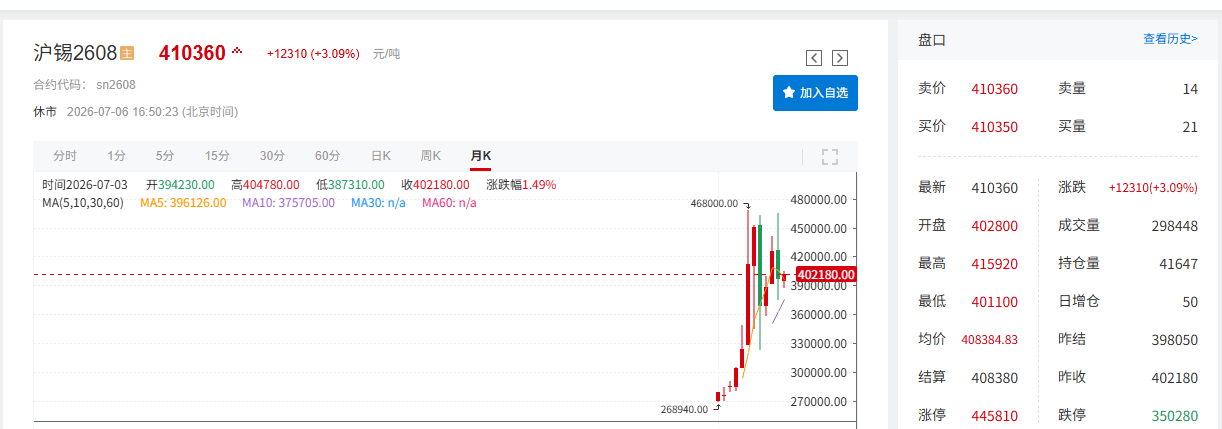

en.Wedoany.com Reported - In June, the rising expectations of a Federal Reserve interest rate hike pushed the US Dollar Index up over 2% for the month. The traditional off-season for the electronics industry led to weak terminal demand. Combined with market doubts about the sustainability of the AI rally and concentrated profit-taking, these factors collectively dragged tin prices down. For the month, Shanghai tin fell 7.08% on a monthly basis, while London tin dropped 6.68%. Entering July, Federal Reserve Governor Christopher Waller stated at the Sintra Forum that inflation expectations were receding, and the US June non-farm payroll data fell short of expectations, cooling rate hike expectations. A rebound in tech stocks further helped stabilize and lift tin prices. As of 16:51 on July 6, London tin was reported at $52,970 per ton, up 1.26%, with a tentative monthly gain of 2.56% for July. Shanghai tin was reported at 410,360 yuan per ton, up 3.09%, with a tentative monthly gain of 5.4%.

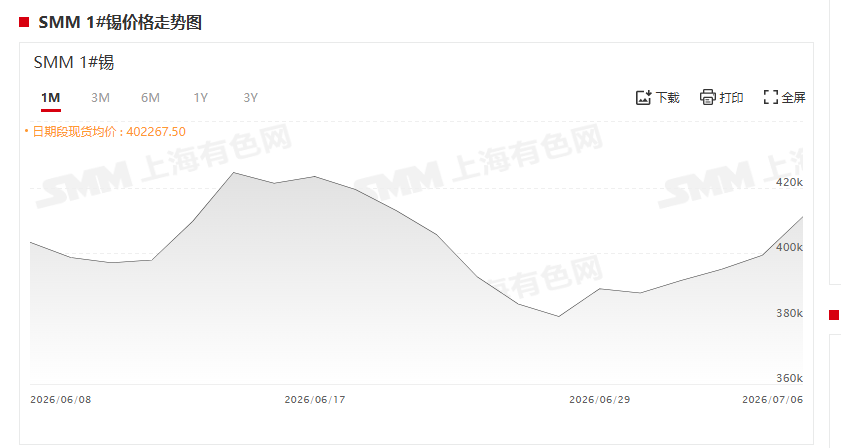

In the spot market, spot tin prices fell over 8% in June. Although prices rose consecutively in July, market sentiment remained cautious.

Regarding spot tin prices, the SMM #1 spot tin price recorded four consecutive days of gains. On July 6, it was quoted between 406,900 and 415,300 yuan per ton, with an average price of 411,100 yuan per ton, up 2.96% from the previous day. As tin prices rebounded, caution grew in the spot market, with only some essential procurement needs being met, resulting in low transaction activity. Looking at the monthly trend, the average SMM #1 spot tin price on June 30 was 387,800 yuan per ton. Compared to the average price of 425,000 yuan per ton on May 29, it fell by 37,200 yuan per ton over more than a month, a decline of 8.75%. When tin prices fell to around 380,000 yuan per ton, downstream enterprises showed a phased release of restocking demand.

On the fundamentals side, refined tin production increased slightly month-on-month in June, remaining generally stable.

In terms of production, refined tin output edged up in June. Raw material supply improved marginally, with an increase in imported tin ore from overseas. The pace of mine resumption in Myanmar was slow but ore continued to flow out, alleviating the domestic raw material shortage. An increase in imported ore arrivals at ports drove up smelting and processing fees, leading to a phased easing of the raw material tightness and creating conditions for smelters to raise operating rates. However, future output expansion faces constraints. The period from May to July is the traditional rainy season in Myanmar, which limits open-pit mining and ore transportation, leading to expectations of a month-on-month decline in short-term overseas ore imports. Currently, the supply side for refined tin is marginally loose, but downstream industries are entering the traditional consumption off-season. Both supply and demand are weak, making it difficult for output to increase significantly in the short term.

On the import side, tin ore imports in May increased both year-on-year and month-on-month. Imports from Myanmar surged 384.5% year-on-year. In May, China's tin ore imports totaled 16,800 tons (approximately 6,408 metal tons), up 7.07% month-on-month and 25.61% year-on-year, an increase of 1,221 metal tons compared to April (approximately 5,187 metal tons in April). Cumulative imports from January to May reached 85,900 tons, a cumulative year-on-year increase of 71.41%. In May, China's tin ingot imports were 1,838 tons, down 34.4% month-on-month and 11.46% year-on-year. Cumulative imports from January to April were 11,196 tons, a cumulative year-on-year increase of 17.75%. Import and export data for the tin industry chain from 2025 to May 2026 indicate that the global tin market's supply-demand pattern is undergoing significant structural adjustments. Overseas mine supply is accelerating its recovery, easing pressure on domestic raw material supply. Meanwhile, lower raw material costs have led to increased supply from downstream smelting, while weak overseas demand has hindered exports. On the raw material supply side, cumulative tin ore imports from January to May 2026 reached 85,998 tons, a substantial year-on-year increase of 71.41%. May's single-month imports were 16,831 tons, up 7.07% month-on-month and surging 25.61% year-on-year. This rebound was primarily driven by the recovery of Myanmar's mines. Tin ore imports from Myanmar in May reached 6,634 tons, a staggering 384.5% year-on-year increase, with cumulative imports from January to May up 203.49% year-on-year. In contrast, while imports from countries other than Myanmar maintained a cumulative positive growth of 34.72%, the single-month figure for May still fell 15.23% year-on-year, indicating a relatively slower recovery in non-Myanmar ore supply.

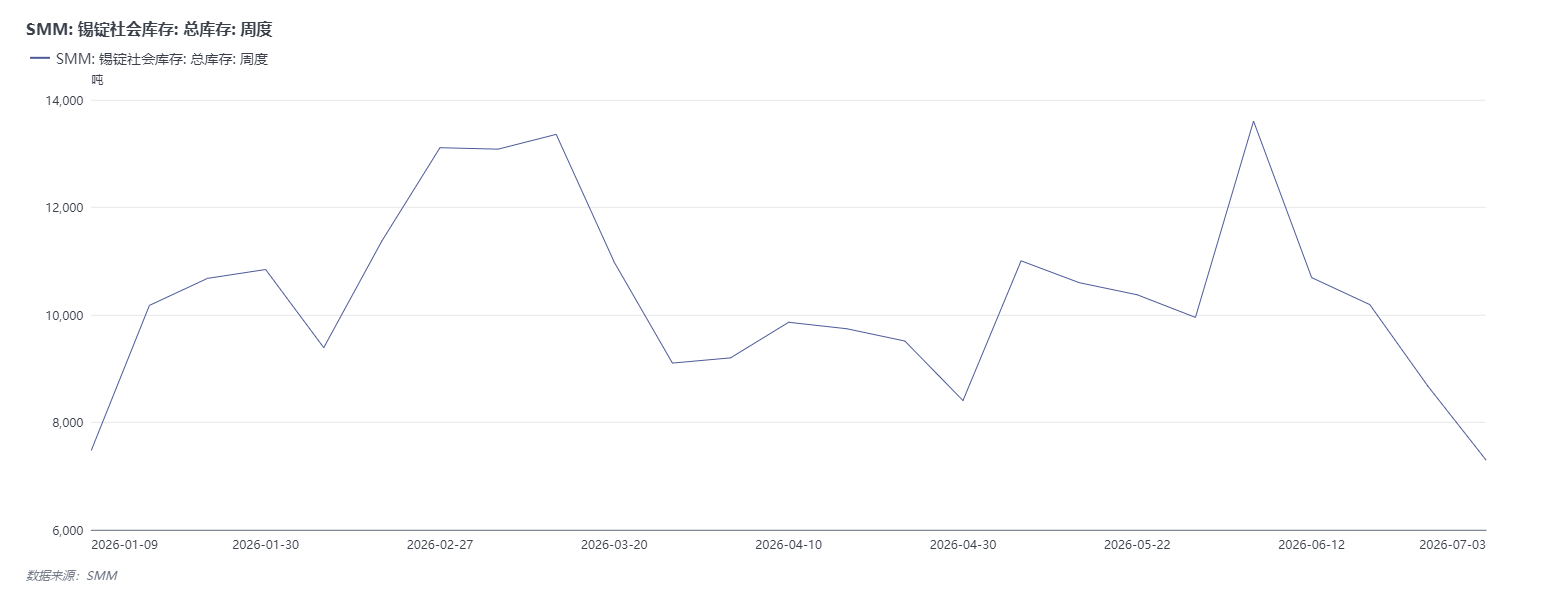

In terms of inventory, SMM's weekly social inventory of tin ingots across three locations has been destocking for four consecutive weeks.

Regarding domestic social inventory of tin ingots, according to SMM statistics, as of July 4, 2026, the total social inventory of tin ingots across three locations stood at 7,299 tons, a significant week-on-week decrease of 1,374 tons, or 15.84%, from 8,673 tons on June 26. Since the cyclical high of 13,604 tons in early June, domestic social inventory of tin ingots has been destocking for four consecutive weeks, with a cumulative destocking magnitude of approximately 46.4% over the past month. The destocking slope shows a pattern of being gentle initially and steep later. The current inventory level has fallen to a low point for the year, indicating a significant marginal improvement in the market's supply-demand balance. By region, inventory in Shanghai fell to 3,750 tons, decreasing by 996 tons in a single week, accounting for 72.5% of the total weekly destocking, making it the primary driver of this round. This reflects accelerated trade flows in the East China region and a substantial recovery in downstream purchasing intentions. Inventory in the Guangdong region also fell to 3,449 tons, a week-on-week decrease of 378 tons, accounting for 27.5% of the total destocking. This confirms that downstream rigid demand, represented by solder companies in South China, remains resilient, with restocking pace picking up. The logic behind the inventory drawdown is the restocking demand triggered by price corrections. The inhibitory effect of previous high tin prices on downstream procurement has gradually subsided as prices have recently returned to more rational levels, leading to the concentrated release of accumulated rigid orders and accelerating the digestion of visible inventory. Regarding LME tin inventory, it stood at 8,575 tons on June 30, down from 8,850 tons on May 29, showing a decline in June.

SMM Outlook

On the macro level, multiple domestic and international macro events in July will continue to disturb tin prices. Overseas, key focuses include the minutes of the Fed's June FOMC meeting, US CPI and PCE inflation data, and the Fed's FOMC meeting at the end of the month. Waller's statement that inflation risks are receding, coupled with the weaker-than-expected June non-farm payroll data, has led to a phased cooling of market rate hike bets. If subsequent inflation data rebounds and the Fed adopts a hawkish tone, a stronger dollar will weigh on tin prices. Conversely, continued easing expectations will provide valuation support for tin prices. Domestically, the central bank is increasing liquidity injections, ultra-long-term special government bonds are being steadily implemented, and stimulus policies related to high-end manufacturing technical upgrades and equipment renewal are gradually taking effect. These factors are positive for the medium-to-long-term consumption of tin downstream industries such as semiconductors, AI computing power, and new energy. However, the weak pattern in the electronics industry during the short-term off-season is unlikely to reverse quickly. The pace of releasing domestic policy dividends will directly determine the strength of downstream spot restocking. On the supply side, the overall tight supply pattern for tin ore remains unchanged, but marginal signals of increase are growing. Smelters maintain stable production, with no large-scale production cuts currently planned. On the demand side, as the traditional consumption off-season sets in, downstream solder companies are cautious in their procurement, only purchasing for essential needs. High prices significantly suppress purchasing intentions. On the inventory side, tin product inventories both domestically and internationally continue their destocking trend, providing support for tin prices. Overall, changes in macro expectations combined with the performance of the tech sector will influence the magnitude of tin price fluctuations. Tight ore supply and low overall inventory levels form a strong fundamental floor, providing a safety net for tin prices. However, the current weak off-season demand will continue to drag on the market, limiting the upside potential for tin prices. Looking ahead, it is crucial to closely track the Fed's policy direction and the prosperity of the semiconductor industry chain, while continuously monitoring the destocking pace both domestically and internationally. A new upward driving force for tin prices will only emerge when a substantial recovery in demand is observed.