en.Wedoany.com Reported - Policy decisions, rather than changes in mine supply, are becoming the core factor influencing the supply-demand balance of critical minerals markets. In the first week of July, two events occurred simultaneously: China expanded export controls on Japan, and the Democratic Republic of the Congo's cobalt export system stalled due to customs registration failures. These events affected critical mineral prices without any changes in mine output or demand, demonstrating that government decisions now carry as much weight as geological and operational developments in current supply chain assessments.

On June 29, China's Ministry of Commerce blacklisted four Japanese government defense research institutions and added 20 entities, including Mitsubishi Electric and Mitsubishi Heavy Industries, to its export control list. The restrictions cover tungsten, molybdenum, and finished magnet materials such as samarium-cobalt magnets and neodymium-iron-boron magnets. Unlike previous restrictions that only targeted raw oxides, this expansion extends controls to downstream high-value manufacturing inputs, meaning export restrictions now reach from upstream mining to processing and component supply, making downstream supply chains more vulnerable to policy changes.

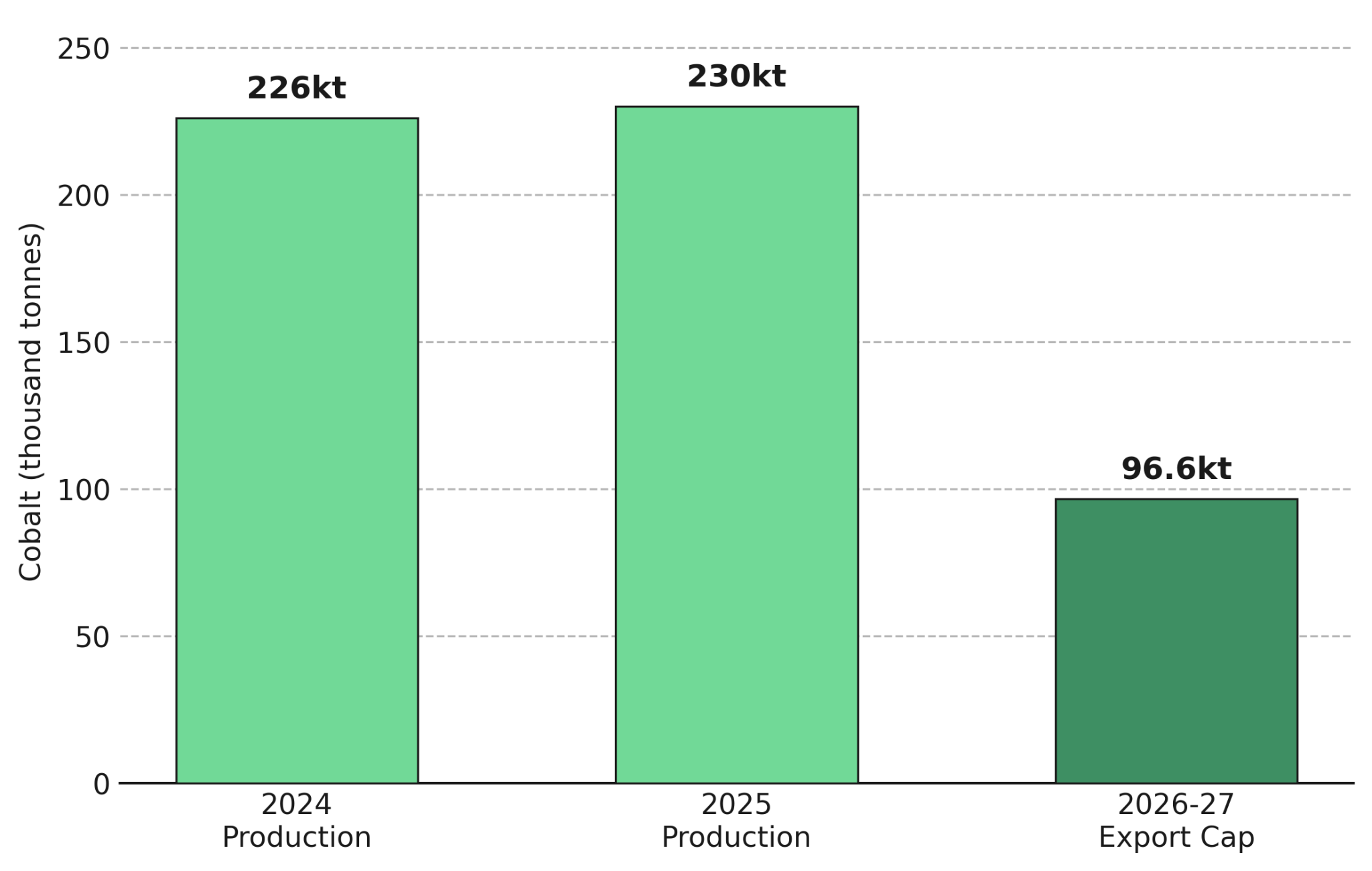

Meanwhile, the Democratic Republic of the Congo supplies approximately 70% of the world's mined cobalt. The country has set annual cobalt export caps of 96,600 tons for 2026 and 2027, less than half its 2024 production. Under quota rules, any quota not shipped by a fixed deadline is automatically forfeited to the national strategic reserve. Since July 1, registration failures on the country's customs platform have put approximately 20,000 tons of cobalt (worth about $1.1 billion) at risk of forfeiture, affecting producers including CMOC Group, Glencore, Eurasian Resources Group, and Huayou Cobalt. This incident shows that even with unchanged mine output and demand, administrative decisions within the export quota system can reduce available supply and influence cobalt prices.

A third policy decision that same week came from North America. On July 1, the United States refused to renew the United States-Mexico-Canada Agreement (USMCA) in its current form. The agreement, covering approximately $2.5 trillion in annual North American trade, was placed on a ten-year annual review cycle rather than being confirmed for a 16-year extension. The agreement remains in effect, but the annual review reduces the predictability of trade rules for cross-border critical mineral projects and battery supply chains, exposing critical mineral production among Canada, the United States, and Mexico to higher policy risk.

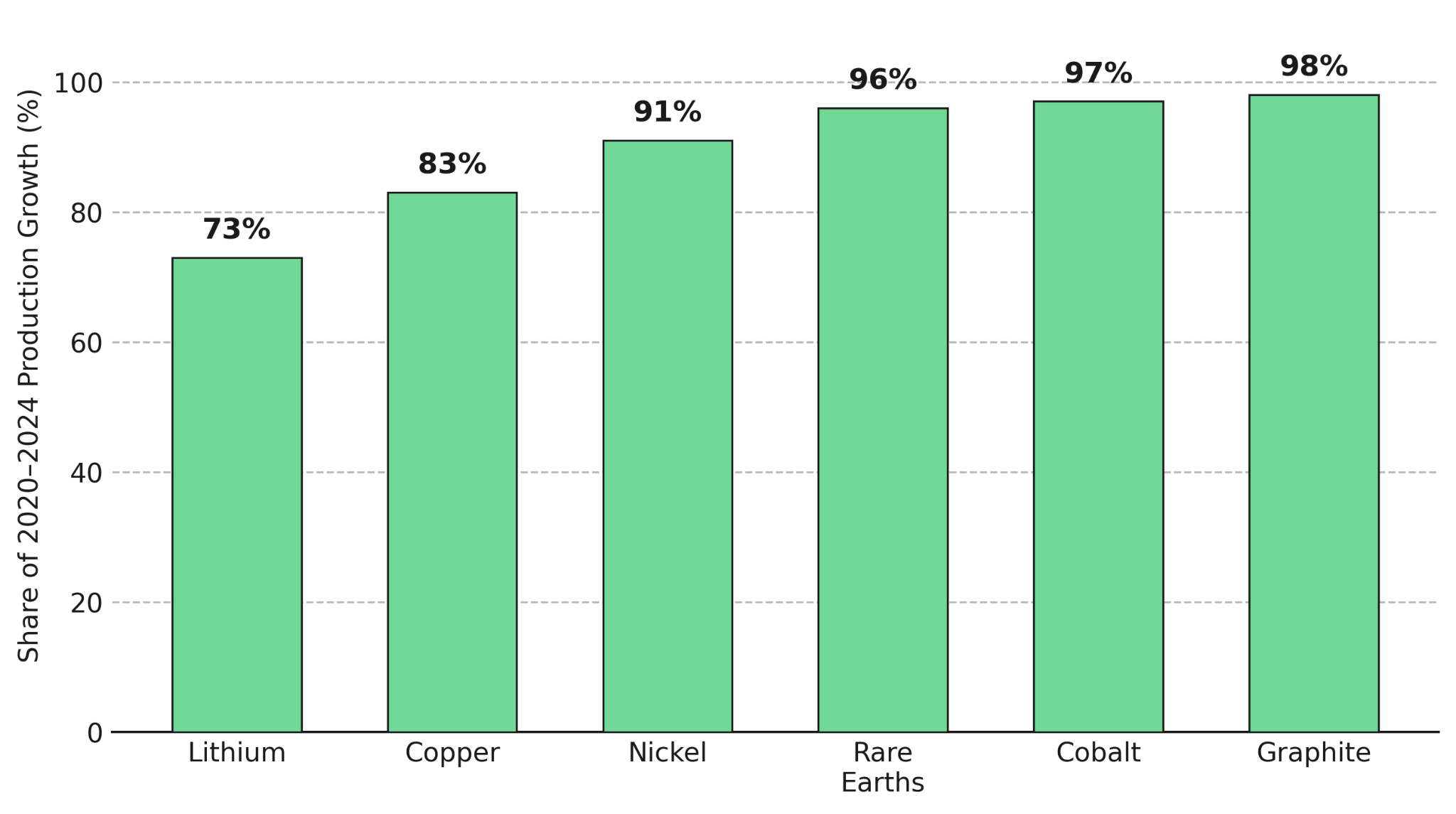

The Congolese customs failure and China's expanded export controls are not isolated events; they reflect an overall trend of minimal change in global smelting concentration over the past five years. According to data from the International Energy Agency (IEA), the average market share of the top three smelting countries for copper, lithium, nickel, cobalt, graphite, and rare earth elements rose from approximately 82% in 2020 to 86% in 2024. Smelting and processing capacity, rather than mine supply, remains the primary source of concentration risk in critical mineral supply chains. IEA baseline scenario projections show that the top three smelting shares will only decline modestly over the next decade, remaining close to 2020 levels.

Smelting concentration data indicates that individual policy actions persistently disrupt critical mineral supply chains because of the underlying vulnerability of those chains. Project financiers are now placing greater emphasis on exposure to policy decisions in single jurisdictions, rather than focusing solely on resource quality. Development finance institutions are prioritizing permitting, environmental compliance, and jurisdictional risk in their due diligence. The International Finance Corporation (IFC) has confirmed that a certain project's final feasibility study and environmental and social impact assessment meet its performance standards, accelerating the due diligence process for other lenders.

Three risk mitigation approaches are becoming increasingly important in critical mineral project financing: by-product production, recycling, and leveraging jurisdictional cost or carbon advantages. Energy Fuels' White Mesa Mill in Utah is the only fully licensed and operating conventional uranium processing facility in the United States, and the only facility capable of separating monazite into individual rare earth oxides. It processes up to 10,000 tons of monazite annually, producing up to 1,000 tons of neodymium-praseodymium oxide (NdPr) for permanent magnets used in electric vehicles and defense. Sovereign Metals' Kasiya project, based on a final feasibility study for rutile (titanium) and graphite production, shows a net present value of $2.2 billion at an 8% discount rate. Its newly confirmed monazite stream can be recovered through existing tailings circuits at near-zero incremental capital cost, and the project's incremental graphite cost is only $241 per ton, enabling a 50% operating margin even in lower-value battery graphite markets, while avoiding the permitting and infrastructure requirements of standalone projects.

Lifezone Metals' U.S. platinum group metals (PGM) recycling project recovers minerals from recycled feedstocks, with pilot-scale tests showing recovery rates of up to 99% for platinum and palladium, and up to 95% for rhodium. Canada Nickel's Crawford project in Ontario leverages the local low-carbon electricity grid to support operations. Ontario's low-cost, low-carbon energy grid, powered by nuclear and hydroelectricity, reduces the embedded carbon intensity of products and lowers compliance costs under the European Union's Carbon Border Adjustment Mechanism (CBAM).

The policy events of the first week of July affected critical mineral pricing without involving mine closures, resource downgrades, or demand shocks, reflecting that government policy decisions in a few exporting countries have become as important as geological or mine development changes. With smelting concentration largely unchanged over the past five years, the differences between projects increasingly lie in how they reduce exposure to concentrated supply chains and policy risks. Financing commitments and offtake agreements remain contingent on project milestones and final approvals, and execution capability has become as important as resource quality and jurisdictional exposure.