Executive Summary

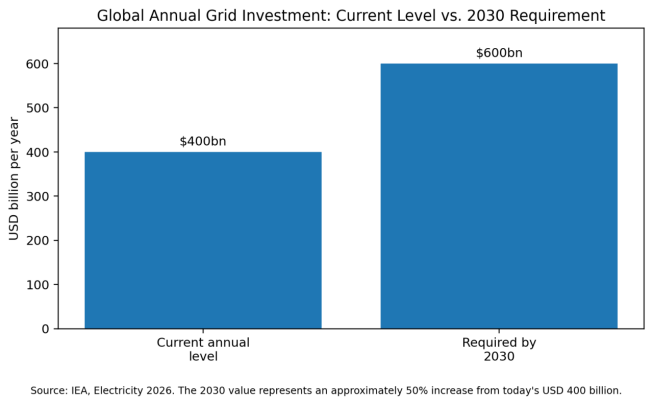

Global switchgear demand is entering a multi-year expansion cycle. Electricity consumption is rising, renewable generation is being connected at distribution and transmission levels, industrial facilities are electrifying, data centers require high-density and highly reliable power distribution, and utilities are replacing aging equipment. The International Energy Agency estimates that annual global grid investment must rise by roughly 50% from today's approximately USD 400 billion to around USD 600 billion by 2030. Switchgear is a critical beneficiary because nearly every new substation, feeder, renewable plant, data center and industrial power system requires protection, isolation and control equipment.

The market is not a single homogeneous category. Low-voltage switchgear is driven by commercial buildings, factories, data centers and distributed energy. Medium-voltage equipment is central to utility distribution, renewable plants, mining, rail, oil and gas and industrial facilities. High-voltage gas-insulated and air-insulated switchgear serves transmission substations, offshore wind, interconnectors and major generation projects. Pricing, qualification, lead times and supplier structures differ materially across these voltage classes.

The most important technology transition is the move away from sulphur hexafluoride (SF₆). The European Union's F-gas regulation began restricting new medium-voltage equipment up to 24 kV from 1 January 2026, with later dates for higher voltage classes. This does not require immediate replacement of installed SF₆ equipment, but it changes new-project specifications, utility frameworks, service training and supplier qualification. Pure-air, vacuum, fluoronitrile mixtures and other alternatives are becoming central competitive technologies.

For procurement teams, the lowest panel price is no longer an adequate decision metric. Arc-flash performance, short-circuit withstand, internal arc classification, footprint, continuity of service, digital protection, cybersecurity, gas-management obligations, spare parts and local service can dominate lifecycle value. International buyers must compare complete technical and commercial boundaries rather than simply USD per panel.

Key Findings

- Global annual grid investment needs to rise from about USD 400 billion today to roughly USD 600 billion by 2030, creating a strong structural demand base for switchgear.

- EU annual grid spending exceeded USD 70 billion in 2025, approximately double the level a decade earlier.

- The EU's 2026 restriction for new switchgear up to 24 kV is accelerating the commercial shift from SF₆ to pure-air, vacuum and other low-GWP technologies.

- Data centers have become a major demand catalyst for LV and MV switchgear, with manufacturers adding capacity specifically for AI-related load growth.

- Supply risk is increasingly concentrated in circuit breakers, vacuum interrupters, instrument transformers, protection relays, copper busbars, specialty steel and qualified testing capacity.

- Digital switchgear can reduce wiring and improve monitoring, but it creates new requirements for IEC 61850 engineering, cybersecurity, firmware management and workforce capability.

- International procurement is moving from lowest equipment price toward delivered lifecycle value, schedule confidence and regulatory compatibility.

Figure 1. Global annual grid investment requirement through 2030.

1. Market Definition and Segmentation

Switchgear is the integrated equipment used to switch, protect, isolate and control electrical circuits. It typically includes circuit breakers, disconnectors, earthing switches, fuses, busbars, current and voltage sensors, protection relays, control systems and metal enclosures. The product boundary varies by project: some contracts cover only factory-assembled panels, while others include bus duct, protection settings, communication systems, installation, testing and commissioning.

The principal voltage segments are low voltage, medium voltage and high voltage. Low-voltage switchgear commonly serves systems up to 1 kV. Medium-voltage classifications vary by national standard but commonly cover distribution levels from approximately 1 kV to 36 or 52 kV. High-voltage switchgear covers transmission applications above these levels. Within each segment, products may be air-insulated, gas-insulated, solid-insulated, hybrid or metal-enclosed.

Market-value estimates from commercial research firms vary substantially because some include circuit breakers, control panels and service revenue while others count only assembled switchgear. This report therefore avoids presenting a single unsupported global market-size number and instead uses grid investment, manufacturing expansion, regulatory deadlines and end-market demand as more reliable indicators.

|

Segment |

Typical Applications |

Primary Buying Criteria |

Main Market Direction |

|

Low voltage |

Data centers, commercial buildings, factories, hospitals, microgrids |

Short-circuit rating, arc resistance, form of separation, maintainability |

Higher current density, digital metering, modular expansion |

|

Medium voltage |

Utility distribution, renewables, mining, rail, oil and gas, industry |

Internal arc class, continuity of service, footprint, insulation medium |

SF₆-free technology, vacuum interruption, digital protection |

|

High voltage |

Transmission substations, offshore wind, interconnectors, large generation |

Reliability, footprint, seismic duty, insulation coordination, lifecycle service |

F-gas-free GIS, condition monitoring, compact offshore solutions |

2. Global Demand Outlook

The IEA's 2026 grid assessment indicates that meeting electricity demand through 2030 requires annual grid investment to increase by approximately 50% from the present USD 400 billion level. The demand is broad-based: new transmission corridors, distribution reinforcement, renewable interconnections, storage, electric transport, heat electrification and large digital loads all require switching and protection equipment.

Grid investment is not the only driver. Data centers increasingly require double-ended substations, redundant MV distribution, high-fault-duty LV switchgear, generator paralleling equipment and sophisticated monitoring. Eaton announced in 2026 that a new 370,000-square-foot Nebraska facility would manufacture air-insulated and gas-insulated switchgear, explicitly linking the expansion to the AI data-center boom. The company stated that its global manufacturing investments had exceeded USD 1.5 billion since 2023.

Renewables change both volume and specification. Solar and onshore wind projects require repeatable MV collection switchgear, while offshore wind needs compact, corrosion-resistant and often F-gas-free equipment. Energy storage projects add bidirectional fault-current behavior, power-electronics harmonics and demanding protection coordination. Utilities are also installing automated ring-main units and feeder switchgear to improve outage restoration and distributed-energy management.

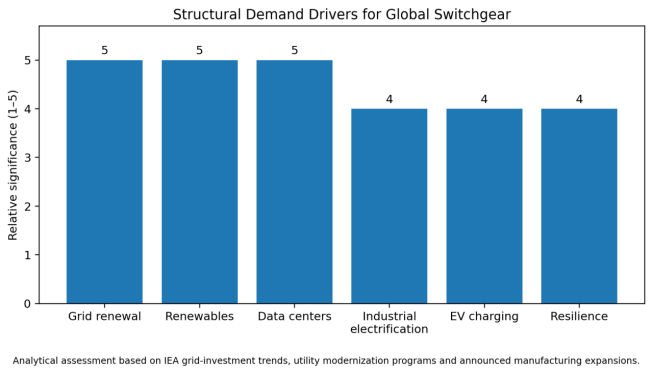

Figure 2. Structural demand drivers for the global switchgear market.

3. Regional Market Analysis

3.1 North America

North American demand is being driven by utility modernization, manufacturing reshoring, data centers, renewable interconnection and resilience investment. The market places strong emphasis on ANSI/IEEE ratings, arc-resistant construction, seismic requirements, UL certification and domestic service capability. Lead-time pressure has encouraged substantial capacity additions. Eaton completed a USD 100 million expansion at its Texas electrical manufacturing site in 2025 and announced a further Nebraska switchgear facility in 2026. Hitachi Energy increased its Pennsylvania investment to more than USD 70 million to expand production of high-voltage equipment, including SF₆-free switchgear and breakers.

The region is commercially attractive but difficult for new entrants. Utility approved-vendor lists, NRTL certification, domestic-content preferences, local engineering support and product-liability exposure create barriers beyond factory price. Data-center buyers also demand rapid schedules, repeatable designs and stringent arc-flash and uptime performance.

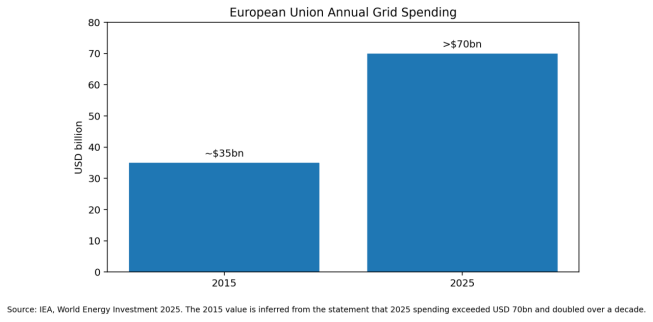

3.2 Europe

Europe combines high grid spending with the world's most consequential switchgear environmental regulation. IEA data indicate that EU annual grid spending exceeded USD 70 billion in 2025, roughly double the amount a decade earlier. Investment is being directed toward renewable integration, cross-border interconnection, distribution reinforcement and replacement of aging assets.

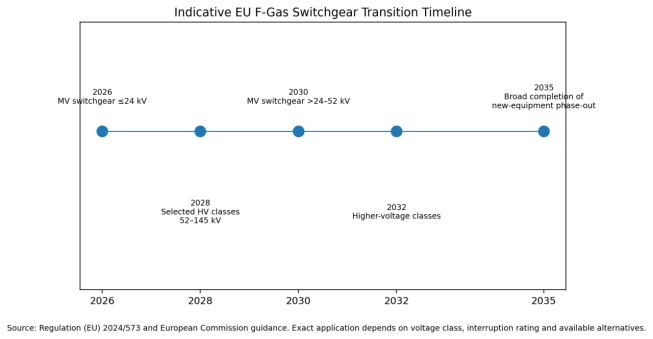

Regulation (EU) 2024/573 creates staged restrictions on fluorinated gases in new electrical switchgear. New MV equipment up to and including 24 kV entered the first major deadline on 1 January 2026. Later dates apply to 24–52 kV and high-voltage classes, subject to technical parameters and exemptions. Utilities are therefore moving framework agreements toward SF₆-free equipment. Schneider Electric and E.ON announced a long-term agreement in 2025 for SF₆-free MV switchgear, illustrating the move from pilot projects to portfolio-scale procurement.

3.3 China and the Wider Asia-Pacific Region

China has one of the world's broadest switchgear manufacturing ecosystems, covering LV panels, MV metal-clad equipment, ring-main units, vacuum circuit breakers, GIS and ultra-high-voltage equipment. Demand is supported by large transmission and distribution programs, renewable-energy bases, industrial electrification, rail transit and data centers. Chinese suppliers can be highly competitive in factory cost and production scale, but export success depends on type testing, destination-country certification, documentation quality and local after-sales capability.

India and Southeast Asia are growth markets because of industrialization, urban power demand, renewable development and grid expansion. Price sensitivity is high, but utilities and industrial buyers increasingly prioritize internal arc classification, tropicalization, local assembly and service coverage. Japan, South Korea and Australia are more mature markets with demanding utility qualification and reliability requirements.

3.4 Middle East and Africa

The Middle East combines utility expansion with oil and gas, desalination, data centers, metro systems and very large renewable projects. Specifications frequently require high ambient-temperature performance, dust protection, corrosion resistance and IEC compliance. Localization programs in Saudi Arabia and other Gulf markets affect supplier strategy. Africa presents significant long-term demand from electrification, mining, renewable projects and urban networks, although project finance, currency risk and service logistics remain constraints.

3.5 Latin America

Latin American switchgear demand is linked to renewable generation, mining, transmission auctions, industrial expansion and replacement of urban distribution assets. Brazil, Mexico, Chile, Colombia and Peru are important markets, but standards, local-content expectations and currency exposure differ. Mining projects often value compact MV equipment, high altitude capability, dust resistance and rapid spare-parts access more than the lowest initial quotation.

Figure 3. European Union annual grid spending, 2015 and 2025.

4. Technology Transition: From SF₆ to F-Gas-Free Switchgear

SF₆ has been widely used because of its excellent dielectric and arc-quenching properties, particularly in compact GIS. Its environmental drawback is severe: equipment manufacturers cite a global-warming potential approximately 24,300 times that of CO₂ and an atmospheric lifetime of up to about 1,000 years. Leakage rates from modern equipment can be low, but the installed base and long equipment life make lifecycle management important.

The transition is not based on a single replacement technology. Medium-voltage equipment increasingly combines vacuum interruption with pure air, dry air or solid insulation. High-voltage alternatives include clean-air systems, vacuum breakers and low-GWP gas mixtures. Technical evaluation must consider voltage, short-circuit current, footprint, ambient temperature, altitude, switching duty and end-of-life handling.

The EU timetable creates a first-mover advantage for suppliers with mature F-gas-free portfolios and type-tested platforms. It also creates transition risk. Buyers must confirm that the selected insulation medium is permitted for the intended commissioning date, that trained service personnel are available, and that spare parts will remain supported for the expected 30–40 year equipment life.

Figure 4. Indicative EU F-gas switchgear transition timeline.

5. Price and Cost Structure

Switchgear prices are difficult to compare globally because scope varies more than the visible panel count suggests. A quotation may include or exclude protection relays, metering, communication gateways, arc-flash sensors, bus duct, batteries, control cables, civil interfaces, installation, commissioning and spare parts. Voltage class, continuous current, short-circuit rating, internal arc classification and enclosure form can change price materially.

Material costs include copper or aluminum busbars, sheet steel or stainless-steel enclosures, insulation, instrument transformers, wiring and surface treatment. The circuit breaker and interruption technology are often the highest-value functional elements. Digital protection and automation add hardware and engineering cost but can reduce copper wiring, installation time and future diagnostic expense.

SF₆-free equipment may carry a premium in early procurement cycles because of newer platforms, lower production scale and project-specific qualification. That premium should not be evaluated in isolation. Avoided gas reporting, leakage management, technician certification, carbon exposure and future retrofit risk can improve lifecycle economics. As production volumes increase, the technology premium is likely to narrow, although high-voltage alternatives will follow a slower cost curve.

|

Cost Element |

Typical Importance |

Main Volatility |

Buyer Control |

|

Circuit breaker / interrupter |

Very high |

Qualified capacity, technology, fault rating |

Standardize ratings; avoid unnecessary customization |

|

Copper or aluminum busbars |

High |

Metal prices, current density, thermal design |

Use transparent metal clauses; compare temperature rise |

|

Enclosure and structural steel |

Medium |

Steel price, corrosion class, arc-resistant design |

Define environment and internal arc requirements clearly |

|

Protection, control and sensors |

Medium to high |

Semiconductors, brand selection, engineering hours |

Standardize relay families and communication architecture |

|

Testing and certification |

Medium |

Type-test availability, witness requirements |

Accept valid test evidence where standards permit |

|

Logistics and installation |

Project-dependent |

Panel dimensions, route, local labor, outage windows |

Separate delivered scope and commissioning responsibilities |

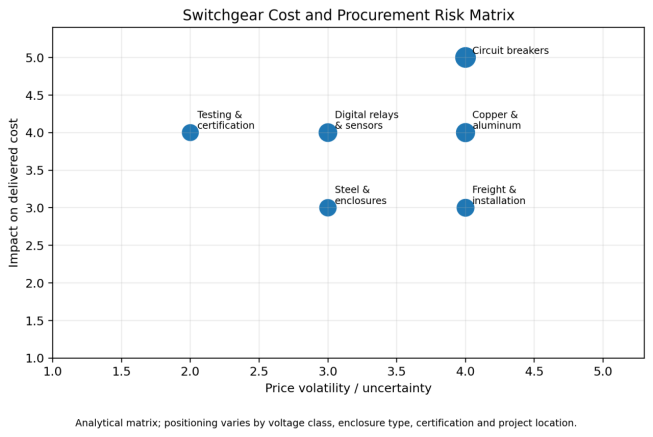

Figure 5. Switchgear cost and procurement risk matrix.

6. Supply Chain and Manufacturing Capacity

The switchgear supply chain is more specialized than the metal enclosure suggests. Critical inputs include vacuum interrupters, molded insulation, high-voltage bushings, instrument transformers, protection relays, current sensors, operating mechanisms and tested circuit-breaker platforms. A shortage in one qualified component can delay a complete lineup.

Factory bottlenecks include sheet-metal fabrication, busbar processing, breaker assembly, dielectric testing, high-power short-circuit testing and customer witness tests. High-voltage GIS requires specialized pressure vessels, gas handling, clean assembly and extensive testing. Expansion announcements from Eaton and Hitachi Energy indicate that producers expect demand pressure to persist rather than normalize immediately.

International procurement adds shipping, packaging, moisture control, site storage and local commissioning risk. Large GIS bays and long LV/MV lineups can require split shipment and field assembly. Buyers should verify who owns alignment, bus-joint torque, protection settings, primary injection, partial-discharge testing and energization support.

7. Digital Switchgear and Smart-Grid Integration

Digital switchgear replaces part of the conventional copper-based measurement and control architecture with sensors, digital communication and intelligent electronic devices. IEC 61850 enables interoperable substation communication, while condition monitoring can track breaker timing, coil current, partial discharge, temperature and gas density.

The business case is strongest where reduced wiring, smaller control rooms, faster commissioning and predictive maintenance have high value. Utilities and data centers can use digital data to identify deterioration before failure and to improve asset utilization. However, the benefits depend on disciplined system engineering.

Digitalization introduces cybersecurity and obsolescence risks. Procurement specifications should define network segmentation, access control, firmware governance, time synchronization, data ownership, software support and replacement strategy. A digitally advanced panel with weak lifecycle software support can create higher TCO than a conventional design.

8. International Standards and Certification

Global switchgear procurement must begin with the applicable standards regime. IEC 62271 is the principal family for high-voltage switchgear and controlgear, while IEC 61439 applies to LV assemblies. North American markets commonly use IEEE/ANSI standards together with UL certification. Internal arc classification, temperature rise, short-time withstand current, dielectric performance, seismic qualification and environmental testing must match the destination market.

|

Area |

Typical Standards / Requirements |

Procurement Risk |

|

IEC MV/HV markets |

IEC 62271 series, internal arc classification, local utility specs |

Assuming one type-test certificate covers a materially different configuration |

|

IEC LV markets |

IEC 61439 design verification, temperature rise, short-circuit withstand |

Confusing component certification with assembly verification |

|

North America |

ANSI/IEEE ratings, UL listing, arc-resistant classifications |

Offering IEC equipment without required NRTL approvals |

|

Digital substations |

IEC 61850, time sync, cybersecurity requirements |

Interoperability gaps and unclear firmware responsibility |

|

Environmental compliance |

EU F-gas rules, gas handling and reporting |

Selecting a platform incompatible with commissioning date or service rules |

9. Competitive Landscape

The global market includes diversified leaders such as ABB, Siemens Energy, Schneider Electric, Hitachi Energy, Eaton, Mitsubishi Electric, GE Vernova and Toshiba, alongside strong regional and Chinese manufacturers. Competitive position differs by voltage class: LV markets are more fragmented and channel-driven, while HV GIS requires deeper engineering, testing and installed-base support.

Competition is shifting in five directions. First, suppliers are expanding manufacturing to secure delivery capacity. Second, F-gas-free portfolios are becoming a qualification requirement in Europe and an increasingly important differentiator elsewhere. Third, manufacturers are integrating digital monitoring and service contracts. Fourth, data-center customers value standardized repeatable designs and rapid delivery. Fifth, utilities are using framework agreements to secure capacity across multi-year investment programs.

Chinese manufacturers can compete through cost, scale and broad product portfolios. Their main international challenges are utility qualification, high-power type testing, local certification, documentation, brand bankability and service response. A credible export offer must include destination-standard compliance, transparent sub-supplier lists, local commissioning and enforceable warranty support.

10. Project and Company Cases

|

Case |

Date |

Market Significance |

|

Eaton Nebraska switchgear facility |

2026 |

New 370,000-square-foot AIS/GIS plant linked to AI data-center demand; production expected in H1 2027. |

|

Hitachi Energy Pennsylvania expansion |

2025 |

Investment increased to more than USD 70 million, including capacity for EconiQ SF₆-free HV switchgear and breakers. |

|

Schneider Electric–E.ON framework |

2025 |

Long-term procurement of SF₆-free MV switchgear demonstrates transition from trials to utility-scale adoption. |

|

Feralpi 110 kV F-gas-free substation |

2024 |

Industrial application of clean-air HV switchgear for green-steel production in Germany. |

|

Siemens Energy Hornsea 3 delivery |

2025–2026 context |

Large-volume use of SF₆-free 72.5 kV GIS for offshore wind, demonstrating a mature specialized application. |

11. Total Cost of Ownership

TCO = Purchase + Engineering + Logistics + Installation + Energy Losses + Maintenance + Compliance + Outage Risk − Residual Value

For switchgear, equipment price is only one part of TCO. A compact GIS solution may reduce land and building cost. Arc-resistant construction can reduce personnel and business risk. Withdrawable breakers may simplify maintenance, while fixed designs may reduce initial cost and footprint. The correct choice depends on load criticality, maintenance strategy and expected expansion.

Continuity of service is especially important in data centers, process plants, hospitals and transport systems. The financial impact of a failed breaker, unavailable spare or extended bus outage may exceed the original switchgear purchase price. Procurement evaluations should therefore capitalize outage risk and include spare breakers, relay spares, operating mechanisms and emergency support.

Environmental compliance is becoming a lifecycle cost category. Existing SF₆ assets may remain in service, but owners must manage leakage, recovery, trained personnel and end-of-life handling. For new European equipment, the regulatory timetable increasingly favors F-gas-free platforms.

12. Procurement Recommendations

Define the exact commercial boundary: Separate factory equipment, protection engineering, communication, bus duct, installation, testing, commissioning and spares.

Avoid unnecessary customization: Standard ratings and repeatable layouts reduce price, engineering hours, delivery risk and spare-parts complexity.

Verify type tests: Confirm that certificates apply to the offered enclosure, breaker, current rating, short-circuit level and internal arc configuration.

Evaluate SF₆ compliance by commissioning date: Do not rely only on order date; verify the rules applicable when the equipment is placed into operation.

Score delivery credibility: Review backlog, factory load, breaker supply, test slots and recent on-time performance.

Standardize digital architecture: Specify relay families, IEC 61850 profiles, cybersecurity and firmware support.

Audit critical sub-suppliers: Review interrupters, relays, instrument transformers, bushings and operating mechanisms.

Plan spares and service: Price spare breakers, coils, motors, relays and local response agreements at award stage.

Compare delivered TCO: Include building space, installation, energy losses, compliance, maintenance and outage exposure.

Use staged quality control: Apply design review, factory inspections, FAT, packing checks, site tests and documented punch-list closure.

13. Market Outlook, 2026–2030

The 2026–2030 outlook is favorable for switchgear demand. Grid investment must accelerate substantially, and data-center, renewable, industrial and transport loads are creating parallel demand outside traditional utility procurement. Capacity additions will improve availability in some categories, but qualified high-voltage equipment and project-specific MV/LV assemblies are likely to remain schedule-sensitive.

Europe will lead the regulatory transition to F-gas-free equipment. Medium-voltage adoption will accelerate first because vacuum and air-based alternatives are already commercially mature. High-voltage transition will be more gradual and specification-dependent. Other markets are likely to adopt alternatives through utility decarbonization policies, corporate emissions targets and technology standardization even without identical legal deadlines.

Price competition will remain intense in standardized LV and MV products, particularly where Chinese and regional manufacturers have scale. However, the value pool will increasingly move toward engineered systems, digital protection, arc-safety performance, fast delivery, local service and lifecycle modernization. Suppliers that can combine capacity, certification, environmental compliance and service are likely to outperform those competing only on factory price.

Conclusion

The global switchgear market is supported by a structural rather than temporary investment cycle. Electricity demand growth, grid modernization, renewable integration, data centers and industrial electrification all require more switching and protection capacity. At the same time, the SF₆ transition is changing the technical basis of the market and creating a new round of product qualification and utility procurement.

The market opportunity is therefore not simply more panels. It is a shift toward safer, lower-emission, digitally connected and serviceable electrical infrastructure. Buyers should focus on delivered lifecycle value, regulatory compatibility and schedule certainty. Manufacturers need qualified capacity, credible environmental technology, destination-market certification and local support.

Through 2030, the most competitive suppliers will be those that can standardize where possible, customize where necessary and prove performance across the entire equipment lifecycle.