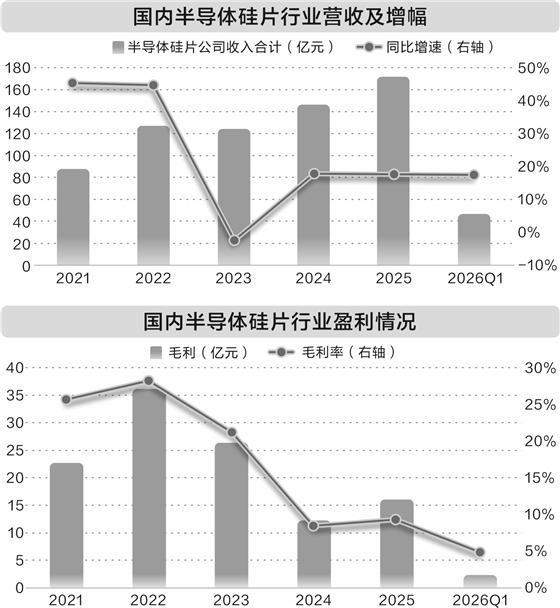

en.Wedoany.com Reported - Since June, the semiconductor silicon wafer sector has seen intensive activity in both the capital market and industry landscape. NSIG announced plans to jointly invest 11.448 billion yuan with the Guosheng Group in its subsidiary, Shanghai Simgui, for the upgrade of 300mm silicon wafer capacity. On June 14, Shanghai Hejing established a SOI (Silicon-on-Insulator) joint venture, entering a high-value-added track. Global silicon wafer giants have initiated two rounds of price adjustments this year. Although domestic silicon wafer companies have not yet fully entered a price hike cycle, management generally believes prices have shown signs of stabilization, with room for recovery expected as demand improves.

As a core substrate material in the midstream of the semiconductor industry chain, silicon wafers are widely used in the manufacturing of integrated circuits, discrete devices, sensors, and other products. From an industry cycle perspective, the semiconductor silicon wafer market entered a moderate recovery channel in 2025, characterized by a divergence of "volume growth and price decline." According to statistics from SEMI, global semiconductor silicon wafer shipment area reached 12,973 million square inches (MSI) in 2025, a year-on-year increase of approximately 5.8%, but total sales revenue for the same period decreased by about 1.2% year-on-year, marking a third consecutive year of decline.

Market conditions have further improved this year. In the first quarter, SEMI estimated that global silicon wafer shipments increased by 13.1% year-on-year, reaching 3,275 million square inches (MSI). On May 10, the three major silicon wafer manufacturers—Shin-Etsu Chemical, SUMCO, and GlobalWafers—simultaneously issued price hike notices: prices for conventional 12-inch silicon wafers rose by approximately 5% to 8%, while high-end specialty wafers for AI/HPC scenarios saw increases of 18% to 22%. GlobalWafers Chairman Hsu Hsiu-lan stated at a performance briefing in late May that, given 12-inch capacity is already fully loaded, coupled with rising costs and increased depreciation, the company is actively negotiating with customers for price increases in the second half of the year.

The core driver of this industry recovery is AI. Li Wei, Director and Executive Vice President of NSIG, recently analyzed in an interview with Securities Times that the rapid development of the AI industry has spurred prosperity in areas such as AI computing chips, memory chips, silicon photonics products, power management chips, and future 6G applications. However, some semiconductor components have been negatively impacted; for instance, mobile phone chips are currently facing pressure from memory supply shortages and rising costs. From the perspective of silicon wafer applications, products related to the AI industry are developing rapidly and are expected to remain in an upward phase for one to two years. Products with low correlation to AI may see tepid performance. The development of 12-inch silicon wafers, driven by AI demand, is outperforming 8-inch wafers, and products like SOI are also performing prominently.

Gao Chengyuan, an industry development consultant at Guangzhou Boshi Information Technology Research Institute, provided a set of data to Securities Times: a single AI server requires approximately 3.8 times the amount of 12-inch silicon wafers compared to a general-purpose server, and HBM (High Bandwidth Memory) consumes three times the silicon wafers of mainstream DRAM (Dynamic Random Access Memory). This "multiplier leverage" has tightened the supply-demand balance for corresponding 12-inch lightly doped polished wafers, heavily doped wafers, and epitaxial wafers. Demand for 8-inch and smaller wafers used in mature process nodes outside the AI field remains relatively stable, creating a structural imbalance. Meanwhile, the capacity expansion cycle on the supply side typically takes 18 to 24 months. According to SUMCO's forecast, AI demand for advanced 12-inch silicon wafers will reach 1 million wafers per month by 2026, accounting for over 10% of total global demand. Concurrently, demand from sectors such as 汽车产业" target="_blank">new energy vehicles, industrial control, and 3D NAND memory is also recovering synchronously, boosting the market sentiment for corresponding 8-inch and 12-inch silicon wafers.

Following price hikes by global leading manufacturers, a few domestic silicon wafer companies have issued price adjustment notices for all categories of epitaxial wafer products, with an increase of 15%. However, the domestic semiconductor silicon wafer market has not yet entered a comprehensive price hike cycle. Xi'an Yicai stated in a research briefing disclosed in late May that current product prices are roughly flat compared to last year and remain at low levels. With sustained strong market demand, full production at its second factory, and an improving customer and product mix, the average selling price is expected to rise. NSIG responded at a performance briefing on May 22 that silicon wafer prices are gradually stabilizing, with expectations of recovery as demand improves. A sales manager at a domestic silicon wafer manufacturer analyzed for Securities Times that the market heat this year has exceeded expectations. Prices for 2025 were already negotiated with major key customers by the end of last year, so prices for these products will remain unchanged. For customers with short-term incremental orders, appropriate price increases are inevitable. Certain AI-related silicon wafer varieties from the company are already experiencing significant supply shortages, prompting accelerated capacity expansion, creating room for price adjustments for these types. The manager also pointed out that silicon wafers are non-standardized products with diverse varieties and uneven batches, requiring structural adjustments based on different situations in practice. If market heat persists into the second half of the year, the company's pricing agreements at the end of this year will also have some room for adjustment overall.

From an industry structure perspective, the global market is dominated by the top five silicon wafer manufacturers, which collectively hold over 80% of the global share, creating multiple barriers in technology, capacity, and customer resources. This is particularly true in the high-end 300mm (12-inch) silicon wafer segment, where they have long monopolized core supply. Against this backdrop, domestic manufacturers are accelerating their deployment. NSIG plans to jointly invest 11.448 billion yuan with its shareholder, Guosheng Group, in its subsidiary Shanghai Simgui, which is the entity responsible for implementing the company's 300mm semiconductor silicon wafer development strategy. By the end of 2025, NSIG's total 300mm semiconductor silicon wafer capacity had reached 850,000 wafers per month, with capacity utilization remaining high. Apart from its recent strategic investment in establishing an SOI joint venture, Shanghai Hejing is also steadily advancing the expansion project for 12-inch semiconductor silicon wafers at its Zhengzhou Hejing Phase II facility, planning to add an annual epitaxial wafer capacity of 720,000 wafers.

According to a forecast by JW Insights, the size of China's semiconductor silicon wafer market is expected to reach $5.867 billion by 2030, with its global share further increasing to 23.21%. In 2025, the localization rate of 12-inch silicon wafers in mainland China was approximately 15% to 20%, and it is expected to rise to 25% to 30% by 2026. As leading companies gradually ramp up production capacity, the process of domestic substitution will further accelerate. Gao Chengyuan believes that the opportunities for the domestic silicon wafer industry lie in the surge in demand for high-end silicon wafers driven by the AI computing power explosion and the space for domestic substitution created by the wave of fab expansion in China. According to SEMI's forecast, 108 new fabs are expected to be built globally by 2028, with 84 in Asia, of which China alone accounts for 47, exceeding half of Asia's new capacity. In the mainstream 22-40nm process node, China's capacity share is projected to increase from 25% in 2024 to 42% in 2028.

Domestic silicon wafer manufacturers also face challenges overseas. Li Wei told Securities Times that, except for a few very high-end silicon wafers, domestic capabilities can already meet the technical requirements for over 80% of global silicon wafers. The company's products are exported to North America, Europe, and Asia, but the global market share of domestic manufacturers remains low. One reason is that the technical threshold for the highest-end silicon wafers has not yet been reached. Another is that geopolitical factors have hindered the pace of overseas market expansion. Compared with international silicon wafer giants, the main gap lies in the lack of a broad customer base, making it difficult to establish long-term, stable supply relationships with many world-class foundries. From a supply chain perspective, while extensive domestic substitution has been achieved in areas such as equipment and materials, some areas remain unconquered, inevitably leading to dependence on others.

Gao Chengyuan pointed out that from a financial perspective, despite impressive revenue growth, the domestic silicon wafer industry as a whole is still in a phase of "high investment" assault. A single 12-inch production line requires investments often reaching tens of billions of yuan, necessitating sustained high-intensity R&D spending. Consequently, related companies generally have not yet escaped loss-making status. According to statistics, in the first quarter of 2026, seven A-share listed silicon wafer companies reported a combined net loss of approximately 2.407 billion yuan, with an average net profit of about -344 million yuan. In the long term, the core challenge for domestic silicon wafer companies is to balance expanding capacity and maintaining technological innovation capabilities while finding a balance between innovation investment and profitability. In the short term, as global silicon wafer price increases are transmitted to the domestic market, coupled with improved capacity utilization and optimized product mix, the industry's profitability is expected to gradually improve.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com