en.Wedoany.com Reported - Uncertainty in U.S. trade policy is reshaping pricing and trade flows in the platinum group metals (PGM) market, with its impact potentially surpassing that of individual mine developments by 2026. A key catalyst is a pending U.S. trade policy decision. The United States relies heavily on imported PGMs, with South Africa as its largest source, accounting for approximately 16% of supply, primarily platinum, rhodium, and palladium used in automotive catalytic converters. On January 14, 2026, Proclamation No. 11001 declined to immediately impose tariffs on processed critical minerals but directed the Department of Commerce and the U.S. Trade Representative to negotiate with trading partners and submit a report within 180 days (i.e., by July 13, 2026). The proclamation explicitly reserves the right to take future actions, including implementing minimum import prices.

The risk of tariffs alone—rather than actual tariffs imposed—has already prompted end-users and traders to ship metals into U.S. warehouses ahead of a ruling, thereby increasing domestic inventories and reducing physical supply in other regions. In April 2026, the U.S. set a final anti-dumping duty of 132.83% on Russian palladium, but it will only take effect if the U.S. International Trade Commission determines that the domestic industry has been injured. As Russia supplies approximately 40% of global palladium, an affirmative ruling could disrupt supply and exacerbate palladium price volatility. Trade barriers could keep metals that have flowed back to the U.S. within the country, reducing supply elsewhere, while negotiation outcomes could release these inventories back into the global market. Consequently, jurisdiction and market access may have a greater impact on the valuation of PGM assets.

Although trade policy may drive short-term price fluctuations, the platinum market remains in deficit. The WPIC (World Platinum Investment Council) Q1 2026 Platinum Quarterly report, released on May 18, shows the council maintains its forecast for a full-year 2026 platinum deficit of 297,000 ounces but recorded a quarterly surplus of 268,000 ounces. The quarterly surplus reflects the timing of investment flows rather than changes in underlying supply and demand. The deficit indicates that consumption plus net investment exceeds primary mine supply and recycling, resulting in an undersupplied market for the full year. Rising platinum prices have not led to significant new supply. Since the mid-2000s, South African primary platinum production has fallen by about a quarter, even through multiple price cycles; over the same period, Eskom (South Africa's state-owned power utility) electricity tariffs for mining operations rose by approximately 60% between 2021 and 2026. South African platinum mines are aging, deep, and power-intensive, so while higher prices have improved profit margins, they have not materially increased output. All-in sustaining costs (AISC, including operating and sustaining capital costs) have risen with energy and labor costs, improving cash flow for existing producers but barely justifying investment in new shafts.

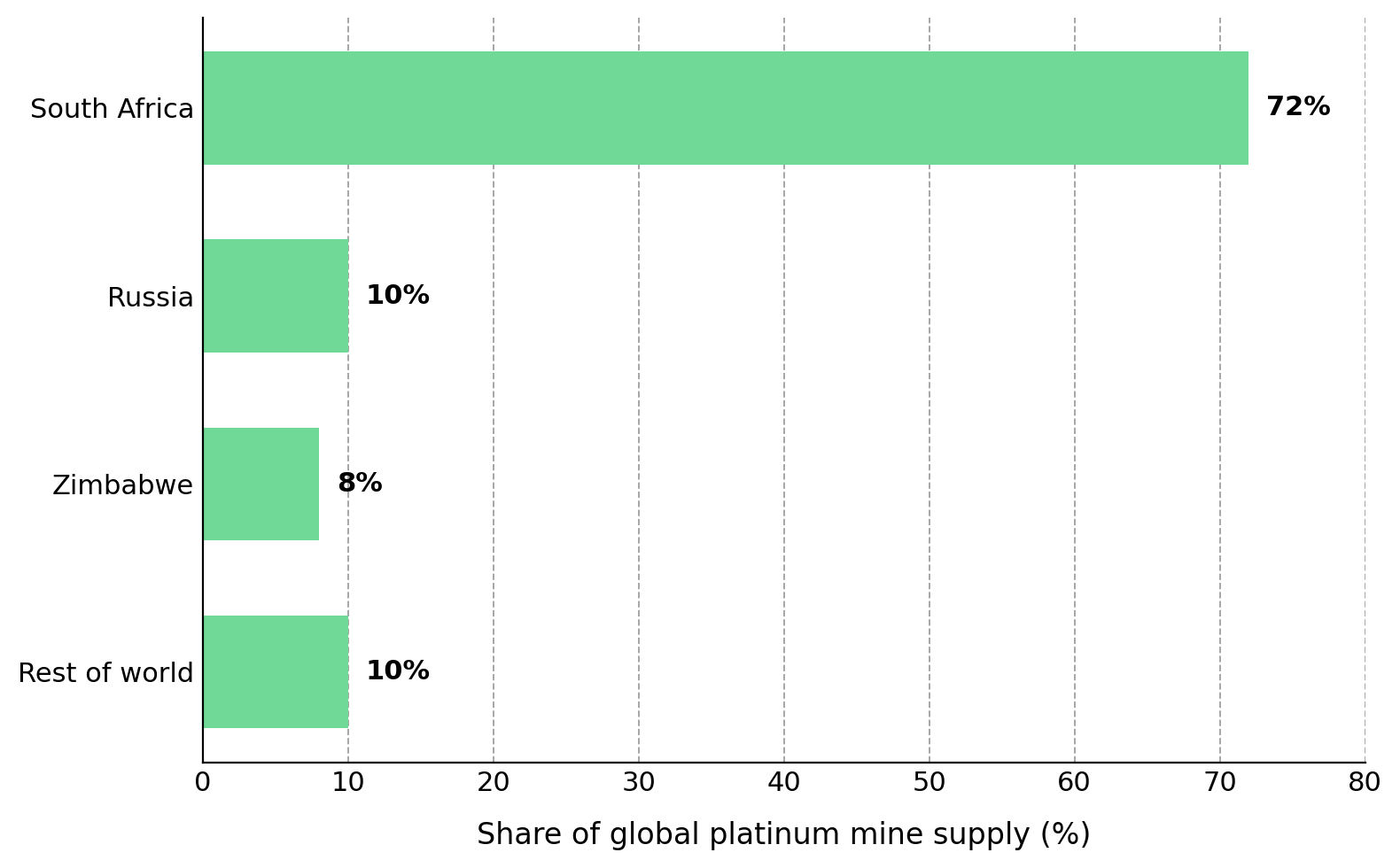

Approximately 90% of global platinum mine supply comes from three countries. Nick Smart, CEO of ValOre Metals, describes the persistent decline in platinum mine supply despite significantly higher prices, highlighting the market's supply inelasticity: "Primary platinum production has been declining over the past five years. It peaked at just over 6 million ounces in 2021, and this year's forecast is around 5.5 million ounces, while the metal price has doubled over the past year." Similar constraints extend to Russia, where producer Nornickel expects platinum output to fall by about 8% to approximately 616,000 ounces in 2026, and palladium output by up to 11%, due to declining ore grades, a trend price signals have failed to reverse.

The platinum deficit is reducing above-ground inventories, which are expected to fall to just under three months of global demand. When inventory levels drop below approximately four months of demand coverage, platinum prices may become more sensitive to supply disruptions than to normal demand fluctuations. With low inventories and slow supply response, disruptions to power, logistics, or trade could have a significant impact on platinum prices. Investors must weigh long-term supply constraints against short-term demand risks. Platinum demand comes from industrial and investment markets, which respond differently to various economic drivers. The adoption of battery electric vehicles is reducing autocatalyst demand, but Chinese jewelry demand, industrial applications in chemicals and glass, and WPIC's forecast of a 35% increase in bar and coin investment demand in 2026 are partially offsetting this decline. Platinum's lower price relative to gold supports investment demand.

Investment flows remain a key driver of platinum prices and are influenced by real yields. Since platinum generates no income, it competes directly with cash and bonds, so changes in the expected path of Federal Reserve policy affect the metal's price. With the benchmark interest rate at 3.5% to 3.75% and the next decision scheduled for June 17-18, reduced expectations for rate cuts caused platinum prices to fall from over $2,200 per ounce to approximately $1,922 within a few trading days, even though the market remains in deficit. The World Bank reports that the average platinum price in Q1 2026 was approximately $2,206 per ounce, indicating prices remain elevated despite recent volatility. A reversal of investment flows could lead to significant declines, even if market fundamentals remain unchanged, while leverage or concentrated single-stock positions could amplify these losses.

Current PGM market conditions are influencing how investors allocate capital across the industry. In a market where approximately 90% of supply comes from three countries and demand exceeds supply, investors may assign higher valuations to assets located in jurisdictions with lower risk and supply chain security. Valuation impacts vary among producers, developers, and explorers, making staged risk assessment crucial. Investors use different valuation metrics for companies at different stages: producers are judged on AISC, EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization), and free cash flow because they generate revenue and operating cash flow; developers are judged on NPV (Net Present Value), IRR (Internal Rate of Return), and permitting timelines, as project economics and execution determine future value; explorers are judged on enterprise value per ounce (EV/oz), grade determined by drilling, and resource confidence, progressing from inferred to indicated, measured, and ultimately reserve categories.

ValOre Metals is an early-stage PGM exploration company operating in Brazil, currently fully focused on the Pedra Branca project in northeastern Brazil, having divested its Saskatchewan uranium interests to Future Fuels. The company is in the exploration stage and has not disclosed AISC, NPV, or reserves. The asset has an inferred resource of 2.2 million ounces announced in 2022, with a key catalyst being a preliminary economic assessment (PEA) planned for completion this year, which will provide the first economic evaluation of the project. Using market capitalization as a proxy for enterprise value, ValOre is valued at approximately $26 million, while PGM development-stage peers with comparable resource sizes are valued at around $100 to $200 million. The valuation gap reflects ValOre's inferred resource classification and the lack of economic studies. Metallurgical performance is a key determinant of Pedra Branca's economics: near-surface oxide deposits may support lower-cost mining, but oxide ores often respond poorly to conventional flotation and may require leaching. Early test work indicates recoveries around 70%, making recovery a critical variable in the upcoming PEA. The project's upside potential must be weighed against risks associated with the exploration stage: exploration companies are typically pre-revenue, illiquid, and reliant on external financing, which can lead to shareholder dilution; inferred resources may not convert to higher-confidence categories; the PEA is a preliminary study with significant uncertainty; and project timelines also depend on permitting, with many exploration projects failing to reach production.

The investment thesis for PGMs involves weighing multiple risk exposures: WPIC forecasts a platinum deficit of approximately 297,000 ounces in 2026 (a fourth consecutive year of shortage), which could support prices and benefit producers with disclosed margins; the highly concentrated PGM supply chain, with approximately 90% of production from three countries, may support higher valuations for assets in alternative jurisdictions; the risk of potential trade policy changes, including the U.S. Section 232 process and Russian palladium tariffs, could disrupt physical markets and increase the strategic value of non-Russian, non-South African supply; and the phenomenon of platinum prices doubling to improve producer cash flow without generating significant new supply supports the case for a sustained deficit and the need for new resource development. Investors should apply a staged valuation framework, focusing on cost curves and scenario analysis for developers, and enterprise value per ounce and resource confidence for explorers.

This investment thesis is based on several assumptions that could prove incorrect. The thesis would weaken if trade agreements release U.S. warehouse inventories back into the global market, if South African or Russian supply recovers faster than expected, if rising interest rates reduce investment demand, or if BEV adoption reduces autocatalyst demand faster than jewelry, industrial, and investment demand can offset. Any of these outcomes could reduce the supply-demand tightness that currently supports platinum prices and valuations.

The central question for the PGM market in 2026 is whether supply can respond to demand growth and policy-driven disruptions. In a concentrated market with recurring deficits, jurisdiction, supply security, and future development potential may have a greater impact on valuations than resource size alone. Favorable market conditions do not eliminate company-specific or stage-specific risks, making rigorous due diligence essential.

Summary: The platinum market remains in a state of structural undersupply, with the World Platinum Investment Council forecasting a fourth consecutive annual deficit in 2026, while above-ground inventories continue to decline. Concurrently, persistent uncertainty in U.S. trade policy and the concentration of nearly 90% of global PGM production in South Africa, Russia, and Zimbabwe are elevating the strategic importance of supply security. Investors are increasingly focusing on jurisdictional risk, supply chain resilience, and development potential when evaluating PGM companies, while applying different valuation frameworks for producers, developers, and explorers.

Frequently Asked Questions (AI-generated):

Why is platinum expected to remain in deficit in 2026? The World Platinum Investment Council forecasts a platinum deficit of approximately 297,000 ounces in 2026, marking a fourth consecutive year where demand exceeds mine supply and recycling. Despite higher prices improving producer margins, supply growth remains limited due to aging mines, declining ore grades, rising operating costs, and infrastructure constraints in major producing regions. Consequently, inventories continue to decline even as demand from industrial, jewelry, and investment markets remains relatively robust.

How does U.S. trade policy affect the PGM market? The U.S. Section 232 critical minerals review introduces uncertainty regarding potential tariffs, quotas, or minimum import prices for strategic minerals. Even without immediate tariff imposition, market participants have preemptively moved inventories to U.S. warehouses in anticipation of possible policy changes. Future trade restrictions could alter global PGM trade flows, increase regional price volatility, and confer greater value on supply sources with reliable market access.

Why is supply concentration important for PGM investors? Approximately 90% of global primary PGM production comes from South Africa, Russia, and Zimbabwe. This concentration increases the market's vulnerability to geopolitical tensions, operational disruptions, power shortages, logistics bottlenecks, and regulatory changes. In a market already facing recurring deficits, investors may assign premium valuations to projects located in lower-risk jurisdictions that can diversify global supply.

What valuation metrics should investors use for different types of PGM companies? Valuation methods vary by company development stage. Producers are typically assessed using metrics such as all-in sustaining costs (AISC), EBITDA, and free cash flow, as they generate operating revenue. Developers are usually evaluated using net present value (NPV), internal rate of return (IRR), and permitting progress. Exploration companies are typically pre-revenue and are more commonly valued using enterprise value per ounce, resource size, resource confidence, and the potential impact of future economic studies.

What are the biggest risks to the bullish platinum investment thesis? Several factors could undermine the current platinum investment case. A favorable trade agreement could release accumulated inventories back into the global market, easing supply tightness. Mine production in major producing countries could recover faster than expected, while rising interest rates could reduce investment demand for precious metals. Additionally, the adoption of battery electric vehicles could accelerate faster than anticipated, hastening the decline in autocatalyst demand, potentially offsetting growth in jewelry, industrial, and investment sectors.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com