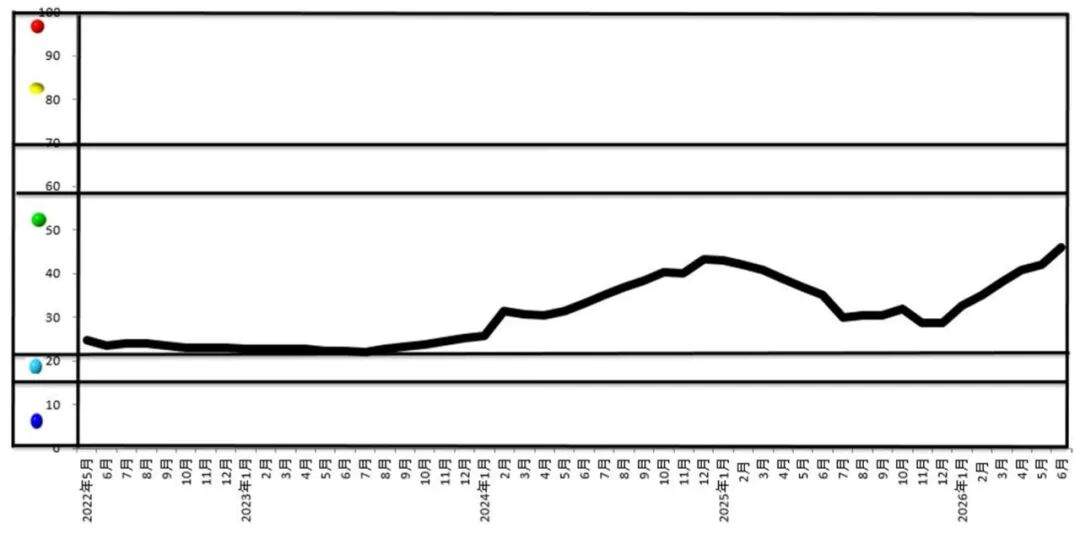

en.Wedoany.com Reported - The latest June 2026 sentiment index released by the China Nonferrous Metals Industry Association shows that the nonferrous metals industry sentiment index for the month stood at 46.1, up 4.1 percentage points from the previous month, placing it in the middle of the "normal" range and maintaining an overall upward trend.

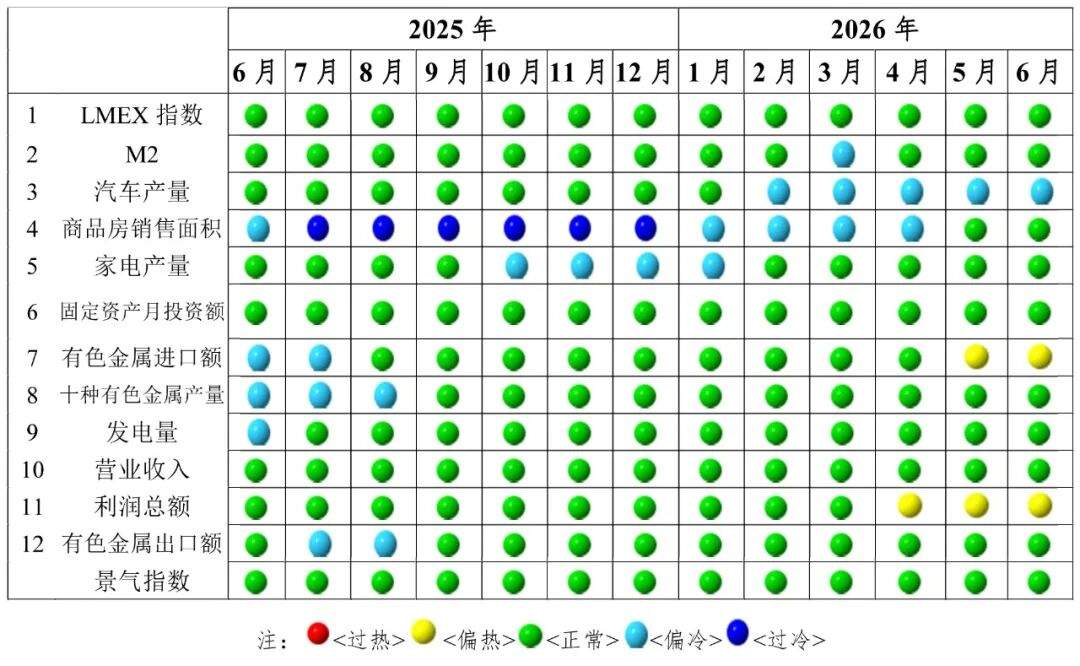

Among the indicators constituting the nonferrous metals industry sentiment index, nine indicators—including the LMEX index, M2 index, commercial housing sales area index, home appliance production index, nonferrous metals fixed asset monthly investment index, nonferrous metals export value index, ten major nonferrous metals production index, power generation index, and operating revenue index—are in the "normal" range; the automobile production index is in the "slightly cold" range; and two indicators—the nonferrous metals import value index and total profit index—are in the "slightly hot" range.

Regarding the leading composite index, it stood at 89.4 in June, up 6.9 percentage points from the previous month. After seasonal adjustment, six indicators—the LMEX index, M2 index, automobile production index, commercial housing sales area index, home appliance composite index, and nonferrous metals import value index—rose month-on-month, with increases of 5.8%, 0.5%, 0.7%, 2.9%, 2.7%, and 3.5%, respectively; these six indicators also rose year-on-year, with gains of 27.3%, 8.4%, 14.7%, 1.6%, 4.6%, and 9.4%, respectively.

The report notes that in June, China's domestic nonferrous metals industry overall exhibited characteristics of "production growth, investment divergence, price volatility, trade divergence, and profit improvement." Internationally, ongoing geopolitical conflicts in the Middle East continue to disrupt the global economy, with energy prices fluctuating at high levels and a pattern of low growth and high inflation persisting. The United Nations' World Economic Situation and Prospects 2026 Mid-Year Update has significantly revised its global inflation forecast upward from 3.1% at the beginning of the year to 3.9%, while the International Monetary Fund (IMF) has warned that global inflation could reach 4.4% in 2026. By region, U.S. employment has weakened slightly but inflation remains high, with the Federal Reserve maintaining high interest rates throughout the year; the Eurozone faces weak domestic demand, leading the European Central Bank to passively raise interest rates by 25 basis points in June; Japan has raised rates slightly due to imported inflation shocks; and India maintains high growth, with a full-year growth forecast of 6.4%. Domestically, China's economic sentiment has marginally improved, with the Manufacturing Purchasing Managers' Index (PMI) rebounding to 50.3%, up 0.3 percentage points month-on-month, returning to expansion territory; the production index at 51.4% and new orders index at 51.2% both improved, with new export orders crossing the boom-bust line; the non-manufacturing PMI stood at 50.2%, slightly up; however, the small enterprise PMI was 48.2%, continuing to contract. On the price front, upstream crude oil prices have fallen periodically, the Producer Price Index (PPI) has slowed its upward pace, and the Consumer Price Index (CPI) has stabilized year-on-year in a moderate range of 1.2%.

At the industry level, driven by industrial activity expansion and policy measures, nonferrous metals production remained generally stable in June. According to data from the National Bureau of Statistics, the value-added industrial output of enterprises above a designated size in the nonferrous metals industry fell by 3.4% year-on-year in May, with the mining and beneficiation segment maintaining positive growth of 3.4%, while the smelting and processing segment declined by 4.5%. In terms of output, production of ten major nonferrous metals in June reached 6.980 million tons, up 2.2% year-on-year; refined copper output was 1.264 million tons, up 2.2%; primary aluminum output was 3.890 million tons, up 1.7%; and total content of six types of mine metals was 2.391 million tons, down 7% year-on-year. Fixed asset investment showed structural divergence, with investment in the nonferrous metals industry from January to May growing by 3.0% year-on-year, a slowdown of 2.5 percentage points from the first four months, but still 2.9 percentage points higher than the average growth rate of national industrial investment. Among this, investment in the mining and beneficiation sector grew by 32.6% year-on-year, while investment in smelting and rolling processing fell by 2.3%. In terms of imports and exports, total trade in the nonferrous metals industry from January to May reached $272.27 billion, surging 66.4% year-on-year; imports of copper ore and concentrate totaled 12.275 million tons, down 1% year-on-year, with the decline widening to 17.3% in May alone; cumulative imports of unwrought copper and copper products were 2.013 million tons, down 7% year-on-year; while exports of unwrought aluminum and aluminum products continued to grow, with cumulative exports reaching 2.687 million tons, up 9.6% year-on-year, and May exports alone at 634,000 tons, with a growth rate of 12.7%.

Market price trends showed significant divergence. In June, the average LME tin price rose 54.9% year-on-year, while LME copper and aluminum increased by 38.9% and 31.3%, respectively; lead was the only traditional industrial metal to decline, with its average LME price edging down 0.4%. In the precious metals sector, the average London silver price surged 154.4% year-on-year, far outpacing gold. New energy metals saw a hot market, with the average price of domestic lithium carbonate futures soaring 141.6% year-on-year, and spot prices rising over 155%; in contrast, the average price of industrial silicon futures fell 7.8% year-on-year, with structural oversupply in the industry suppressing prices. Industry profitability data showed significant improvement, but the sustainability of growth is insufficient. From January to May, 12,324 enterprises above a designated size in the nonferrous metals industry reported total operating revenue of 4.7687 trillion yuan, up 22.5% year-on-year, and total profits of 353.42 billion yuan, up 110.5% year-on-year. By segment, profits at smelting enterprises grew by 122.1%, while profits at mining and processing enterprises increased by 93.9% and 95.1%, respectively. The report points out that this round of profit growth has mainly relied on the dividend from rising commodity prices, with a weak foundation for endogenous growth; long-standing issues constraining the industry persist, including reduced domestic primary mineral production, widening resource supply gaps, processing fees for copper, lead, and zinc falling to negative levels, underutilized capacity at recycling enterprises, and intense competition in the deep processing segment.