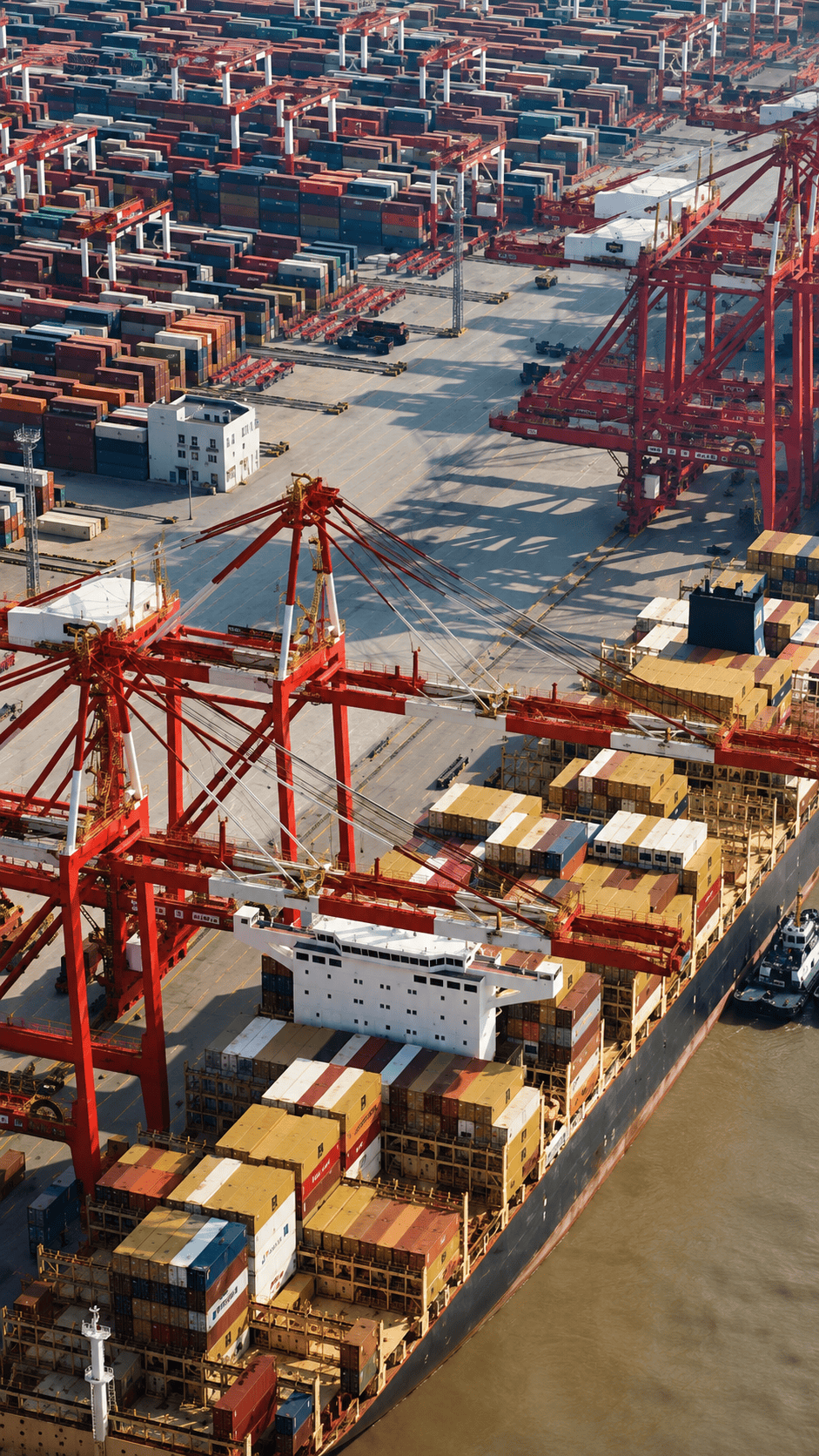

en.Wedoany.com Reported - The "Global Port Tracker" report, jointly released by the National Retail Federation (NRF) and maritime consultancy Hackett Associates, predicts that U.S. port imports in July will hit a historic high. The report attributes this growth primarily to retailers accelerating stockpiling ahead of the expiration of temporary tariffs and the anticipated introduction of new, higher tariffs.

The ports covered in the report include Los Angeles/Long Beach, Oakland, Tacoma, Seattle, Houston, New York/New Jersey, Hampton Roads, Charleston, Savannah, Miami, Jacksonville, and Port Everglades in Fort Lauderdale, Florida. The report notes that cargo import data is not directly correlated with retail sales or employment, as it counts the number of containers entering the U.S. rather than the value of goods, but import volumes can roughly reflect retailers' expectations.

Jonathan Gold, NRF's Vice President for Supply Chain and Customs Policy, stated that the early peak season this year is expected to last through July, as retailers and other importers prepare for potentially higher tariffs and other trade uncertainties that may begin in August. He emphasized that with the back-to-school sales season and winter holidays approaching, retailers are working to bring products into the U.S. and guard against new tariffs that could drive up prices. Despite ongoing economic headwinds, consumers continue to spend, but affordability remains a key factor.

For the most recent month with available data, May, U.S. imports at the ports covered by the report totaled 2.24 million TEU, up 10.1% month-over-month and 14.9% year-over-year. The report explains that the lower import figures for May 2024 are related to the timing of the White House's "Liberation Day."

The report released forecasts for June and subsequent months: June at 2.33 million TEU, up 18.7% year-over-year, bringing the total for the first half of 2026 to 12.77 million TEU, up 2% year-over-year; July at 2.47 million TEU, up 3.3% year-over-year, setting a new monthly record, surpassing the 2.4 million TEU in May 2022; August at 2.22 million TEU, down 4.5% year-over-year; September at 1.99 million TEU, down 5.7% year-over-year; October at 1.99 million TEU, down 3.8% year-over-year; and November at 1.92 million TEU, down 5.2% year-over-year.

The report states that imports from May to July are expected to be the highest of 2026, adding that the shipping peak season, which typically occurs around October, has shifted earlier in recent years due to port labor disputes and anticipated tariff increases. Ben Hackett, founder of Hackett Associates, analyzed in the report that multiple factors, including international trade pressures related to intermittent peace agreements in the Persian Gulf and the expiration of the temporary 10% Section 122 tariff on July 24, which could trigger a new round of higher tariffs, are key industry themes. He wrote that the sharp rise in import volumes, with strong growth in May potentially extending into July, largely reflects pre-stocking ahead of expected tariff increases starting July 25. The surprising resilience of the U.S. economy encourages consumers to continue spending, while an unstable ceasefire agreement with Iran has helped West Texas Intermediate crude oil prices fall nearly 40% from recent highs of nearly $120 per barrel, already beginning to lower fuel costs for consumers at the pump. Additionally, logistical issues surrounding uncertainty over passage through the Strait of Hormuz continue to drive changes in supply chain strategies. Carriers have succeeded in supporting higher freight rates by increasing capacity and strictly managing deployments, ensuring profitability—a significant shift from the widespread pessimism just a few months ago. Due to these developments, the report has raised its forecasts for June and July, as shippers navigate the uncertainty of the government's upcoming tariff policies.