en.Wedoany.com Reported - On July 1, 2026, BigMint data showed that the export index for Indian pellets (Fe 63%, 3-3.5% Al) fell by $1.5 per ton week-on-week, with the East Coast FOB price reported at $97.5 per ton, marking the lowest level since early March 2026.

Pellet prices remained under pressure due to the overall weakness in the seaborne iron ore market. Market sentiment stayed subdued during the assessment period, broadly aligning with the weakening trend in the global iron ore fines market. Seasonal slowdown in Chinese construction activities dampened buying interest, particularly for regular-grade pellets, with demand remaining sluggish.

According to market sources, over the past week, one producer concluded a transaction of approximately 60,000 tons of Fe 64%, 1.5% Al2O3 pellets at a price close to China CFR $123 per ton. Additionally, a batch of regular-grade pellets (Fe 63%, 1.5% Al2O3) supplied by a pellet manufacturer in southern India was booked yesterday at around India FOB $107-108 per ton.

During this publication window, no confirmed trades (0 deals) were recorded for T1 trade on India's East Coast, with the price calculation weight for this category at 0% today. A total of 11 indicative prices were received, of which 9 were used in the index calculation, assigned a 100% weight.

The overall market remains in a downtrend, but Chinese steel mills continue to trade for high-quality low-aluminum materials to pursue better cost efficiency. An international trader commented that Chinese buyers still prefer low-aluminum pellets, but bids for regular-grade materials face pressure due to the weak fines market.

Most buyers indicated acceptable price levels around China CFR $108-110 per ton, while seller offers remained near CFR $117-118 per ton. The widening gap between buyer expectations and seller quotes limited new trading activity. Another market participant noted that the spread has widened over the past few days, making it difficult to conclude new large-volume deals.

This week, pellet inventories at 34 major Chinese ports fell to approximately 6.36 million tons, but market participants noted that pellet stocks have gradually normalized alongside iron ore fines and lump inventories. A Hong Kong trader stated that due to rising coking coal prices, steel mill profit margins have narrowed, prompting mills to become more aggressive in optimizing raw material costs.

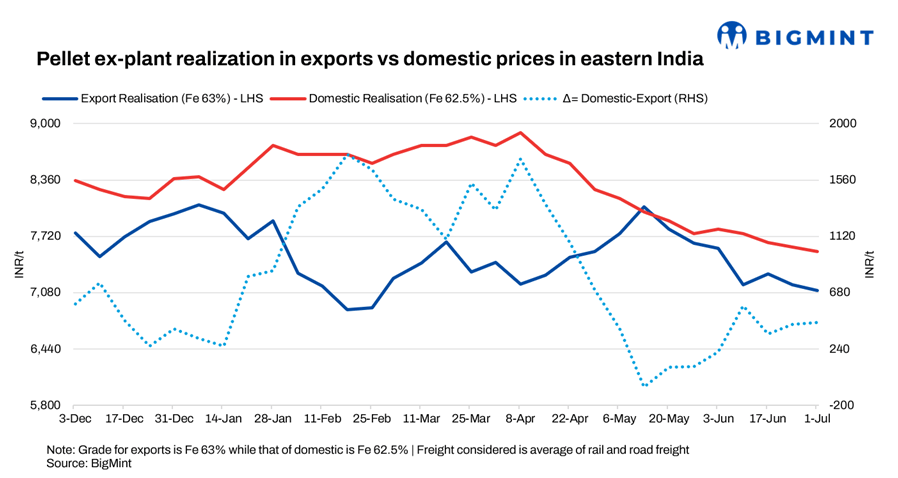

Meanwhile, stronger domestic realization prices continued to keep some sellers away from the export market. Over the past week, several large-volume pellet transactions were reportedly concluded in domestic markets such as Madhya Pradesh and eastern India. A pellet producer noted that current domestic realization prices are above export parity levels, leading many sellers to prioritize the local market over aggressive export orders. A major steel producer recently completed several bulk deals, further alleviating sales pressure and maintaining liquidity.

This week, the price spread between export and domestic realization stood at INR 450 per ton, unchanged from last week. The export realization price (Fe 63%) this week was INR 7,100 per ton ($75 per ton), while the domestic realization price (Fe 62.5%) fell by INR 50 per ton ($0.5 per ton) week-on-week to INR 7,550 per ton ex-works ($79 per ton).

On June 30, the benchmark iron ore fines Fe 61% index rose by $2 per ton week-on-week to China CFR $99 per dry metric ton. Iron ore prices experienced a technical rebound after a prolonged decline, improving market sentiment. As prices fell to near one-year lows, buyers stepped in to take advantage of lower levels, providing market support. Trading activity in the seaborne fines market remained limited, but market discussions boosted confidence in both the spot and futures segments.

On July 1, the Dalian Commodity Exchange (DCE) iron ore futures settlement price for the September 2026 contract was RMB 743.5 per ton ($109 per ton), unchanged from last week.