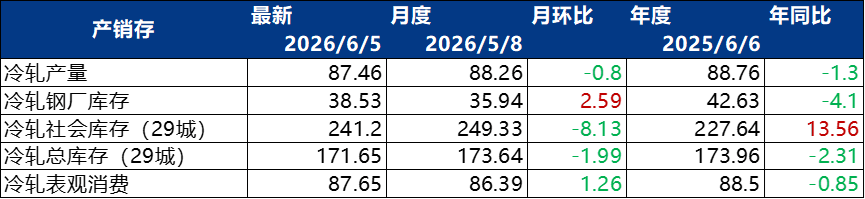

en.Wedoany.com Reported - Last week, the steel market showed divergent trends, with ferrous and non-ferrous metals sectors driven by different cost and demand factors. As of June 5, the five-day average daily transaction volume of hot-rolled coils nationwide reached 42,666 tons, up 5.66% from the previous week but down 13.47% month-on-month. The five-day average daily transaction volume of cold-rolled coils was 20,661 tons, up 13.7% from the previous week. Meanwhile, the non-ferrous metals market continued its pattern of strength overseas and weakness domestically, with the tug-of-war between cost support and demand drag becoming the dominant logic.

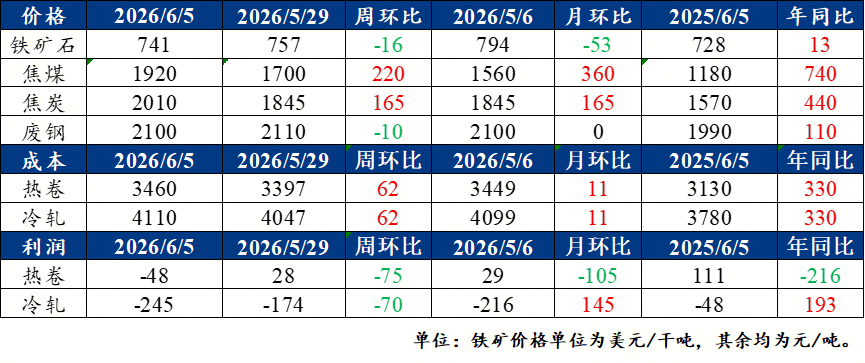

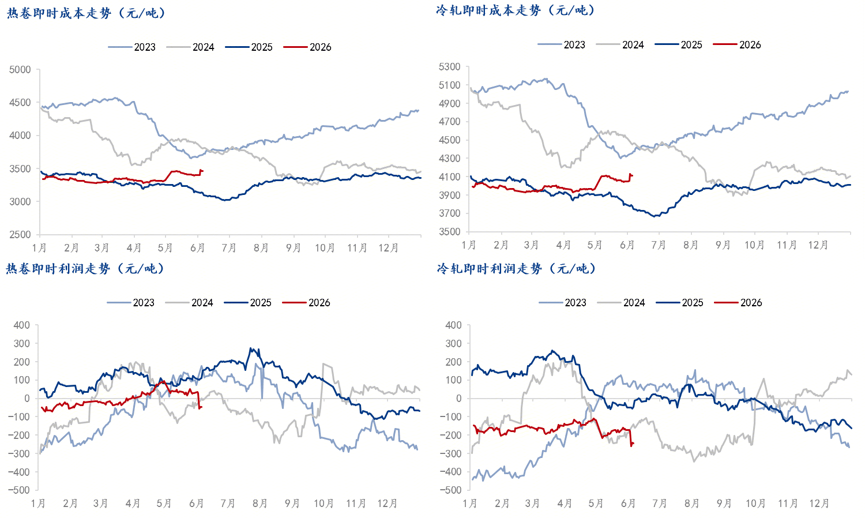

In the steel sector, the national average price of hot-rolled coils was 3,412 yuan/ton, down 13 yuan/ton from the previous week. Prices in Shanghai fell 20 yuan/ton week-on-week, Guangzhou prices remained flat, and Tianjin prices rose 30 yuan/ton week-on-week. Speculative demand emerged in the market, leading to a recovery in transaction volumes. The average price of 1.0mm cold-rolled coils was 3,865 yuan/ton, down 8 yuan/ton week-on-week. In Shanghai, the quoted price for 1.0mm Benxi Steel cold-rolled coils was 3,750 yuan/ton, down 20 yuan/ton week-on-week. In Lecong, the quoted price for 1.0mm Liuzhou Steel cold-rolled coils was 3,790 yuan/ton, down 10 yuan/ton week-on-week. In Tianjin, the quoted price for 1.0mm Angang Tiantie cold-rolled coils was 3,690 yuan/ton, down 10 yuan/ton week-on-week. In terms of costs and profits, the sharp rise in coke and coking coal prices pushed up the costs of hot-rolled and cold-rolled coils. However, due to the larger magnitude of cost increases, spot profits for finished steel products contracted.

On the steel mill supply side, according to a full-sample survey by Mysteel on hot-rolled coils, the estimated total impact volume for hot-rolled coils last week was 13,600 tons, the actual total impact volume this week was 2,000 tons, and the estimated total impact volume for next week is 40,000 tons. One steel mill in North China resumed production this week. The data statistics period is from May 28 to June 3, 2026, and the next week's statistics period is from June 4 to June 10.

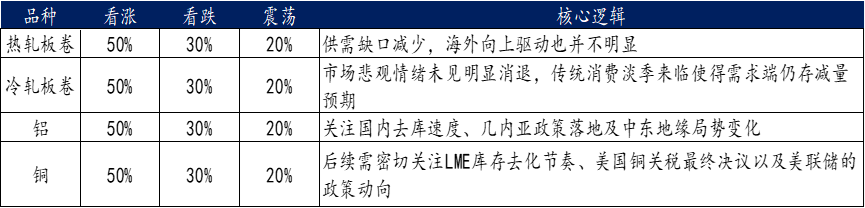

In the non-ferrous metals sector, the aluminum market showed a pattern of strength overseas and weakness domestically. Low overseas inventories combined with supply disruptions pushed LME aluminum to a new high for the period, while high domestic inventories and weak seasonal demand dragged SHFE aluminum down after an initial rally. The copper market continued to seesaw between macro expectations volatility and supply-side support, with the market awaiting the implementation of tariff policies and clarity on the Federal Reserve's policy direction. In the short term, copper prices are expected to maintain high-level fluctuations, with the price range likely between 102,500 yuan/ton and 106,500 yuan/ton. Going forward, close attention should be paid to the pace of LME inventory destocking, the final resolution on US copper tariffs, and Fed policy moves. Zinc prices rose and then fell amid intense competition between cost support and demand drag. The core contradiction in the nickel market remains clear: cost-side support from tighter Indonesian ore supply and rising smelting costs, but high visible inventories and subdued real demand form a ceiling.

In terms of policy and industry hotspots, the steel industry saw the implementation of supporting rules for the new version of the "Implementation Measures for Steel Industry Capacity Replacement." The replacement ratio for ironmaking and steelmaking capacity has been uniformly raised to 1:1.5, with the minimum ratio for mergers and acquisitions replacement set at 1:1.25. Cross-enterprise capacity replacement will be abolished after two years. A "lookback" review of ultra-low emissions and a special energy consumption inspection were launched on June 1. Long-process steel enterprises must complete ultra-low emission verification by the end of June; those failing to meet standards will face production restrictions and rectification at 70% capacity. In the non-ferrous metals industry, local implementation rules for the "Stable Growth Work Plan for the Non-Ferrous Metals Industry (2025-2026)" have been intensively rolled out, targeting an average annual industrial added value growth rate of 5%, with key support for three major directions: green exploration, high-end new materials, and recycled metal recycling. The Shanghai Futures Exchange revised non-ferrous metals delivery rules, strengthening quality control for lead futures deliverable products. Preparations are underway for the supporting rules of the new "Regulations for the Implementation of the Mineral Resources Law," which will include 25 types of critical minerals such as copper, lithium, cobalt, nickel, rare earths, gallium, and germanium in the strategic mineral catalog. In the automotive sector, the policy halving the purchase tax on new energy vehicles has been extended until 2027. National subsidy details for trade-in programs were implemented on June 4: scrapping and replacing with a new energy vehicle provides a 12% subsidy (up to 20,000 yuan), while replacing with a fuel vehicle provides a 10% subsidy (up to 15,000 yuan). For replacement purchases (without scrapping), buying a new energy vehicle provides an 8% subsidy (up to 15,000 yuan), and buying a fuel vehicle provides a 6% subsidy (up to 10,000 yuan). The national standard "Specification for Defect Monitoring and Analysis of Traction Batteries in Battery Swap Scenarios" took effect on June 1.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com