en.Wedoany.com Reported - South Africa's consumer mobile market has hit a structural growth ceiling, with existing operators facing transformation pressure, while the machine connectivity sector is emerging as a new growth engine.

According to data from the Global System for Mobile Communications Association (GSMA Intelligence), South Africa has 124 million active SIM cards, with a population of approximately 65 million. Based on Statistics South Africa's mid-2025 estimates, the population aged 15 and above is about 46.6 million, constituting the actual addressable market for consumer mobile products, equivalent to 2.66 SIM cards per adult. The unemployment rate in the first quarter of 2026 was 32.7%, with youth unemployment (ages 15-24) as high as 60.9%, indicating a shrinking pool of new economic activity customers. Future consumer mobile growth will primarily come from the redistribution of existing users rather than market expansion.

Market forecasts from Business Market Information Technology (BMIT) show that the number of mobile virtual network operator users will grow from the current approximately 4.8 million to between 11 million and 12 million by 2029, but this growth essentially involves users moving between different operators or adding secondary SIM cards. Banking mobile virtual network operators, such as Capitec Connect, FNB Connect, Standard Bank Connect, and Nedbank Connect, are unaffected as they serve a restricted financial customer base and their business models do not rely on connectivity revenue growth. Retailer mobile virtual network operators, such as Pick n Pay, Mr Price, Shoprite, and Spar, can also withstand market saturation pressures by leveraging their existing loyalty ecosystems and distribution networks.

New entrants lacking a large existing institutional backing, such as educational or fintech-integrated mobile virtual network operators that have emerged since 2024, face severe challenges. A report from Africa Analysis shows that as of mid-2025, South Africa had 38 launched mobile virtual network operator brands, but only 21 were active, with 17 brands having failed. The case of South Africa's first mobile virtual network operator, Virgin Mobile SA, which entered voluntary business rescue in 2020 and closed in November 2021, illustrates the pattern of market clearing.

Regulatory policies further intensify industry pressures. The Independent Communications Authority of South Africa has implemented cost-based pricing for inter-operator call termination fees, and the Electronic Communications Amendment Bill plans to extend this logic to mobile virtual network operator wholesale rates. European experience shows that aggressive wholesale pricing can lead to long-term underinvestment and market consolidation. For consumer mobile virtual network operators without an anchor institution, the question has shifted from whether to transition to specialized connectivity to whether they have the time and capital to complete the transition before user churn occurs.

The same logic applies to mobile virtual network enablers, the platform layer between network operators and mobile virtual network operators. The mobile virtual network enablers that will survive this transformation are those that have already shifted to connecting machines and devices, providing platform infrastructure for specialized operators. South Africa's mobile market currently has 23 active operators. Vodacom launched its own network hosting platform in September 2024, followed by Telkom in March 2025. The independent platform Huge NXTGN saw its user base grow from fewer than 10,000 managed in December 2025 to over 110,000 by May 2026. While regulation is opening market doors, the consumer market behind those doors is not growing.

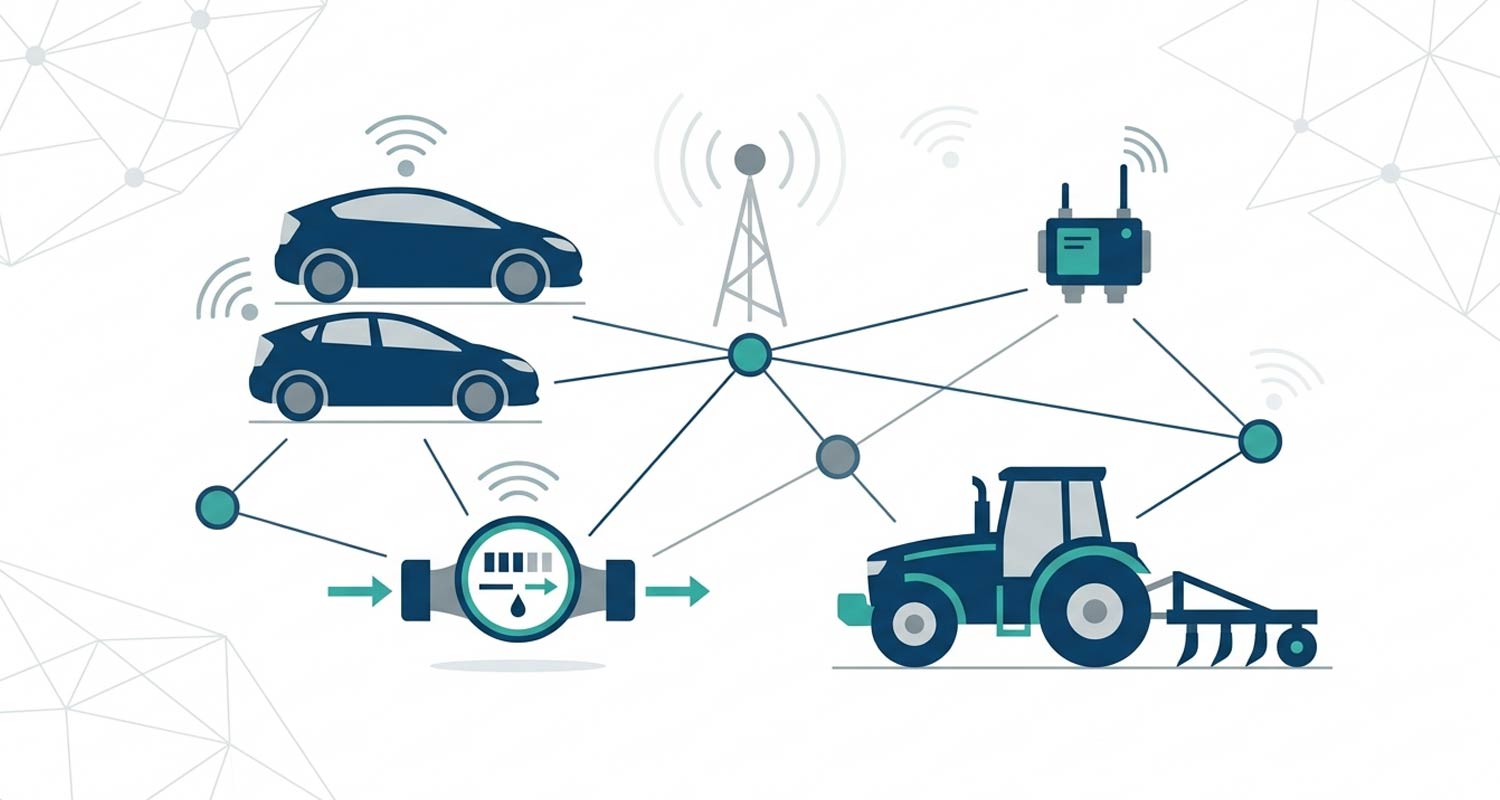

Real growth opportunities lie in the machine connectivity sector, involving vehicles, meters, industrial equipment, logistics assets, and agricultural infrastructure. As of September 2025, South Africa had 13.6 million registered vehicles, while the connectivity rate for assets such as smart meters and mining sensors remains very low. Vodacom's acquisition of IoT.nxt for 1 billion rand in 2019 confirms the reality of this market. However, two limiting factors exist: first, the market space for specialized machine connectivity is not yet as precisely calculable as the consumer market; second, not all machine connectivity relies on cellular networks, as low-cost wireless technologies have advantages in certain scenarios.

Operators capable of seizing machine connectivity opportunities should be enterprises built for this purpose, requiring different capabilities such as enterprise relationships, platform development, and operational technology integration. The consumer growth ceiling in South Africa's mobile market is now calculable, and the market is approaching it. Growth has not dried up, but the structures built by the current generation of operators to capture that growth need to be reshaped.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com