en.Wedoany.com Reported - Inspur Information's 2026 semi-annual performance forecast shows that China's computing hardware industry is reversing its profitability difficulties. The announcement indicates that the company expects net profit attributable to shareholders of the listed company in the first half of the year to reach 2.6 billion to 3.1 billion yuan, a year-on-year increase of 226% to 288%. Even after excluding non-recurring gains and losses, the net profit excluding non-recurring items also recorded a high year-on-year growth of 206% to 280%, eliminating the impact of one-time gains outside the core business.

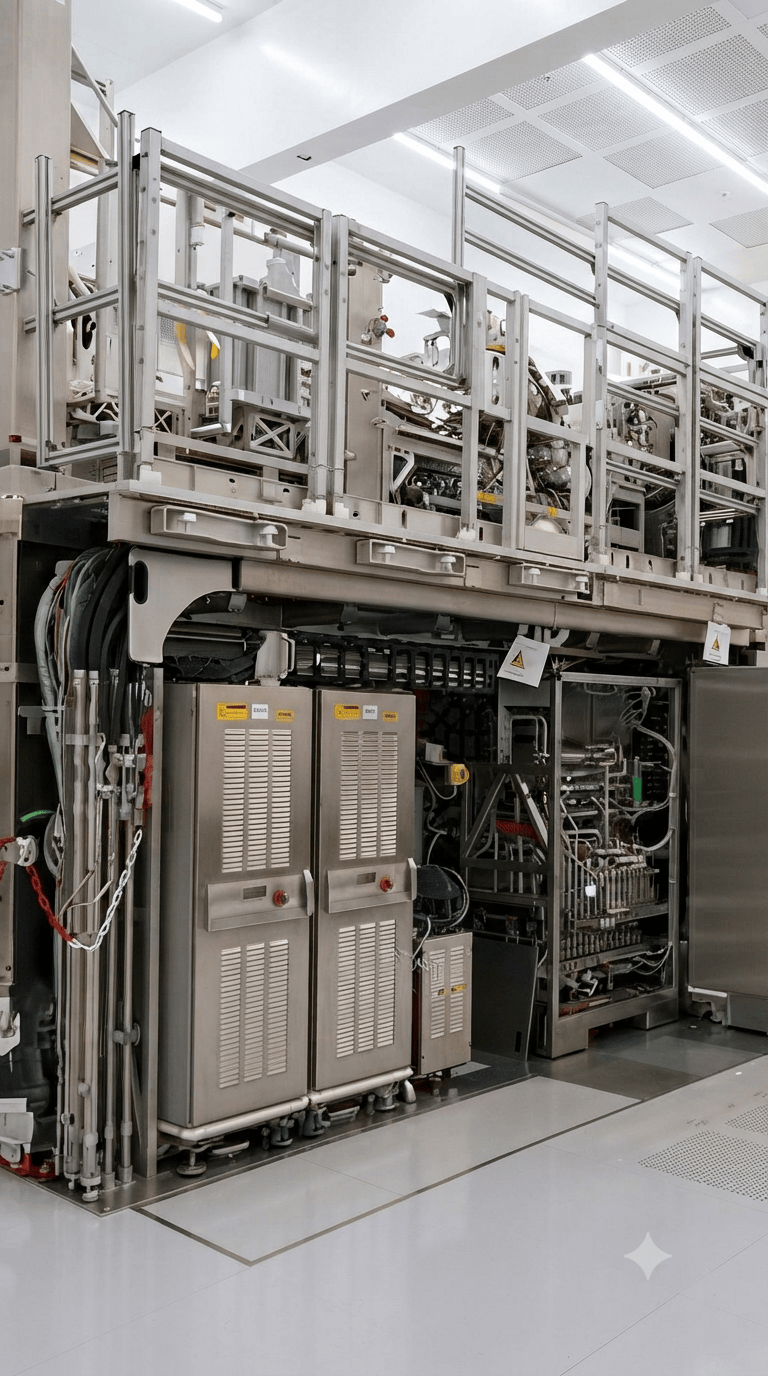

Looking at quarterly data, Inspur Information's single-quarter profit in the second quarter has already approached the full-year profit level of 2025. In the past few years, Chinese server OEMs have suffered from extremely low profit margins due to product homogeneity and fierce price wars, even being labeled as "low-margin OEMs." This significant profit growth is primarily driven by shipments of AI servers and high-priced liquid-cooled models.

Comparing recent disclosures from various manufacturers, the expansion of profit margins is becoming a common industry-wide phenomenon. Xingyun Technology's semi-annual results for the same period show that its computing business revenue grew up to 604% year-on-year, and it recently signed a long-term computing services contract worth 5.5 billion yuan. Its overseas factory in Thailand has also entered mass production. Super Fusion officially launched its IPO on the ChiNext board in early July, planning to raise 8 billion yuan. Its prospectus shows that AI server revenue has exceeded 50%, with its main products being large-scale intelligent computing clusters. Sugon disclosed an 8 billion yuan convertible bond fundraising plan in June, with all funds used to invest in AI training and inference servers and liquid-cooled clusters. Official data shows that Sugon's liquid-cooled server revenue grew 180% year-on-year.

Supporting the profit flexibility of server OEMs is the simultaneous improvement in multiple dimensions, including demand, products, and costs. On the demand side, major Chinese internet companies and the three major telecom operators have successively entered a new cycle of intelligent computing center construction, with billions of yuan in computing capital expenditure translating into orders for ten-thousand-card clusters for midstream server manufacturers. Meanwhile, overseas cloud vendors are accelerating their self-developed computing layouts. AWS raised its shipment forecast for self-developed Trainium ASIC servers in the third quarter of 2026 by 20% to 30%, while Google, Microsoft, and other vendors continue to increase investment in computing infrastructure. On the product side, traditional air-cooled general-purpose servers have low technical barriers and severe homogeneity, resulting in thin profit margins. However, with the widespread adoption of AI large model training and high-load inference scenarios, high-power computing equipment demands significantly higher heat dissipation and stability, leading to sustained explosive demand for high-performance AI servers and liquid-cooled servers tailored for high-end scenarios. At the World Artificial Intelligence Conference (WAIC) in Shanghai on July 7, Huawei announced that it would officially unveil the Atlas 950 SuperPod ten-thousand-card super node on July 17. This architecture supports up to 8,192 Ascend NPU fully interconnected, directly driving orders for upstream components such as high-speed connectors and switch chips from Chinese manufacturers. On the cost side, according to research data from TrendForce, the contract price of general-purpose DRAM is expected to increase by 13% to 18% quarter-on-quarter in the third quarter of 2026, while NAND Flash contract prices are expected to rise by 10% to 15% quarter-on-quarter.

Against the backdrop of upstream price increases, leading server companies can smoothly pass on cost pressures through long-term locked-in procurement, large-scale orders, and pricing power for high-end products. Small and medium-sized manufacturers, due to weak bargaining power, see their profit margins continuously compressed, with industry orders and profits further concentrating among top players. However, supply chain risks remain. In early July, market rumors about a delay in the iteration of Nvidia's new-generation Kyber server products caused short-term significant volatility in global PCB and server OEM sectors. Although Nvidia officially denied the rumors later that day, stating that its roadmap remains unchanged, this reflects that the technical routes and shipment schedules of server OEMs are still influenced by overseas chip giants. AWS's upward revision of its shipment forecast for self-developed Trainium ASIC servers by 20% to 30% also indicates that the trend of cloud vendors developing their own chips may lead to long-term diversion of orders for pure GPU servers.

Through the volume growth of AI and liquid-cooled models, China's server industry is moving away from its past low-margin status, with order backlogs and profit recovery supported by real data. The industry's positive trend is clear, but market participants must remain rational and vigilant regarding volatility and the recurring nature of technological breakthroughs.