en.Wedoany.com Reported - AI servers are accelerating the growth rate of the PCB industry: while standard boards are still growing at single-digit rates, high-multilayer boards, HDI, and IC substrates have already surpassed 20%.

In 2026, the global PCB market is expected to grow by 18.8%, exceeding $100 billion for the first time. This figure is striking, but it does not answer the industry's most pressing question: where will new orders and profits flow? The answer lies in the product structure. AI servers require thicker motherboards and lower-loss materials, 1.6T optical modules demand finer circuits, and AI chips need more complex IC substrates. While the overall market is rising, manufacturing difficulty is determining how much of the incremental growth different manufacturers can capture.

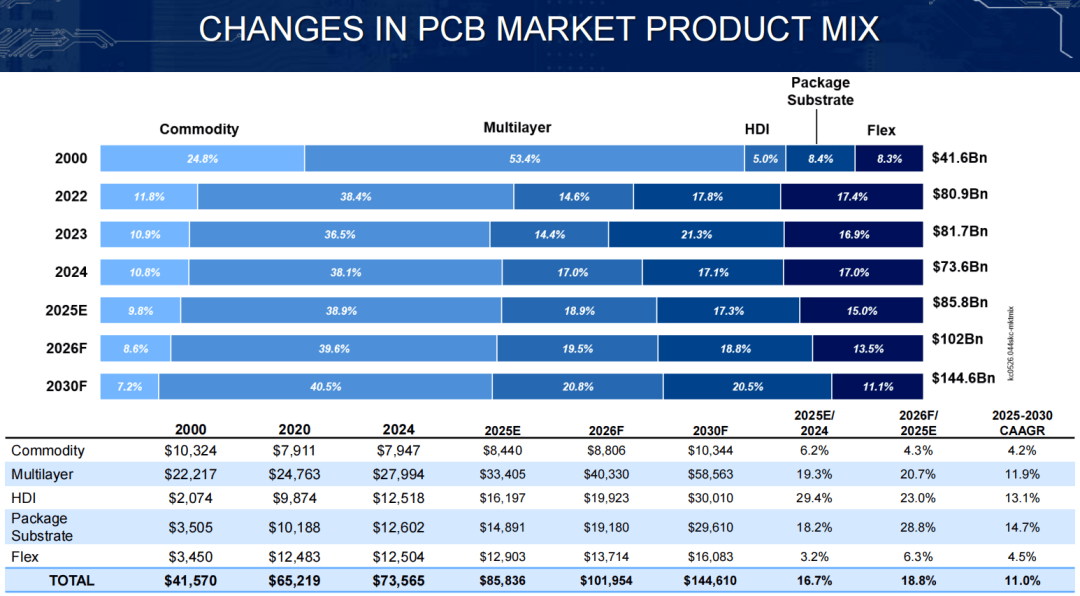

01| Within the Same PCB Market, Growth Rates Differ by Nearly 7 Times

In 2025, global PCB output value reached $85.8 billion, a year-on-year increase of 16.7%. The forecast for 2026 is approximately $101.95 billion, but the performance of various product categories has already diverged significantly:

-

Standard PCBs: approximately $8.81 billion, growing 4.3%;

-

High-multilayer boards: approximately $40.33 billion, growing 20.7%;

-

HDI: approximately $19.92 billion, growing 23.0%;

-

IC substrates: approximately $19.18 billion, growing 28.8%.

The growth rate difference between standard boards and IC substrates is nearly 7 times. By 2030, high-multilayer boards, HDI, and IC substrates are expected to collectively account for over 80% of the market.

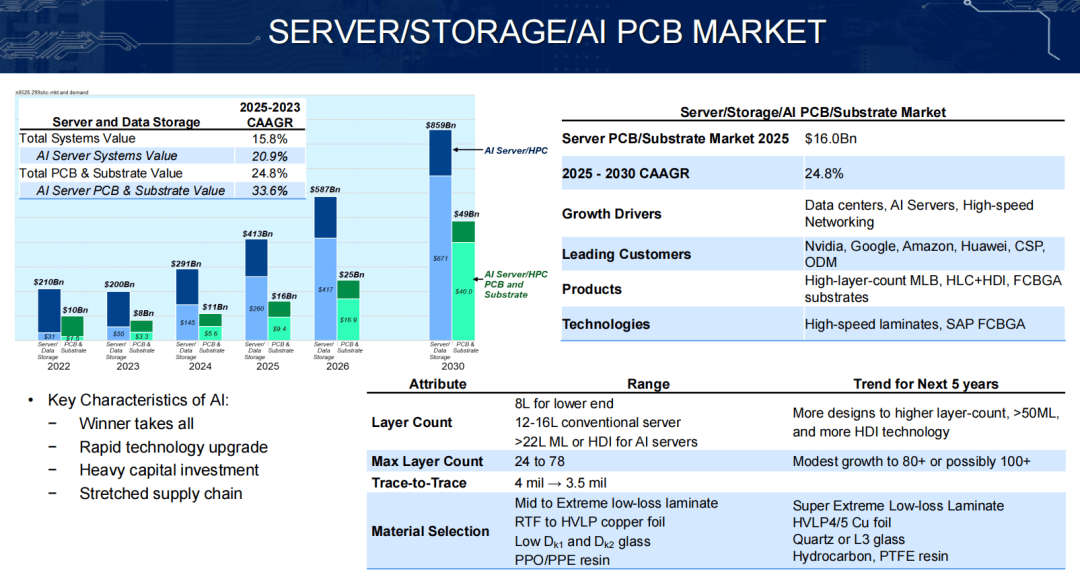

This gap stems from changes in downstream equipment. AI server and storage-related PCBs grew by 47% in 2025 and are expected to increase by another 53% in 2026; wired network PCBs are projected to grow by 45% over the same period. In 2025, AI server and storage-related PCBs and substrates have already formed a $16 billion market, with a compound annual growth rate of 24.8% expected over the next five years.

As the PCB market enters the $100 billion era, the quality of growth is already determined by the board's layer count, line width, and material grade.

02| AI Server Motherboards: Potentially from 22 Layers to 80 Layers

A standard server and an AI server impose two entirely different sets of requirements on PCBs.

Low-end server motherboards typically have 8 layers, while conventional servers often range from 12 to 16 layers. AI servers generally require more than 22 layers, with some high-end products already reaching 24 to 78 layers. According to current roadmaps, products with over 80 layers may emerge in the next five years, with extreme designs potentially approaching 100 layers.

As boards become thicker, engineering challenges multiply. Each additional lamination requires re-controlling interlayer alignment, board thickness, and warpage; high-speed signals passing through more layers make via stubs and transmission losses more difficult to manage. Line widths must also shrink from 4 mil to 3.5 mil, making back drilling, copper plating, and electrical testing more precise.

Materials must also be upgraded. Copper-clad laminates are transitioning to ultra-low loss grades, copper foil is moving from RTF and HVLP to HVLP4/5, and glass fiber fabric is shifting to low-dielectric materials or even quartz fabric. A small amount of loss may be insignificant in a single line, but within a cluster of tens of thousands of GPUs, it can affect bandwidth, power consumption, and system stability.

Demand is growing rapidly, but ramping up qualified production capacity takes time. High-layer-count PCBs require customer certification, while simultaneously addressing yield rates, material matching, and batch consistency. Building factories is relatively easy, but consistently producing dozens of layers of low-loss boards constitutes effective supply.

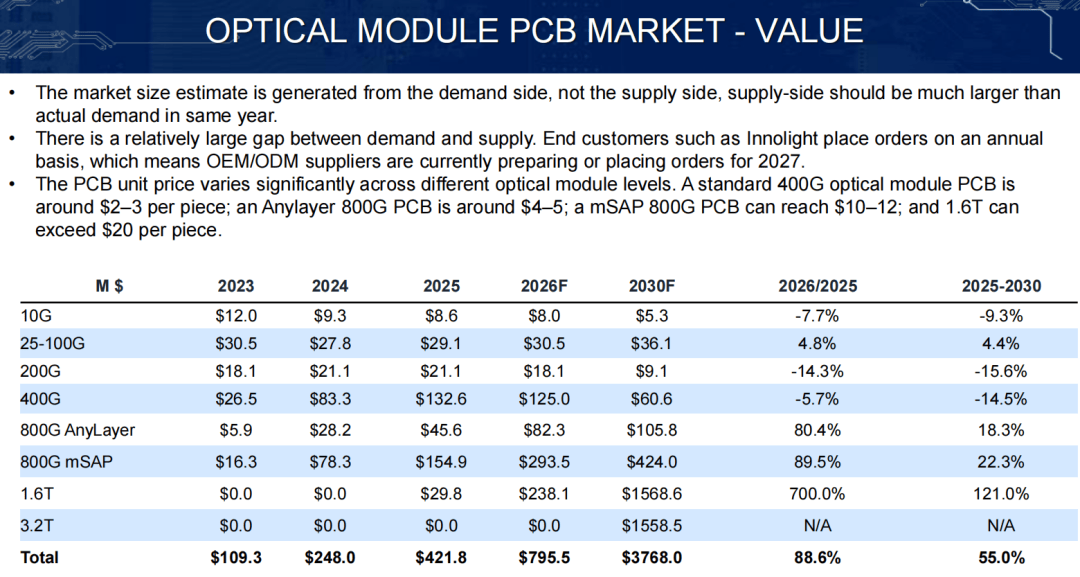

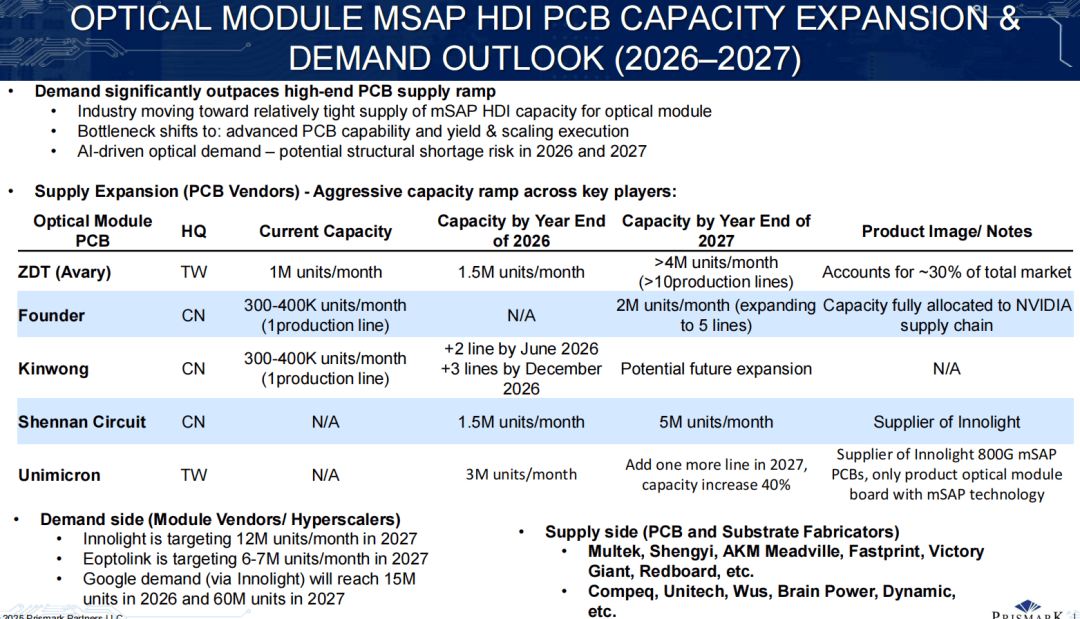

03| 1.6T Optical Modules Push a Small Board Above $20

Another jump in PCB value occurs within high-speed optical modules.

In 2025, the global optical module PCB market was approximately $422 million; in 2026, it is expected to reach $796 million, an increase of nearly 89%. Among this, 1.6T optical module PCBs are projected to rise from $29.8 million to $238 million, a 700% increase in one year.

The speed upgrade directly changes the board's price. Standard 400G PCBs cost approximately $2 to $3, while 800G AnyLayer boards are around $4 to $5; using mSAP fine-line processes, 800G products rise to $10 to $12, and 1.6T boards exceed $20.

This several-fold price difference has clear manufacturing reasons. 1.6T products typically require 12 to 16 layers, M6/M7 materials, and 25/25 micron line width and spacing; 3.2T will further shrink to 15/15 microns, introducing BT or ABF materials and SAP processes. As lines become finer, exposure, copper plating, flash etching, and inspection all require re-establishing process windows.

From 2026 to 2027, mSAP HDI optical module boards may face structural tightness. Supply constraints are concentrated in fine-line yield rates, customer certification, and mass delivery capabilities; simply adding standard HDI production lines will not immediately fill the gap.

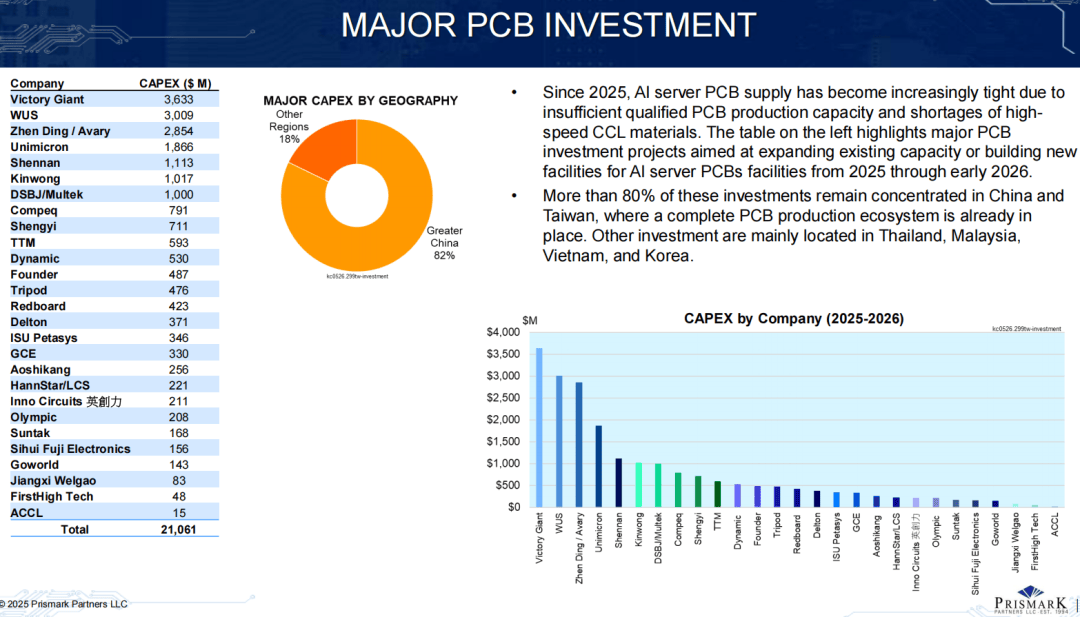

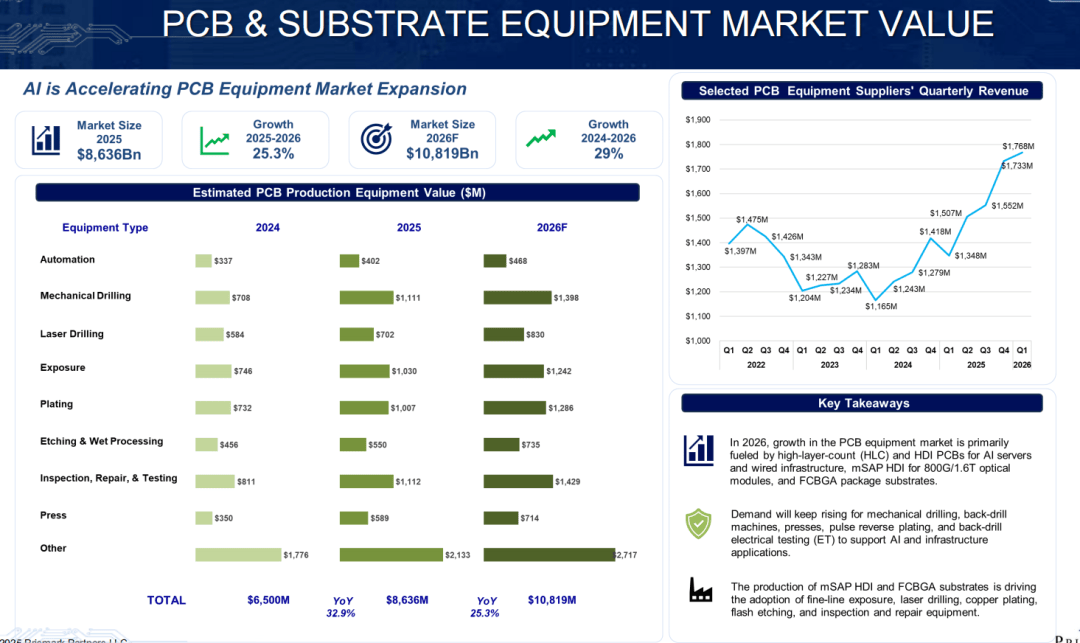

04| $21 Billion in Capacity Expansion: Buying Equipment is Just the First Step

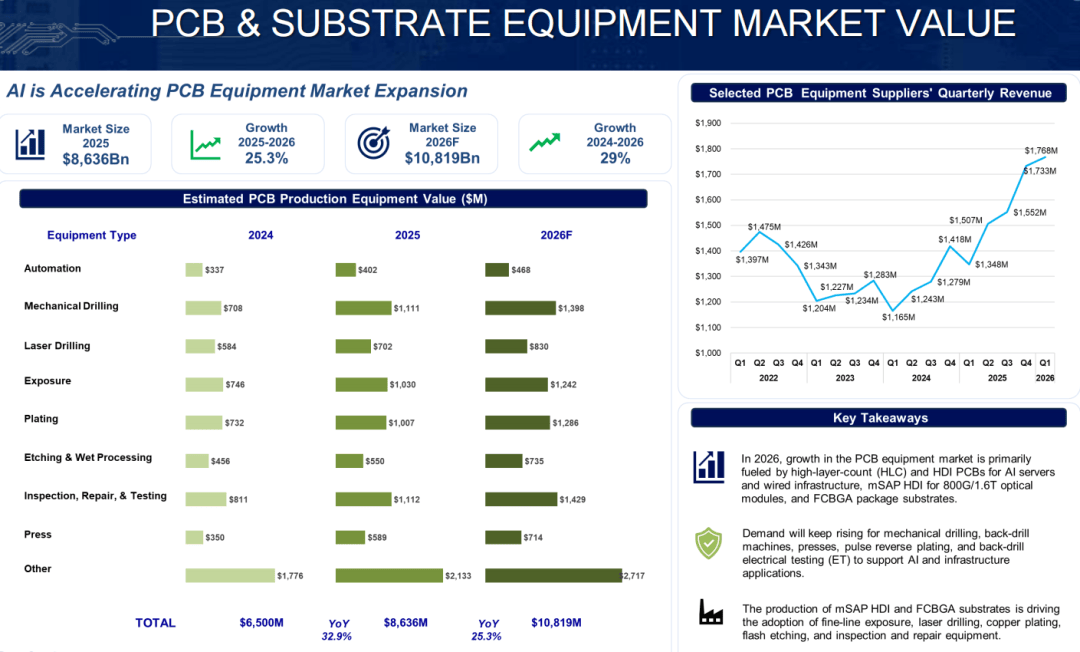

Facing AI orders, the PCB industry has initiated large-scale capacity expansion. From 2025 to 2026, major investment projects total approximately $21.06 billion, with over 80% concentrated in mainland China and Taiwan. The PCB and IC substrate equipment market is also expected to grow from $6.5 billion in 2024 to $10.82 billion in 2026.

Different products drive demand for different equipment. High-multilayer boards increase demand for mechanical drilling, back drilling, lamination, plating, and electrical testing; mSAP and FCBGA require stronger laser drilling, fine-line exposure, flash etching, AOI inspection, and line repair capabilities. IC substrates, expected to grow by 28.8% in 2026, will continue to drive this round of equipment investment.

The challenge of capacity expansion lies in the mass production phase. Whether M9-grade high-speed materials, HVLP4 copper foil, and low-CTE glass fiber can be stably supplied, whether new production lines can pass certification, and whether yield rates can cover depreciation will all affect the speed of order conversion. $21 billion can quickly add factories and equipment, but mature production capacity still needs to be proven through batches of products.

Conclusion | After $100 Billion, the Industry Begins to Allocate Growth by Difficulty

The total PCB market has surpassed $100 billion, and the growth rate gap between standard boards (4.3%) and IC substrates (28.8%) has also drawn two distinct growth curves.

Whether server boards can be stably produced with over 80 layers, whether 1.6T mSAP can ramp up on schedule, and whether high-speed copper-clad laminates and HVLP4 can keep up with demand—these specific developments will determine the extent to which expansion projects are realized.

The PCB incremental growth brought by AI will ultimately fall on high-difficulty products that can pass certification, maintain yield rates, and achieve continuous delivery.