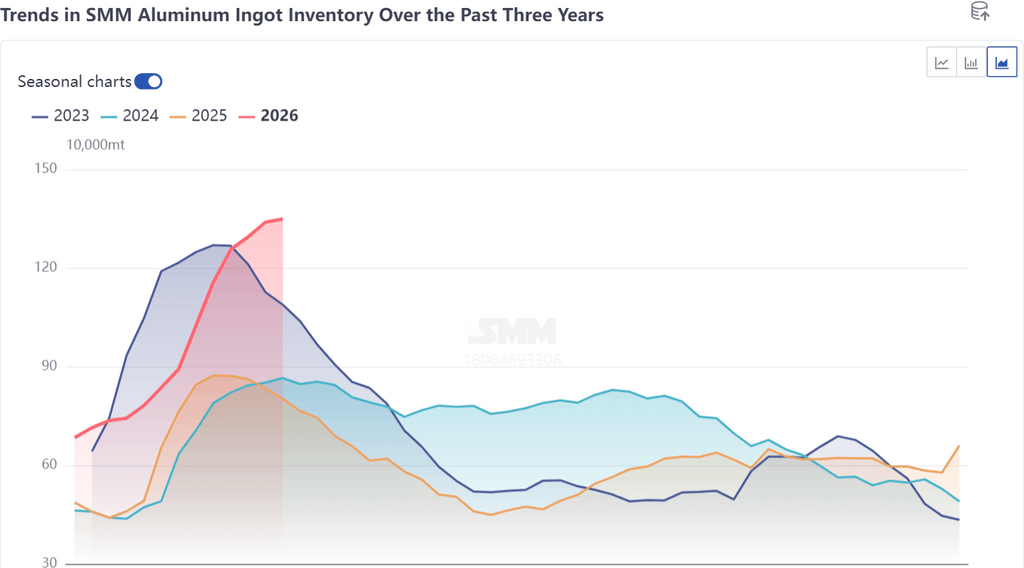

en.Wedoany.com Report on Mar 30th, In the second half of March, regional divergence in China's aluminum market intensified, with East China and South China showing stark differences in inventory trends and spot price spreads. The nationwide accumulation of aluminum inventory is nearing its end, with pressure easing in East China. However, aluminum ingot inventory in South China unexpectedly increased against the trend, causing the Guangdong-Shanghai aluminum ingot price spread to widen to nearly three digits.

According to SMM spot monitoring data, as of this Thursday, South China aluminum ingots were at a discount of 180 yuan/ton to the SHFE aluminum 2604 contract, with the Guangdong-Shanghai price spread at -90 yuan/ton. The total aluminum ingot inventory in major consumption areas nationwide was 1.349 million tons, increasing by only 10,000 tons week-on-week, while weekly outbound volume rose significantly by 30,000 tons to 128,100 tons week-on-week. South China's aluminum ingot inventory increased to 370,000 tons, exceeding the expected peak by 20,000 tons, becoming a focal point in the market.

The core reasons for the abnormal accumulation of aluminum ingot inventory in South China include concentrated shipments from southwestern sources, delayed pickups of long-term contract cargoes due to high freight rates, and the concentrated arrival of Russian aluminum shipments by sea. Aluminum plants in Yunnan and Guangxi initiated a concentrated shipment mode for their plant inventories in the second half of March, flooding the South China market with a large volume of supply. Simultaneously, road freight rates remained high, prompting buyers to delay pickups to reduce costs. As settlement dates approached, they were forced to concentrate pickups, with undigested supplies entering warehouses. The concentrated arrival of imported cargo further pushed up inventory, creating a triple supply resonance.

This week, trading sentiment in the South China spot market stabilized. Suppliers showed strong price support intentions, while downstream processing enterprises were highly motivated to purchase and replenish stocks at low prices. However, influenced by inventory accumulation and ample circulating supply, traders pressed for lower purchase prices, and warehouse delivery transactions were limited. The spot discount narrowed slightly but remained high, with prices struggling to rise, and the price spread with East China continued to widen.

The widening Guangdong-Shanghai price spread primarily stems from divergences in supply-demand dynamics and inventory pressure between the two regions. East China has a higher proportion of industrial profile demand, supported strongly by new energy and photovoltaic demand. Faster downstream resumption of work drove an increase in pickup volumes, easing inventory pressure. South China's consumption is dominated by construction profiles, with a slower resumption pace. Coupled with the short-term concentrated warehousing of supplies, inventory pressure surged sharply, putting downward pressure on spot prices. Going forward, attention should be paid to the digestion speed of South China supplies, the trend of road freight rates, the arrival pace of imported cargo, and the release of downstream peak season demand. As the concentrated warehoused supplies are gradually absorbed, South China's inventory pressure is expected to ease, and the Guangdong-Shanghai price spread may return to a reasonable range.

Overall, the abnormal increase in South China's aluminum ingot inventory is due to the phased and structural concentrated warehousing of supplies, not a reversal in market demand. The nationwide accumulation of aluminum inventory is nearing its end, and the inventory inflection point is still expected to appear by late March or early to mid-April. Close attention should be paid to the marginal changes in regional supply-demand divergence in the future.