en.Wedoany.com Reported - Recently, data from CFM Flash Memory Market showed that in the first quarter of 2026, the global NAND Flash market size reached $42.815 billion, a quarter-on-quarter increase of 81.8%. Doubling demand for enterprise SSDs, coupled with AI server infrastructure construction and increased procurement of high-capacity storage, drove a significant rise in the average selling price of NAND flash memory, ushering the global storage industry into a new cycle of high prosperity.

The core driving force behind this rebound in the NAND market has shifted from the traditional consumer electronics replacement cycle to data centers and AI computing infrastructure. In the past, smartphones, PCs, and consumer-grade SSDs were key variables for NAND demand, with price fluctuations largely influenced by end-device inventory and the shipment pace of consumer electronics. Entering 2026, demand for enterprise SSDs has rapidly expanded, with AI training, inference clusters, cloud services, and high-performance storage systems continuously driving up demand for low-latency, high-capacity, and high-reliability flash memory. As server-side procurement prioritization increases, manufacturers are tilting production capacity towards enterprise-grade products, while consumer SSDs, mobile storage, and some low-margin products passively face supply tightness, further amplifying price elasticity. The substantial quarter-on-quarter growth in market size indicates that NAND is no longer just a cyclical product for consumer electronics but is becoming a core storage resource in the expansion of AI infrastructure.

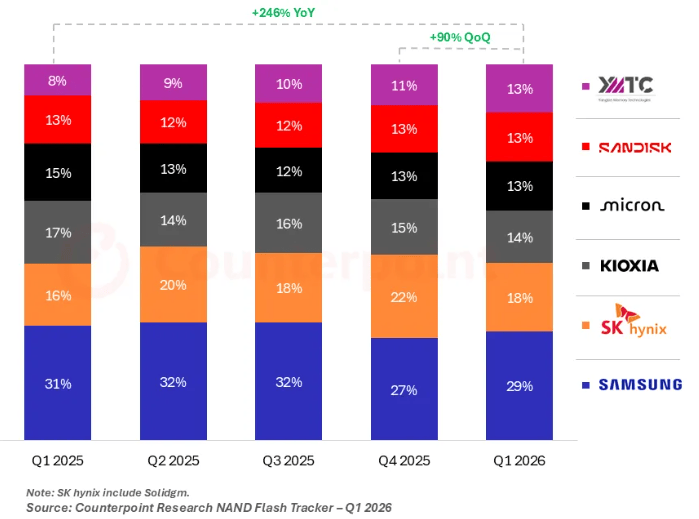

In terms of vendor landscape, Samsung remains the global leader, followed by SK Hynix, Kioxia, SanDisk, and Micron, with the top five vendors collectively holding the vast majority of market share.

The changes at China's YMTC constitute another major industry trend. Public data has shown that YMTC's share of global NAND shipments has risen from over 10% to approximately 13%. Although it is still categorized under "Others" in some revenue-based rankings, its capacity expansion, validation of domestic equipment, enterprise SSD adoption, and the shift of domestic customers are reshaping the global NAND supply landscape. For China's semiconductor industry, YMTC's significance lies not only in its increased market share but also in representing a critical phase for Chinese storage chips, moving from technological catch-up and product validation to volume supply. The NAND industry is characterized by high capital expenditure, long-cycle capacity ramps, and high process barriers. Gaining market share often requires simultaneous completion of process node transitions, yield control, customer qualification, supply chain localization, and continuous capacity expansion.

The current market upswing also provides a more direct window of opportunity for China's storage industry chain. As demand for AI servers and enterprise SSDs drives up global capacity utilization, customers are paying significantly more attention to supply stability, delivery lead times, and price certainty. The acceptance of domestic storage solutions by domestic server manufacturers, cloud computing companies, and terminal brands is expected to continue to increase. If YMTC can make steady progress in high-layer-count 3D NAND, enterprise SSD controller adaptation, packaging and testing, localization of equipment and materials, and customer delivery, it may secure a larger position as the global NAND industry transitions from being "dominated by a few international giants" to a "multi-regional supply system." At the same time, rapid price increases will also bring cost pressure to end-users. The consumer electronics, PC, and general SSD markets may see demand suppression in a high-price environment. The subsequent industry trend will still depend on the sustainability of AI-driven demand and the pace of new capacity releases from manufacturers.

For the integrated circuit industry, the substantial quarter-on-quarter growth in the NAND market size is not just a short-term phenomenon of rising storage prices; it also reflects how AI computing infrastructure is reshaping semiconductor demand structure. HBM, server DRAM, and enterprise SSDs have collectively become key resources for data center expansion. The strategic position of storage chips has evolved from "supporting components" to a critical foundation affecting AI system throughput, cost, and energy efficiency. YMTC's increased market share and expansion expectations will continue to impact China's storage equipment, materials, packaging and testing, modules, and server supply chain. Going forward, it is necessary to monitor its capacity ramp-up, customer structure, proportion of enterprise-grade products, and whether global NAND prices will remain high in the second quarter and the second half of the year.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com