en.Wedoany.com Reported - Algeria's 2026 oil and gas tender round is at a critical juncture where geopolitics and market demand intersect. The Middle East crisis has pushed up oil and gas prices, Europe is accelerating the diversification of non-Russian gas supplies, and Middle Eastern investors are reassessing the safe destinations for upstream capital. These factors create an opportunity for Algiers to consolidate its position as Europe's second-largest gas supplier, but also expose challenges that need to be overcome.

In early June, the Algerian National Agency for the Development of Hydrocarbon Resources (ALNAFT) launched a tender for seven onshore conventional oil and gas blocks, with bidding and approval processes to be completed by November. These blocks are estimated to contain approximately 2.1 billion barrels of oil and 66.5 billion cubic meters of gas, located within existing discovery and exploration areas. Four of the blocks are situated in the Illizi-Ghadames Basin near the borders with Libya and Tunisia, while the remaining blocks cover areas with greater oil potential in the Oued Mya and Sahara Basins.

Geographic location is a key factor influencing this tender round. The 2024 round was more focused on the gas-rich southwestern region, which, despite attractive resources, suffered from underdeveloped infrastructure and longer exploration and production cycles. The 2026 round shifts to the southeast, where the Berkine and Illizi-Ghadames Basins are more mature, with well-established facilities and convenient market access, making this tender more commercially relevant in the current high-price environment.

While the previous tender round was not a failure, it was not a resounding success either. Five out of six licenses were awarded, but competition was mild, reflecting the long-standing difficulty of Algeria's upstream terms in attracting sufficient foreign capital. The 2014 round had already exposed obstacles posed by high taxes, strict state control, and limited commercial flexibility. The 2019 Hydrocarbons Law attempted to improve the situation by expanding contract options and removing the previous requirement for Sonatrach to hold at least a 51% stake in upstream projects.

The 2024 awards indicate that adjustments have begun to yield results. QatarEnergy and TotalEnergies jointly entered the Ahara license, with TotalEnergies as operator, each holding a 24.5% stake. Eni and PTTEP secured the gas-oriented Reggane 2 project. Chinese companies are also deepening their involvement, with Sinopec acquiring the Hassi Berkane North block and conducting gas exploration at Guern El Guessa, while Zhongman Petroleum entered the Zerafa II gas block. Subsequently, Eni signed a $1.35 billion production sharing agreement at the Zemoul El Kbar border, expected to produce 415 million barrels of oil equivalent, including 9.3 billion cubic meters of gas. Saudi Arabia's Midad Energy also signed a $5.4 billion contract for the Illizi South block.

The diversity of the investor portfolio is significant. Eni has been operating in Algeria since 1981, producing approximately 140,000 barrels of oil equivalent per day. TotalEnergies is both an upstream investor and a major offtaker of Algerian LNG. QatarEnergy brings LNG expertise and financial support. The entry of PTTEP, Sinopec, and Saudi companies indicates that Algeria's upstream opening is no longer limited to the European market. Negotiations with Chevron and ExxonMobil regarding shale and unconventional gas are ongoing, and if commercial terms remain attractive, potential interest could be further stimulated.

Algeria's export position is strong, but its production base is not solid. It is Africa's largest gas producer, with gas accounting for about 49% of its oil and gas output. Total recoverable resources are estimated at 2.5 to 3.4 trillion cubic meters of gas and approximately 10.5 billion barrels of oil. However, existing fields are mature, domestic demand is rising, and the export surplus is being squeezed. Production increased from about 278 million cubic meters per day in 2021 to 287 million cubic meters per day in 2023, but the latter appears to be a peak rather than the start of a sustained growth cycle.

The backbone of Algeria's upstream sector is the Hassi R'Mel gas field, which, after 65 years of operation, remains the mainstay of the production base. The field peaked in the mid-1990s and is now deeply mature, with its initial resource base of 3 trillion cubic meters depleted to about 20% of its original volume. Satellite fields and grid connection measures have slowed the decline, but discoverable reserves are decreasing, and Sonatrach's room for maneuver is shrinking. Much of the current pressure stems from a 14-year moratorium on production sharing and service contracts for gas fields imposed between 2005 and 2019, which hindered development when upstream momentum waned following the incremental supply discoveries of the 1980s and 1990s.

Pipeline gas remains the backbone of Algeria's export system. About two-thirds of exports are transported via pipelines, primarily through the TransMed line (via Tunisia and Sicily into Italy) and the Medgaz subsea pipeline (directly to Almería, Spain). TransMed has an annual capacity of approximately 32 to 35 billion cubic meters, transporting about 21 billion cubic meters in recent years. Medgaz can deliver around 10 to 10.5 billion cubic meters annually. A third Morocco-Spain line has been closed since 2021, after Algiers refused to renew the transit agreement due to political tensions with Rabat.

Italy is now Algeria's main gas customer, receiving about 20 to 23 billion cubic meters annually, with approximately 30% of its gas demand relying on Algerian supply. Spain is politically more complex but remains structurally important, with Algeria meeting about 25% of its gas imports. Negotiations launched in March 2026 to expand Medgaz by up to 1 billion cubic meters per year indicate that demand for Algerian pipeline gas persists, with the constraint being delivery capacity.

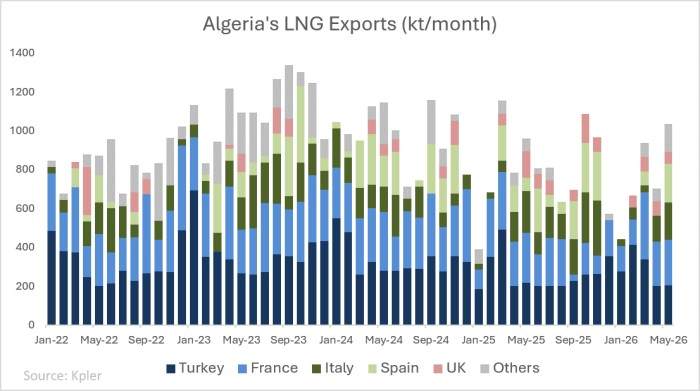

LNG exports follow a similar pattern but are more volatile. Algeria has two LNG export hubs: Arzew/Bethioua in the west, with a liquefaction capacity of about 20.8 million tons per year, and Skikda in the east, with an operational capacity of about 4.5 million tons per year. Following Europe's decoupling from Russian gas, LNG exports surged from an average of about 900,000 tons per month to a record 1.3 million tons in September 2023, a 60% year-on-year increase. France, Italy, and Spain are the main European buyers, with Turkey receiving nearly a quarter of the cargoes. By 2025, Algeria's LNG exports to Europe had declined to about 9.5 million tons per year, accounting for roughly 6% of European LNG imports, a decrease of about 2 million tons year-on-year. Combined with pipeline exports, by 2025 Algeria accounted for about 18% of EU gas imports, second only to Norway and ahead of Russia. This gives Algiers strategic leverage, especially with Italy and Spain, but also increases risk: Europe needs Algeria to remain reliable, and Algeria needs new upstream investment to maintain production.

A recent issue is Algeria's growing domestic demand. In 2025, Algeria consumed about 57 billion cubic meters of gas per year, more than half of its national production. Every additional cubic meter must be contested among power demand, industrial consumption, pipeline contracts, and LNG cargoes. Hydrocarbons account for about 10% to 12% of GDP and over 90% of export revenues, and the shrinking export buffer is not just an energy issue but also a fiscal and external balance concern.

This makes the 2026 tender round more important than the regional map suggests. Oil still has value, but Algeria's OPEC+ membership sets a ceiling on future crude investment. Gas is the strategic priority, as it can strengthen Algeria's role in European supply security, maintain market share in Italy and Spain, and provide Sonatrach with more options through LNG. However, this requires new field development and infrastructure investment in less developed gas regions.

Algeria faces a rare opportunity: Europe wants nearby gas, investors want to avoid security risks in the Gulf, and the country has adjusted its upstream terms more flexibly than a decade ago. But the window is not permanent. Mature fields, growing domestic demand, and infrastructure gaps will steadily erode export capacity unless new projects advance quickly. If the 2026 tender round attracts substantial capital, Algeria can turn the current geopolitical opportunity into a long-term gas advantage; if it disappoints, the country may become a supplier that Europe urgently needs but has too little remaining gas to fully benefit from.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com