en.Wedoany.com Report on Mar 30th, As China's economy shifts towards advanced manufacturing, the steel industry is transitioning from construction-driven long products to flat products, laying the groundwork for producing higher value-added goods. According to Shanghai Metals Market (SMM) data, by the end of 2025, China's hot-rolled coil (HRC) capacity will increase by nearly 40% from 300 million tons in 2020 to 410 million tons, with an estimated annual capacity growth rate of 7%. The expansion pace is expected to slow to 2% over the next five years, and capacity expansion may conclude by 2030.

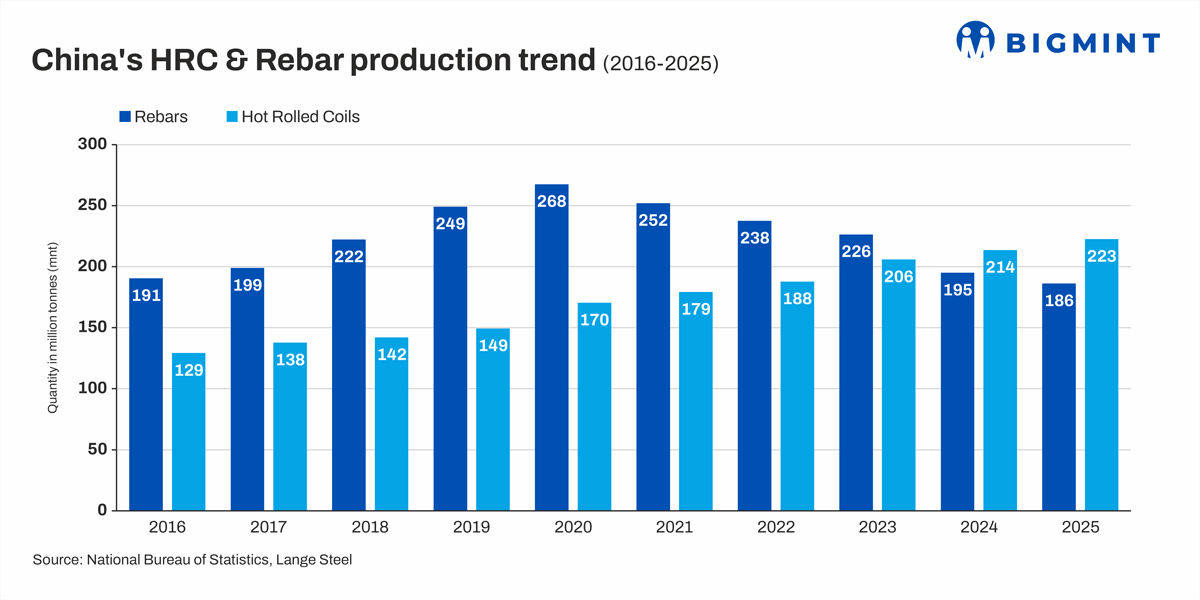

Data from the National Bureau of Statistics and Lange Steel show that since 2024, HRC output has surpassed that of rebar. In 2025, HRC production increased by 24% from 179 million tons in 2021 to 223 million tons, while rebar production fell by 26% to 186 million tons over the same period. This divergence coincides with the real estate sector's adjustment in 2021.

Manufacturing has become the primary driver of steel consumption, accounting for 30% in 2023, up from 20% in 2011. Growth in key manufacturing sectors such as exports of mechanical and electrical products, automobiles, and the shipbuilding industry has supported demand for flat steel like HRC. In 2025, sales of new energy vehicles in China grew 28% year-on-year to 16.5 million units, and the shipbuilding industry accounted for 69% of global new orders.

China's steel industry is accelerating its transformation towards higher grades and value-added products. Hot-rolled coil, as a key base material, is used to manufacture special grades like automotive steel and electrical steel. Industry policies emphasize quality improvement and technological upgrading, aiming for an annual growth in added value of around 4%. This transformation aligns with economic development strategies, promoting the growth of high-end manufacturing.

Looking ahead, the decline in long product output, the rise of flat products, and the advancement of value-added products mark a structural transformation in China's steel industry. It is expected that steel production may see a slight decline in 2026, with demand recovery depending on producers' ability to adapt to manufacturing-dominated consumption and the demand for higher value-added steel.