en.Wedoany.com Reported - SK Square has decided to postpone the initial public offering (IPO) plan for its subsidiary T Map Mobility. Unlike other subsidiaries such as 11st, Content Wavve, and ONE store, which faced hurdles in going public and subsequently entered a sale process, T Map Mobility has been retained as it is considered a core pillar of artificial intelligence (AI) data assets.

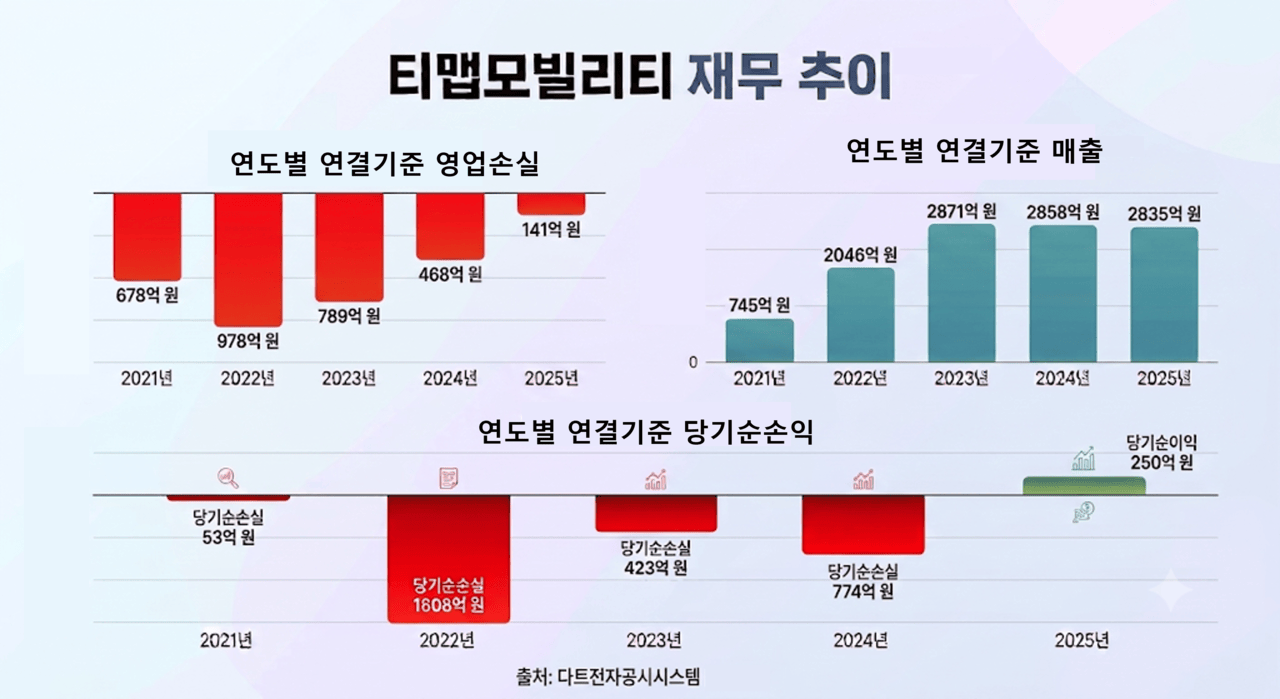

Since its spin-off from SK Telecom (SKT) in 2020, T Map Mobility has yet to achieve an annual operating profit surplus. According to data from the Financial Supervisory Service's electronic disclosure system, its sales on a consolidated basis increased from KRW 74.5 billion in 2021 to KRW 204.6 billion in 2022 and KRW 287.1 billion in 2023, before declining to KRW 285.8 billion in 2024 and further to KRW 283.5 billion in 2025. Despite revenue growth, the company's loss-making structure persisted, with operating losses on a consolidated basis amounting to KRW 67.8 billion, KRW 97.8 billion, KRW 78.9 billion, KRW 46.8 billion, and KRW 14.1 billion from 2021 to 2025, respectively. Net profit for the period also remained in deficit, fluctuating significantly; in 2022, net losses surged to KRW 160.8 billion due to accounting factors such as equity method valuation losses related to Uti and the recognition of additional liabilities for its stake in Uber. This figure dropped to KRW 42.3 billion in 2023, then rose again to KRW 77.4 billion in 2024, showing repeated volatility.

As of the end of 2025, T Map Mobility's accumulated deficit carried forward reached KRW 207.4 billion. However, in 2025, the company achieved a net profit of KRW 25 billion, turning profitable, primarily driven by a gain of KRW 49.7 billion from the disposal of non-current assets held for sale generated during the year.

Against this backdrop, Lee Jae-hwan (이재환) took office as CEO early last year. He graduated from Yonsei University's Department of Computer Science and earned a master's degree in Management Engineering from the Korea Advanced Institute of Science and Technology (KAIST). He joined SK's Management and Economics Research Institute in 2004 and later served as the head of the T Map Parking Business Team within SK Telecom's mobile business division. When the company was spun off at the end of 2020, he joined as a founding member, subsequently serving as Head of Growth Strategy and Chief Strategy Officer (CSO). While serving as CSO in 2023, Lee stated plans to pursue an IPO by 2025 and aimed to achieve a turnaround to profitability in 2024 to support this goal. In the second half of 2023, he also launched new services, outlining a vision to evolve beyond navigation into a comprehensive mobility platform.

After taking office, Lee focused on improving the company's fundamentals by streamlining non-core divisions. To adjust the financial structure, he successively sold stakes in Carrot General Insurance (KRW 36 billion) and Uti, a joint venture with Uber (KRW 57 billion), and booked proceeds from the sale of stakes in Seoul Airport Limousine Bus (KRW 60 billion) and the designated driving intermediary service Good Service (KRW 14 billion) as accounting profits. However, this is closer to a short-term effect from equity sales, and the company still requires supplementary measures to stabilize long-term value, remaining far from its target of KRW 600 billion in annual sales.

When T Map Mobility attracted pre-IPO investments in 2021, it was valued at KRW 1.4 trillion, with the IPO scheduled for 2025 as a condition. Subsequently, to boost its valuation to KRW 4.5 trillion, the company acquired Seoul Airport Limousine Bus and YPL, among others, but performance growth was delayed. At the end of 2025, major shareholder SK Square extended the IPO deadline agreed upon with financial investors (FIs) by two years to 2027, with the FIs consenting to the extension citing performance improvements. However, given current performance, maintaining the initial investment valuation or setting a higher public offering price is not easy. Analysts suggest that SK Square's reason for not selling T Map Mobility lies in securing AI data infrastructure. Based on driving data from over 15 million monthly active users (MAU), the company has launched services such as an AI-powered location recommendation service and an insurance discount service based on driving habit data.

Industry insiders note that T Map is a leading company in the navigation sector, having positioned itself as an AI mobility company, with the vast amount of driver data being a key advantage. Market attention is focused on the extended deadline of 2027. Whether T Map Mobility can diversify its profit model and break the trend of accumulated losses by the deadline will depend on the success of its data business and achieving profitability through cost efficiency.