en.Wedoany.com Reported - On June 5, at the 2026 SMM Indonesia Mining Conference and Critical Metals Conference Tin Forum, hosted by Shanghai Metals Market Information Technology Co., Ltd. (SMM), co-organized by the Ministry of Foreign Affairs of the Republic of Indonesia, the National Economic Council of Indonesia, the Indonesian Nickel Miners Association (APNI), and MMR, with the Jakarta Futures Exchange as a strategic partner, SMM Senior Analyst Jordan delivered a presentation on the theme "Global Tin Market: Price Trends and Future Outlook."

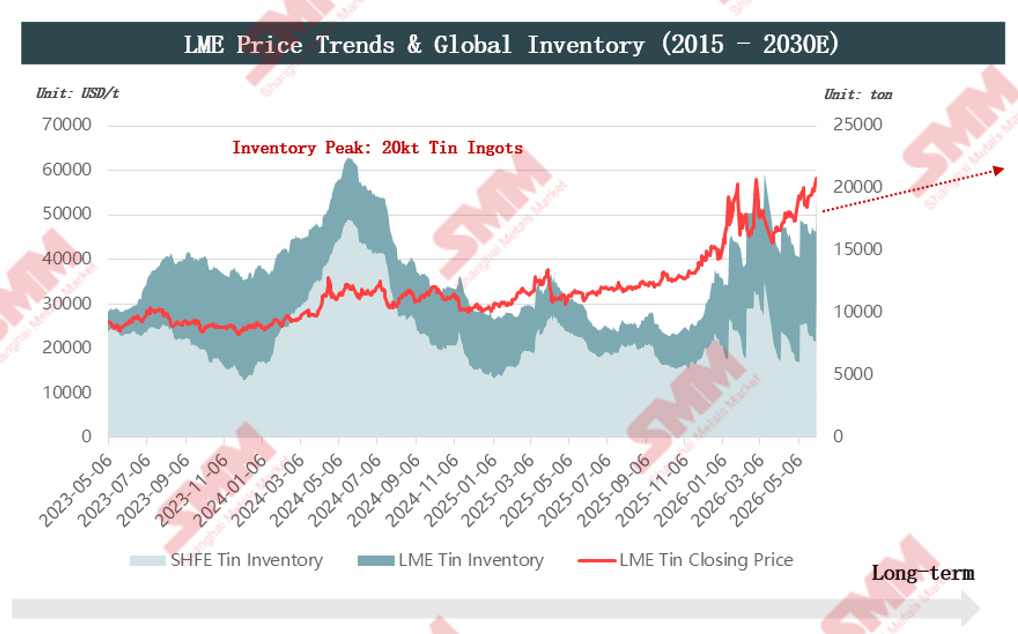

The analyst, drawing on London Metal Exchange price trends and global inventory data, pointed out that supply rigidity at the mine level establishes a long-term price floor, while macro liquidity drives price fluctuations.

On the supply side, supply elasticity is limited, with the global static mine life falling below 15 years and high geographic concentration of reserves. Rising mining output, coupled with shrinking global resources, has accelerated the depletion of reserves in extractable countries. Production at major mines in the Democratic Republic of the Congo (DRC) remains stable, but M23 armed activities have increased market uncertainty. The conflict has affected the Masisi region east of the Bisie mine and the Goma port, disrupting the original tin ore transport route via Goma to Dar es Salaam. To mitigate risks, the Bisie mine has strengthened security, adjusted its freight route northward through Uganda, and ultimately ships to the port of Mombasa, Kenya. Market concerns persist over the potential spread of the M23 conflict, which could disrupt normal mine operations. The DRC recently experienced an Ebola outbreak, with confirmed cases concentrated in Beni and Bunia, near Uganda. While strict epidemic prevention measures have been implemented at the mine and transport stages, with no impact on mining and freight so far, the market remains worried about the outlook for local mineral supply.

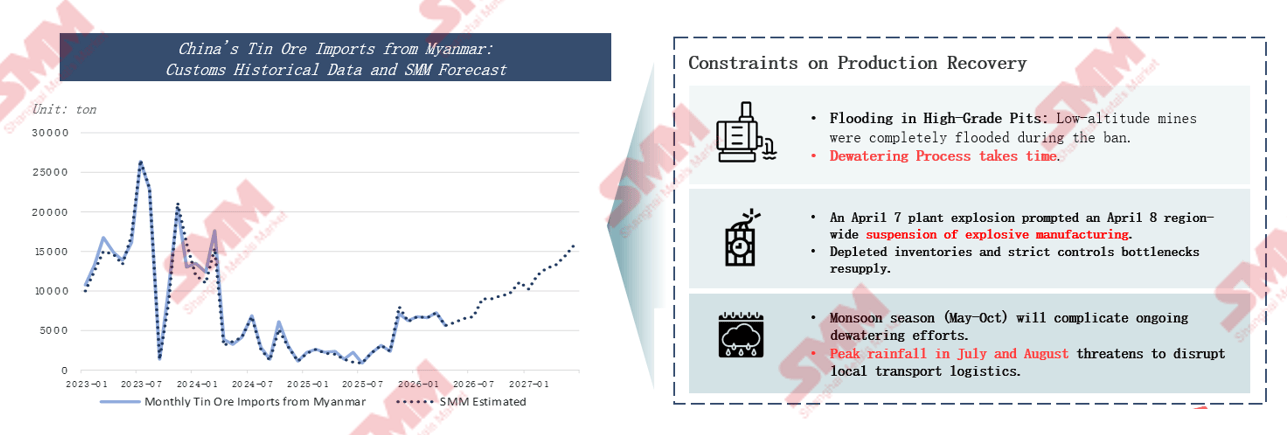

Regarding Myanmar's tin mines, 90% of the country's tin output is concentrated in the Wa State. The Wa State fully suspended tin mining in 2023 and only reissued mining permits in July 2025. Due to the region's rainy climate, extensive water accumulation occurred in the mines during the suspension. After resumption, drainage became a primary challenge, as water affected multiple pits, and cost-sharing arrangements among companies for drainage were delayed. In February 2026, after local authorities issued detailed rules clarifying drainage cost-sharing standards, tin mining in the Wa State officially resumed. Currently, strict controls on civilian explosives in Myanmar, combined with rainy season hindrances to mining and logistics, have slowed the recovery progress, with full resumption expected by 2027.

Global new tin mine projects are scarce, generally with low ore grades and long lead times for implementation. Only three new projects have grades exceeding 1%, posing upward risks to future mining costs. The total scale of projects under construction reaches 173.5 thousand tons, with just four major projects accounting for over 67%. Five new projects in Australia will only bring marginal increases, with limited impact.

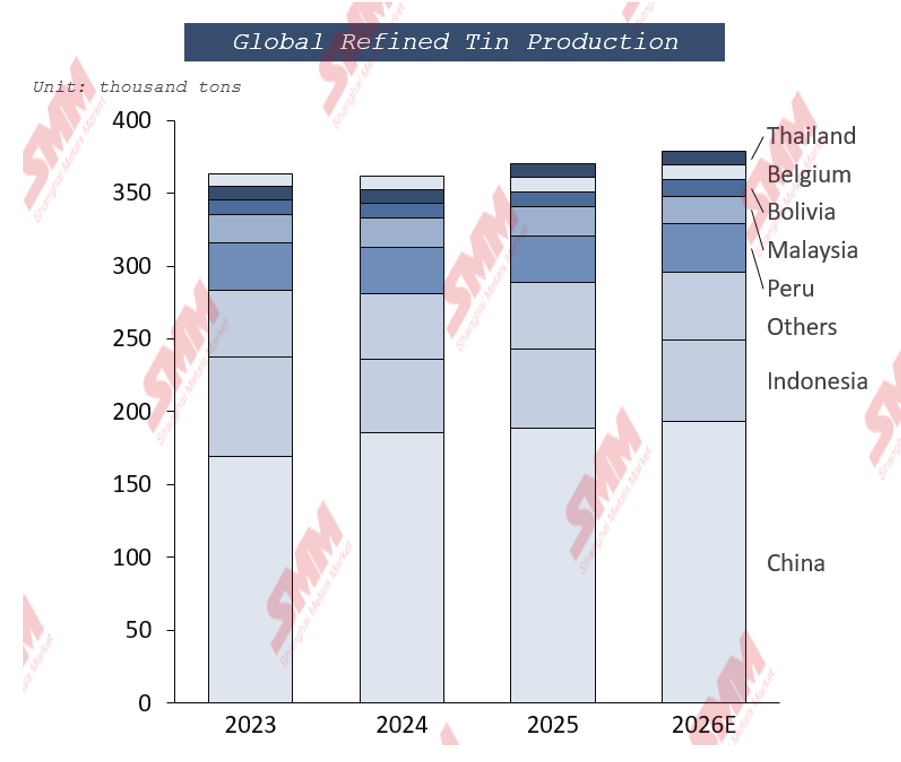

The high concentration of primary tin smelting capacity limits the elasticity of global tin ingot supply. China's tin ingot capacity accounts for 50% of the global total, but its tin ore supply is only 27%, creating a structural imbalance that makes the country heavily reliant on imported ore. Indonesia, the world's second-largest producer, continues to face policy controls that constrain raw material supply. Indonesia's 2026 RKAB quota is expected to be slightly relaxed, but actual utilization remains limited by weather and administrative barriers.

On the demand side, solder remains the primary downstream application for tin, widely used in the electronics sector. Surging demand for AI computing power has significantly boosted shipments of high-performance servers, with electronic solder's tin consumption share expected to reach 38% in 2026. Demand in traditional consumption areas such as tin chemicals and tinplate is stable but lacks growth momentum. By material type, steel and tinplate metal cans accounted for 63.06% of the food can market share in 2025; by can type, three-piece welded cans contributed 58.63% of revenue. Production of PVC heat stabilizers, a key downstream for tin chemicals, remains stable.

From a supply-demand balance perspective, the global tin market is expected to maintain a tight balance, with new mine capacity concentrated for release in 2028.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com