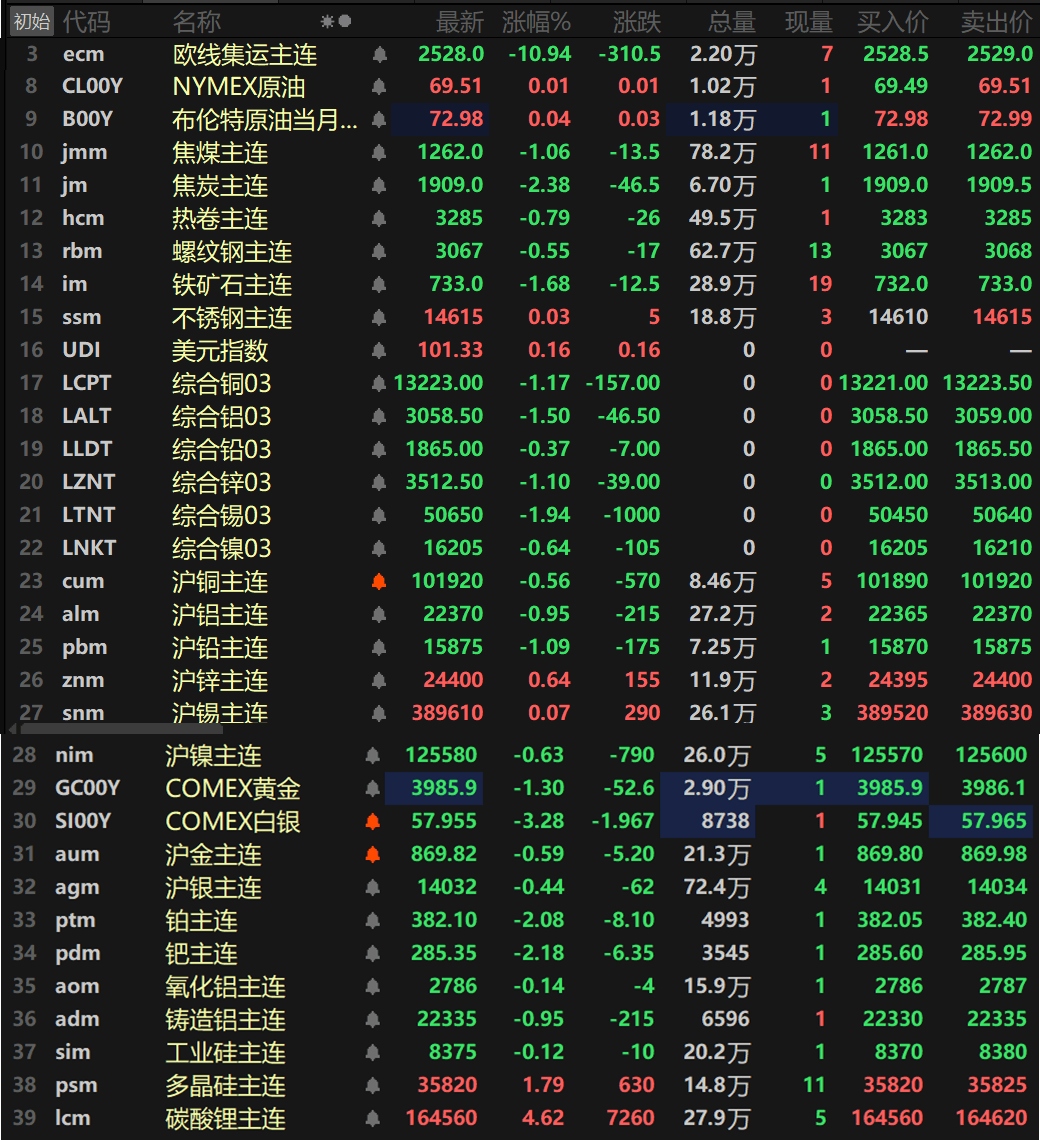

en.Wedoany.com Reported - SMM data shows that in the first half of 2026, refined indium led the spot metal market with an 86.73% increase. Germanium ingots, 45% grade molybdenum concentrate, and battery-grade lithium carbonate recorded gains of 72.22%, 37.38%, and 32.07% respectively, firmly ranking among the top gainers. Praseodymium neodymium oxide, first-grade metallurgical coke, and SMM#1 tin also experienced notable upward trends. In contrast, among the weaker varieties, 1# antimony ingot fell 27.19% in the first half of the year; SMM#1 silver showed a pattern of rising then falling, closing the first half with an overall decline of 24.44%, indicating significant long-short divergence.

Looking back at the first half of the year, geopolitical conflicts continued to disrupt market risk appetite, the inflection point in Federal Reserve monetary policy expectations emerged, and robust demand from the AI industry chain constituted core variables influencing the metals market. Expectations of tight supply supported an upward bias for most metals in the first half of the year. However, recent macro headwinds have concentrated: the US dollar index posted two consecutive monthly gains, putting pressure on dollar-denominated commodities; coupled with rising concerns over the true intensity of AI demand and returns on capital investment, this further dragged down various metal prices.

Looking ahead to the second half of the year, whether the Federal Reserve's interest rate path will continue easing or shift to tightening, policy uncertainties from the US midterm elections, and the evolving pace of global geopolitical situations will continue to reshape the pricing logic of the metals market, influencing the future trading ranges of various metal varieties. From a medium-to-long-term perspective, beyond the two traditional drivers of global macro policy and geopolitical games, marginal changes in demand from the new energy and high-end electronics sectors, as well as the stability and resilience of global resource supply chains, could deeply impact the price centers of various metal varieties.

SMM analysis shows that in June 2026, China's total production of sintered NdFeB blanks increased both month-on-month and year-on-year. However, analyzing the order structure, the increase this month was mainly driven by non-essential stocking demand triggered by raw material price fluctuations, rather than actual expansion in end-user consumption. Based on this, SMM expects China's NdFeB blank production to decline month-on-month in July.

The slight increase in NdFeB production in June showed a high positive correlation with the sharp volatility in upstream rare earth metal prices. This month, praseodymium neodymium metal prices exhibited a significant "bottom-fishing rebound" pattern. At the beginning of the month, influenced by downstream wait-and-see sentiment, praseodymium neodymium prices continued a gradual decline, with magnetic material companies receiving few orders. By mid-June, market sentiment reversed, and praseodymium neodymium prices surged by 27,500 yuan/ton on June 17, marking the largest single-day increase of the year. This price anomaly directly altered downstream procurement strategies.

Since the NdFeB industry often uses a "raw material cost + processing fee" pricing model, the rapid rise in raw material prices meant a direct increase in production costs. Driven by expectations of further price increases, downstream customers concentrated their procurement orders for precautionary stockpiling. However, as praseodymium neodymium prices hit a short-term peak on June 24, downstream end-users developed "fear of heights" due to difficulties in passing on costs, and the pace of new order signing subsequently slowed. Thus, the production growth in June was essentially inventory transfer driven by price expectations, rather than a comprehensive recovery in real demand.

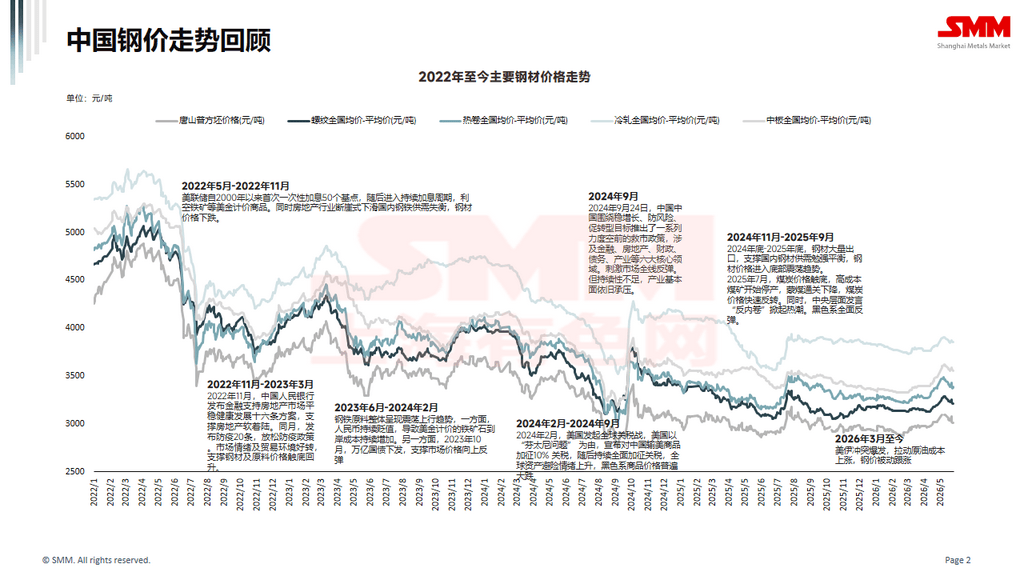

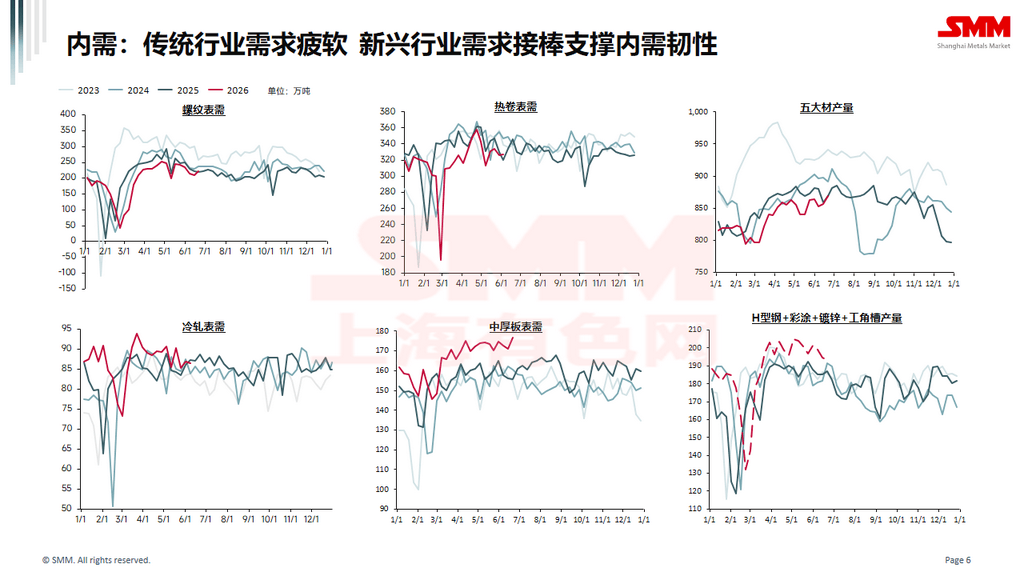

Regarding ferrous metals, SMM expects the price center for hot-rolled coil (HRC) in 2026 to shift slightly higher but with limited upside. Over the next year, nearly 40 million tons of HRC capacity projects are planned or under construction in China from 2026 to 2027, with production expected to increase further in 2026. On the demand side, China's macro policies are expected to remain accommodative, with the manufacturing sector likely to see further stimulus policies for consumption, providing strong demand resilience. However, affected by anti-dumping measures and export structure adjustments, a decline in HRC exports will pressure China's high supply situation. Overall, HRC prices are expected to continue bottoming out in 2026, but considering that overseas geopolitical conflicts are fueling inflation expectations and transmitting to commodity prices, coupled with coal and coke prices entering a new repair upward cycle, the average HRC price may rebound slightly compared to 2025 against a backdrop of rising costs. Looking five years ahead, given that the current peak investment period has passed, and with accelerated industry mergers and restructuring and continuous optimization of capacity structure, the growth rate of HRC supply is expected to gradually slow and stabilize from 2027 onwards. SMM expects that around 2028, a policy combination of supply-side production cuts and tightened steel exports may reappear, and the improvement in overcapacity contradictions could lead to an upward opportunity for HRC prices. However, unlike the intensity of the 2015 supply-side reform combined with real estate easing and shantytown renovation destocking policies, the overall downward trend in China's steel consumption is difficult to reverse after the phased capacity reduction ends, limiting the upside potential of this round of HRC price increases driven by supply contradiction relief. Additionally, the loosening supply-demand balance for iron ore will also lower costs, and HRC prices are expected to come under pressure and correct again after a brief rise.

From the perspective of steel mill profits, considering that China's excess steel capacity relies on steel exports for digestion, steel prices need to remain relatively low to support price competitiveness and orders, which will also limit the upside potential of Chinese steel prices. Steel mill profits are expected to remain at low, marginal levels in the second half of 2026.