en.Wedoany.com Reported - CATL's Jianxiawo lithium mine in Jiangxi, China, has obtained a safety production permit and resumed operations in August 2025 after an 11-month shutdown. The mine produces approximately 46,000 metric tons of lithium carbonate equivalent annually, accounting for 3% of global supply in 2025.

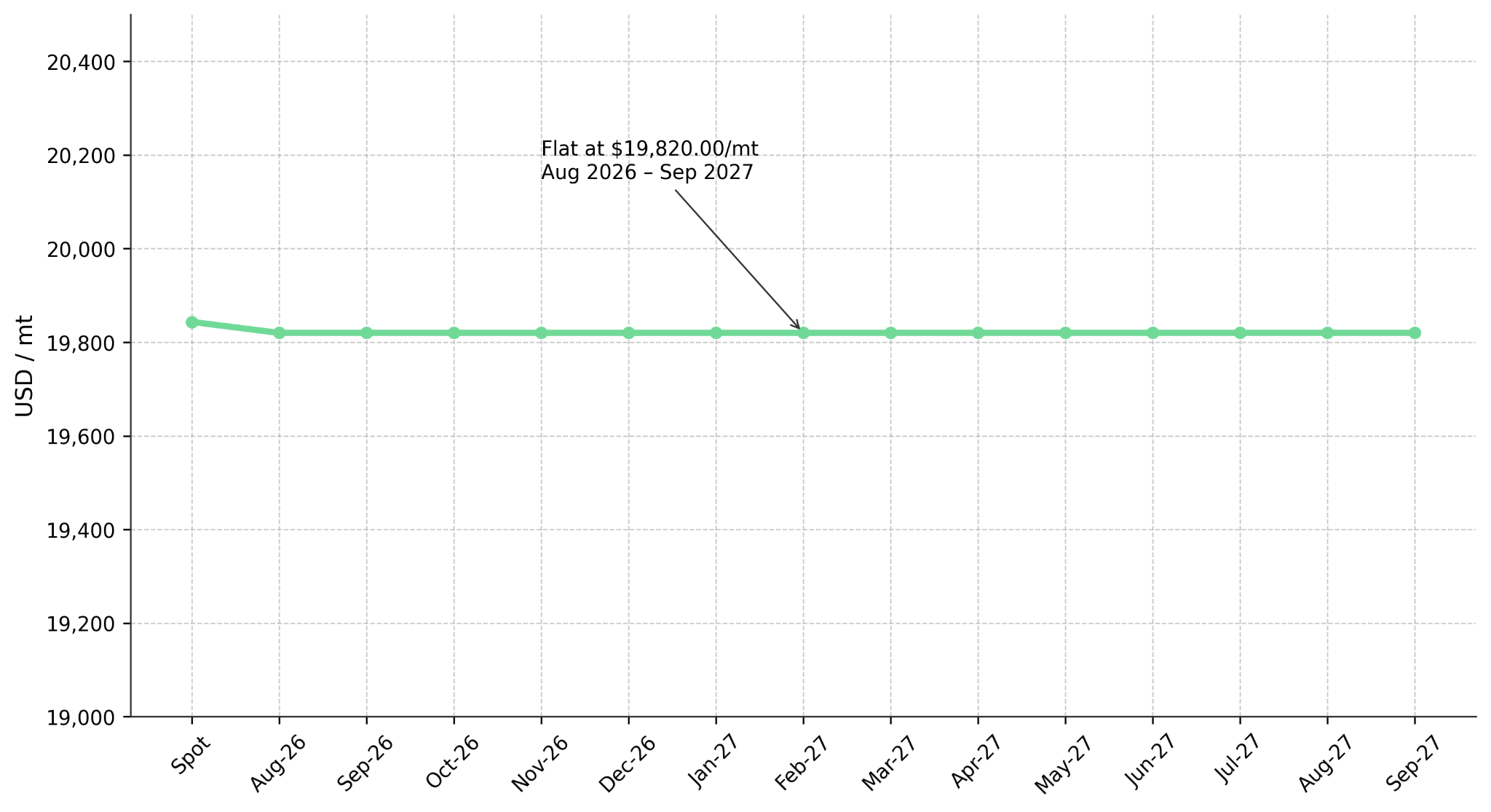

The LME lithium hydroxide CIF closing price stood at $19,843.48 per metric ton, up 0.61%. Every contract from August 2026 to September 2027 remained flat at $19,820.00 per metric ton, indicating that the market does not expect significant lithium price volatility over the next 14 months.

The $23.48 spot-to-forward spread shows minimal pricing differences between current and future lithium prices, failing to reflect term premiums or backwardation, suggesting the market is not pricing in a lithium price surge due to supply disruptions. CME lithium hydroxide CIF CJK futures are cash-settled based on the monthly average of Fastmarkets' lithium hydroxide price assessment, serving as a benchmark for hedging lithium price risk. Only three contracts were traded with no options activity, indicating limited hedging demand. Lithium prices remain dominated by the spot market and LME forward market, with low futures trading volumes and a flat forward curve, implying the market does not anticipate significant lithium price fluctuations over the next 14 months.

The Jianxiawo mine's permit is valid until February 2028, reducing the risk of another shutdown. During the 11-month shutdown, global supply was cut by 3%, but the flat forward curve shows the market does not expect tight supply to drive prices higher. The shutdown in August 2025 briefly boosted lithium futures and lithium mining stocks, while the resumption of production has eliminated this supply disruption. The flat forward curve through September 2027 indicates that a lithium price recovery requires stronger demand, Chinese policy support, or supply disruptions in other regions to sustain it.