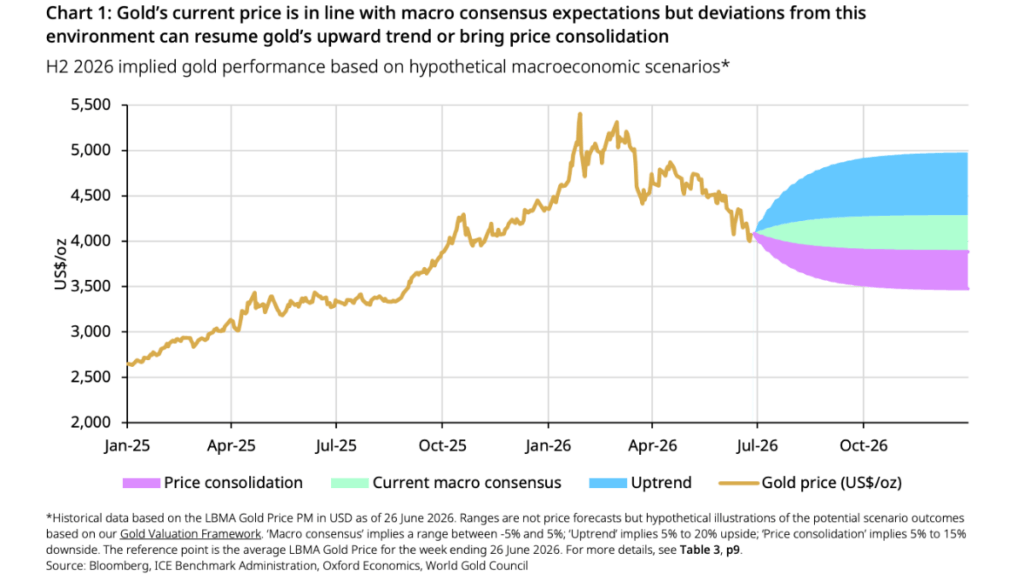

en.Wedoany.com Reported - Gold prices rose 3% to near $4,200 per ounce, driving the Australian mining sub-index up 7.5% in a single day. Local gold prices broke through A$6,000 per ounce, temporarily easing industry pessimism.

The gold price increase was mainly driven by weaker-than-expected U.S. employment data and falling oil prices (progress in ending the U.S.-Iran conflict through negotiations). In the previous two weeks, two concerning U.S. inflation data points had raised rate hike fears, but these have temporarily subsided. Higher interest rates and rate hike expectations are negative for gold, as it yields no income and becomes less attractive relative to cash and bonds in a rising rate environment.

Market sentiment has shifted just as banks began to lower their gold price forecasts. Canaccord Genuity (CG) this week cut its long-term U.S. dollar gold price forecast by 14.3% to $4,747 per ounce and reduced its medium-term forecasts for 2026-2028 by 12%. CG forecasts gold at $4,380 per ounce in 2026 (down from $4,759) and $4,203 per ounce in 2027 (down from $4,902). The long-term silver price was also cut by 11.5% to $72.70 per ounce. CG analyst Tim McCormack downgraded Evolution Mining (ASX:EVN) from Buy to Hold, cutting the target price by 21% from $15.75 to $12.50. CG lowered target prices for large producers by 22% and for mid-tier and junior gold producers by 20%. McCormack noted this was gold's worst quarter since the June 2013 crash, with GDX and GDXJ down 18% and the Australian sub-index down 10%.

For investors viewing gold as a hedge against currency debasement, upside potential remains. The U.S. deficit is at its second-highest level since fiscal 2021, with federal debt expected to exceed $40 trillion by the end of September. By 2036, U.S. government interest payments alone could exceed $2 trillion annually. China has taken advantage of the gold price decline, officially purchasing 810,000 ounces year-to-date, nearly matching its full-year 2025 total of 860,000 ounces. McCormack noted that China's May purchases of 320,000 ounces were the largest monthly total since December 2024.

A team led by Aakash Doshi stated that their bullish view remains unchanged. State Street gold analysts said gold is still heading toward $5,000 per ounce or more in early 2027. The analyst team said the path could be "more bumpy." "We expect gold to potentially rebound to $4,750-$5,500 per ounce over the next 6-9 months (70% baseline), while bearish tactical headwinds increase the probability of gold trading in the $4,000-$4,750 range (25% scenario)," they said in their monthly update. "Strong price support exists at $3,750-$4,000 per ounce, but the $5,500-$6,250 per ounce range (5% bullish scenario) is less likely compared to the January/February macro environment." Global debt has reached a record $353 trillion, with government debt accounting for one-third, also a record. "Positive fiscal and inflationary impulses should continue to support demand for gold as a monetary hedge," State Street experts said. The stock-bond correlation remains higher than the 25-year average before 2021, physical gold demand remains strong, especially from China and emerging market central banks, while global mutual funds and ETFs still hold less than 1% of assets in gold funds. "Well below the 3-10% strategic target we recommend for most portfolios," State Street strategists said. It should be noted that State Street manages an unlisted gold fund, and its bullish commentary should be viewed with caution.

Central bank demand continues to support gold prices, with State Street expecting sovereign net purchases to continue for the 17th consecutive year, ranging between 680-820 tonnes. "Although gold sales by the Russian and Turkish central banks in March were used to address domestic pressures, including funding needs, currency volatility, and budget deficits, these events ultimately reinforced gold's role as a strategic liquid reserve asset," they said. "The ability to mobilize gold during periods of stress can strengthen, rather than weaken, the long-term reserve management rationale for holding gold."

The World Gold Council is more cautious. It does not forecast prices but said gold "could remain range-bound." Its medium-term outlook suggests gold may trade within 5% of its end-June level of around $4,100 per ounce. However, upside potential exists, leading to a "possible breakout." "On the upside, clear catalysts—economic deterioration or a new geopolitical shock, a shift in lower rate expectations, or a wave of dip-buying—could reignite gold's momentum and push it back to $4,500 per ounce or higher," the World Gold Council said. "If signals are strong, gold could rise further. Conversely, in an environment of growth resilience, rising yields, and market calm, gold prices could slide further—a decline of more than 10% from current levels could be cushioned by dip-buying demand. Sustained central bank demand and policy changes in key markets such as India are additional variables that could subtly influence gold's trajectory in the second half of the year."

On the mining company front, several firms reported June (and FY2026) production data. Catalyst Metals (ASX:CYL) rose over 17% on Friday alone, announcing June quarter production of 31,812 ounces at its Plutonic mine in Western Australia, near the midpoint of its full-year guidance range of 100,000-110,000 ounces, with full-year output of 104,000 ounces. Quarterly cash increased by A$46 million to A$323 million. Genesis Minerals (ASX:GMD) ended FY2026 near the top of its guidance, producing 70,767 ounces in the June quarter and 285,400 ounces for the full year, with cash and equivalents increasing by A$258 million to A$520 million at year-end, despite spending A$352 million on M&A, taxes, and exploration. Drilling expenditure will increase significantly from A$40-50 million in 2026 to A$80-90 million in FY2027, with boss Raleigh Finlayson set to outline a strategy to push GMD toward a 500,000-ounce-per-year target in the coming weeks. Vault Minerals (ASX:VAU) announced it had achieved its guidance targets, producing 89,338 ounces in the June quarter and 336,540 ounces for the full year, and restarted underground development at its Sugar Zone mine in Canada on July 1. Vault is merging with Regis Resources (ASX:RRL), ending the quarter with A$842 million in cash and gold holdings (up A$219 million), with no debt or hedging. Northern Star Resources (ASX:NST) sold 433,000 ounces in the June quarter, reaching 1.543Moz for the full year, exceeding its 1.5Moz guidance target. However, this target had been revised down multiple times earlier in the year, leading activist investor Elliott Investment Management to call for a potential sale. NST announced a restructuring this week, with Glencore executive Suresh Vadnagra to replace outgoing Managing Director Stuart Tonkin, and Michael Ashforth to succeed outgoing Chairman Michael Chaney after the November shareholder meeting. Vadnagra will receive an annual salary of A$2.2 million, plus A$1.6 million to compensate for incentives forfeited upon leaving Glencore, which applies even in the event of a change-of-control transaction before his start date of October 5.

Brightstar Resources (ASX:BTR) reported progress on civil works for a new 1.5 million tonne per annum processing plant at its Goldfields project. Open-pit mining at the Lord Byron deposit is expected to begin in late 2026, followed by plant commissioning in mid-2027. The mine will make Brightstar an independent producer in its current form for the first time, producing 75,000 ounces annually, laying the groundwork for BTR's larger Sandstone project. The company previously raised A$300 million in debt and equity for the Goldfields development. It also announced downside price protection for 60,000 ounces of production through put options. "This deferred premium structure maintains a strong balance sheet as we advance the Goldfields project construction, mining ramp-up activities, and Sandstone project exploration and feasibility studies," said BTR Managing Director Alex Rovira. Brightstar shares are down 31% year-to-date but rose sharply this week as gold sentiment recovered.

Iceni Gold (ASX:ICL) announced a A$10 million option and joint venture agreement with South African gold giant Gold Fields. By spending A$5 million over three years, Gold Fields can earn a 51% interest in tenements covering the Everleigh-Tatong target within the 14 Mile Well project in Western Australia, with a minimum expenditure of A$1.5 million in the first two years. By spending an additional A$5 million within the first five years, it can earn a full 70% interest. This is a familiar experience for Iceni boss Wade Johnson, who previously worked on a farm-in deal with Gold Fields while at Lefroy Exploration (ASX:LEX). The deal also extends Iceni's relationship with Gold Fields, which took over a Gold Road Resources farm-in on ICL's Guyer target after acquiring its Gruyere gold mine partner last year. "Gold Fields' commitment validates our belief in the potential for multiple mineralized systems associated with differentiated dolerite sills in the region," Johnson said. "Gold Fields' participation in the joint venture will allow Iceni to accelerate the evaluation of our remaining high-potential targets, which we retain 100% ownership of."