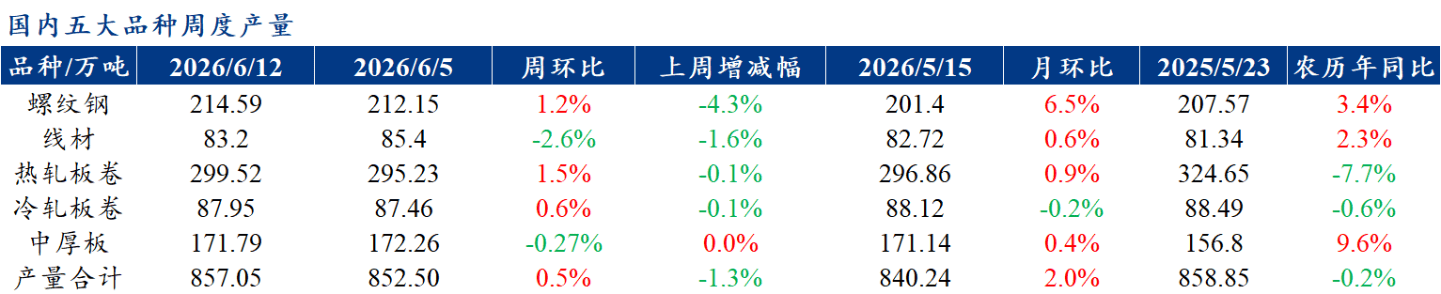

en.Wedoany.com Reported - This week, the output of the five major steel products stood at 8.5705 million tons, a week-on-week increase of 45,500 tons, or 0.5%. Output of all major products increased week-on-week except for wire rod and medium plate, driven primarily by still-viable mill profits, leading some mills to boost production. Total inventories reached 15.6022 million tons, a week-on-week increase of 120,500 tons, or 0.78%. Total inventories of the five major products all increased week-on-week, with the mill inventory increase mainly contributed by rebar and the social inventory increase mainly contributed by hot-rolled coil. In terms of consumption, weekly consumption was 8.45 million tons, down 0.4% week-on-week, with construction materials consumption falling 1.8% and flat products consumption rising 0.3%, showing a trend of declining construction materials and rising flat products.

On the supply side, the impact of environmental inspections in May is gradually fading. With mills still generating some profits, output is expected to continue recovering. On the demand side, from the perspective of fund allocation, the proportion of available funds for projects has declined rapidly. As of the end of this week, 43.7 billion yuan of special new special-purpose bonds were issued in June, while no land reserve special-purpose bonds were issued. Excluding these two parts, the proportion of newly issued special-purpose bonds in June that can be used for project construction was 60%, a relatively low level in the past two years (30th percentile). With slowing funds, rising temperatures, and the ongoing high school entrance examination, downstream demand continues to slow. On the raw materials side, the sixth round of coke price hikes has been implemented, with further increases expected, providing relatively strong overall raw material support. Overall, pressure on finished steel is gradually building, with declining demand but persistent cost support. Short-term steel prices are expected to fluctuate.

In terms of weather, heavy rainfall is expected in southern China from June 6 to 9. Parts of eastern Sichuan, Chongqing, central and eastern Guizhou, southern Guizhou, northern and southern Yunnan, western and southern Hunan, Guangxi, Guangdong, Fujian, central and southern Jiangxi, southern Zhejiang, and Taiwan Island will experience heavy to torrential rain, with localized extreme downpours. Cumulative rainfall is forecast to be 40 to 80 mm, with 100 to 160 mm in parts of western and southeastern Chongqing, northeastern and southern Guizhou, western Hunan, northern Guangxi, central coastal and northwestern Guangdong, central Fujian, and Taiwan Island, and locally exceeding 220 mm.

On the macro front, April analysis indicated that the upward transmission of upstream costs to end-consumer prices was insufficient. In May, CPI was flat year-on-year and slightly down month-on-month, with core CPI remaining inelastic. Non-food prices lost momentum after the May Day holiday, and service prices fell seasonally, suggesting that the resilience of core demand after the holiday effect fades requires more time to verify. May data failed to sustain the slight outperformance seen in April, and market expectations for confirming an inflation rebound may be further delayed.

In terms of cement and concrete, from June 3 to June 9, national cement off-take was 2.5895 million tons, down 5.37% week-on-week and 9.57% year-on-year. Direct supply of cement for infrastructure was 1.63 million tons, down 2.98% week-on-week and 5.78% year-on-year. According to a survey by 100-year Architecture, the capacity utilization rate of 506 domestic concrete mixing plants was 6.23%, down 0.49 percentage points week-on-week and 0.58 percentage points year-on-year. Dispatch volume was 1.2485 million cubic meters, down 7.24% week-on-week and 8.44% year-on-year. Affected by recent major examinations, the pace of construction at regional sites has slowed, concrete market demand has declined, and overall dispatch volume has dropped significantly.

According to Mysteel statistics, rebar output turned from a decline to an increase, with a cumulative increase of 24,400 tons. The increase mainly came from the East China and Southwest regions, with Jiangxi and Sichuan leading the gains, due to production line conversions and increased production loads at some mills. Production line saturation decreased in provinces such as Guangxi and Shanxi, leading to a slight reduction in output. Wire rod output decreased slightly, with a total reduction of 22,000 tons, mainly from blast furnaces, including a decrease of 14,500 tons in East China and 11,300 tons in Shanxi. Hot-rolled coil output increased slightly, up 42,900 tons week-on-week, with one East China mill resuming production, while output at other mills remained largely stable.

According to Mysteel statistics, rebar mill inventories expanded their increase, accumulating a rise of 77,200 tons. Inventory increases were led by East China and Southwest regions, while South China saw a slight decline; provinces such as Jiangsu and Yunnan led the gains, while Guangdong and Sichuan saw slight decreases. Wire rod mill inventories increased slightly, with a total increase of 7,900 tons. The Northwest region saw a larger increase, up 10,800 tons week-on-week, and Shanxi saw a significant increase of 6,400 tons. Hot-rolled coil mill inventories continued to fluctuate narrowly. Recently, market prices have been weak, downstream orders have remained largely flat, speculative demand in the circulation market has weakened, and overall demand has been weak.

According to Mysteel statistics, for construction materials, taking rebar as an example, inventories in the East China region decreased by 45,400 tons week-on-week, while inventories in the Southern and Northern regions increased by 16,800 tons and 24,100 tons week-on-week, respectively. Among the seven major regions, all except East China and South China showed inventory accumulation. For hot-rolled coil, inventories in the East China region increased by 1,300 tons week-on-week, while inventories in the Southern and Northern regions increased by 32,300 tons and 26,700 tons week-on-week, respectively. Among the seven major regions, all except Central China showed inventory accumulation.

According to Mysteel statistics, total inventories of the five major products this week were 15.6022 million tons, up 120,500 tons week-on-week, or 0.78%. Among them, construction materials inventories increased by 58,000 tons week-on-week, or 0.75%, and flat products inventories increased by 62,500 tons week-on-week, or 0.81%. Total inventories in the previous period were 15.4817 million tons, up 0.24% week-on-week, with construction materials inventories up 2,800 tons, or 0.04%, and flat products inventories up 34,500 tons, or 0.44%.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com