiations collapse and tanker attacks escalate, coupled with a potential U.S. blockade on Iranian oil, Persian Gulf flows could decline further.