en.Wedoany.com Reported - The European Commission, under the newly introduced Steel Regulation, has officially announced a country-specific tariff quota scheme for steel imports. This scheme will take effect from July 1 to December 31, 2026, replacing the EU safeguard measures that have been in place since 2018.

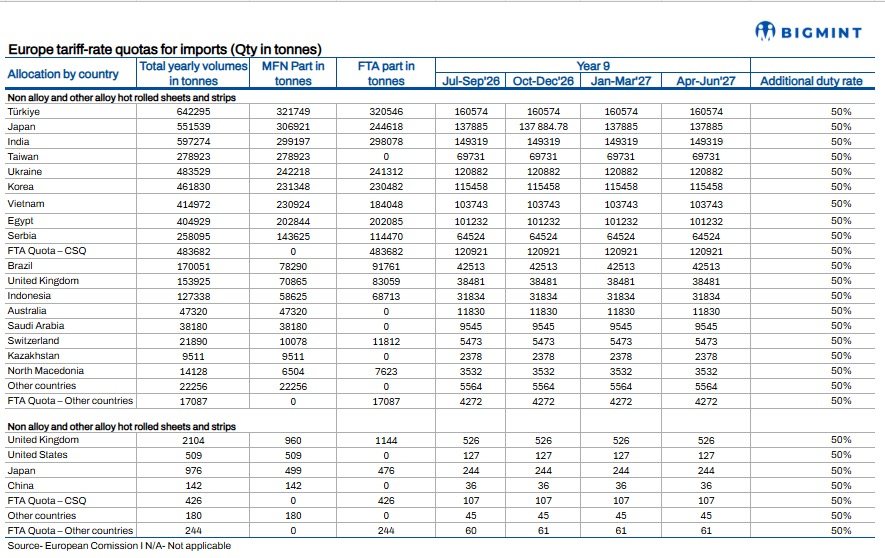

The latest implementing regulation sets a total import quota of 18.35 million tons for 26 product categories, primarily allocated based on each country's share of EU steel imports between 2022 and 2024. It specifies the volume of steel these countries can export to the EU before incurring a 50% tariff on excess quantities. Under the new framework, the EU has reduced the total tariff quota by approximately 47% compared to the previous safeguard mechanism, while increasing the tariff rate on imports exceeding the quota from 25% to 50%.

The EU introduced these measures to address persistent global steel overcapacity, rising import pressure following U.S. tariff increases, and low capacity utilization in the European steel industry. For Indian exporters, these quotas confirm a more restrictive trade environment. Europe remains India's largest overseas steel market, amid slowing demand and the rollout of the Carbon Border Adjustment Mechanism (CBAM).

The new quota framework is structurally divided into two parts: one is the Most Favored Nation (MFN) quota applicable to all eligible exporting countries, and the other is a separate FTA quota established for countries with existing or future Free Trade Agreements (FTAs) with the EU. Under this structure, the European Commission has introduced country-specific quotas, residual quotas, and additional FTA competitive quotas. All quotas will be managed on a first-come, first-served basis, and exporters from FTA partner countries can access additional quota pools after exhausting their respective country-specific quotas.

Notably, Ukraine has received special treatment under this framework due to its current security situation and previous preferential access to the EU market. The regulation also introduces a more differentiated quota management system than previous safeguard arrangements. For hot-rolled coil, the largest product category, the European Commission has established a dedicated quota structure to prevent excessive concentration of imports from a few suppliers while maintaining diversified sourcing options for European buyers. Existing arrangements for steel shipments between Northern Ireland and the UK have also been preserved to ensure continuity of current trade flows.

In terms of major flat products, India has received clear quotas, including for hot-rolled coil (HRC), cold-rolled coil (CRC), galvanized steel, and color-coated products. Although the reduction in quotas reflects the overall shrinkage of the EU import quota pool rather than a decline in India's market share, the stricter quota regime comes at a time when the EU still accounts for the largest share of India's steel exports. In 2025, India's export volumes to Europe declined year-on-year due to weak manufacturing activity in the region, but rebounded in the second half of the year as buyers accelerated purchases ahead of CBAM implementation. Hot-rolled coil remains India's largest export product to the EU, at 1.3 million tons, followed by galvanized steel (820,000 tons) and cold-rolled coil (560,000 tons).

The new quotas are expected to further limit India's ability to expand steel exports to Europe. Unlike in 2025, when Indian steel mills benefited from CBAM-related pre-purchasing and competitive pricing, the smaller quota pool restricts room for additional shipments. The higher 50% out-of-quota tariff also makes exports beyond the quota commercially unattractive, especially for commodity-grade hot-rolled coil. As a result, the EU may become a market where Indian producers focus on maintaining existing business rather than pursuing volume growth. Exporters may increasingly prioritize high-value coated and downstream products, which can better absorb compliance and tariff costs, while limiting spot sales of hot-rolled coil after quarterly quotas begin to saturate.

The stricter EU framework is expected to intensify Indian steel mills' efforts to diversify exports. Some producers had already shifted hot-rolled coil exports to Vietnam in the second half of 2025 amid weak European demand and quota constraints. Markets in Southeast Asia, the Middle East, and Africa may also receive more attention, although their capacity to absorb volumes comparable to the EU remains limited.

The announcement of country-specific quotas removes uncertainty about market access for the remainder of 2026 but also confirms that export opportunities to Europe's largest steel market have narrowed. For Indian producers, the challenge is no longer securing access to the EU market, but maintaining competitiveness within significantly reduced import quotas while managing CBAM-related costs. With hot-rolled coil exports facing the greatest pressure, steel mills may focus on preserving existing customer relationships in Europe while seeking incremental growth in alternative export markets, particularly Vietnam and the Middle East.