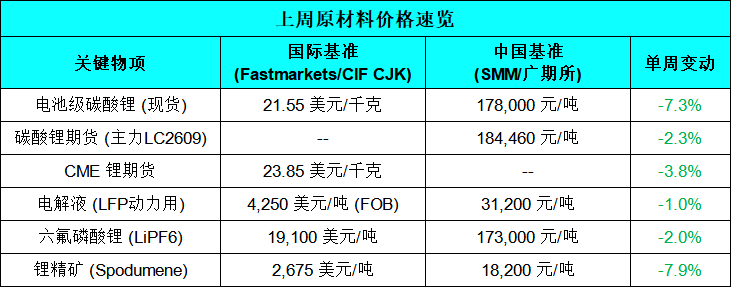

en.Wedoany.com Reported - The Asia-Pacific lithium battery industry chain has been under overall pressure recently. The SMM battery-grade lithium carbonate spot price dropped by 7.3% in a single week, while lithium concentrate quotations to China, Japan, and South Korea fell by 7.9% to US$2,675 per ton. The decline in concentrate outpaced that of lithium salts, indicating that the loosening pace at the raw material end is faster than downstream. Midstream electrolyte and lithium hexafluorophosphate prices stabilized slightly and pulled back, with industry chain profits shifting from the upstream mining end to the midstream material segment. Industry analysis suggests this market trend is mainly influenced by the concentrated release of supply-side expansion information. However, from the demand side, global energy storage cell shipments doubled year-on-year in the first quarter of this year, indicating that fundamental support still exists.

The Minerals Marketing Corporation of Zimbabwe (MMCZ) disclosed on May 18 that the country's lithium sales volume reached 240,826 tons in the first quarter of 2026, with sales revenue of US$178.64 million. Compared to 224,610 tons and US$84.19 million in the same period of 2025, export volume increased slightly, while export value saw a significant year-on-year jump. This is the first public release of quarterly data since the country implemented an emergency export ban on lithium concentrate on February 25. Zimbabwe is currently the world's fourth-largest lithium producer and China's second-largest source of lithium concentrate imports, exporting approximately 1.2 million tons of lithium concentrate to China in 2025. Prior to this data release, there was significant market divergence regarding the country's actual export volume.

Australian mining company Mineral Resources announced on May 19 the restart of the Bald Hill lithium mine in Western Australia. The mine entered care and maintenance in November 2024 due to low lithium prices. MinRes disclosed that Bald Hill has an annual production capacity of approximately 165,000 tons of 5.1% spodumene concentrate, equivalent to about 140,000 tons of SC6 lithium concentrate. The project plans to resume site activities by the end of May, start mining and crushing in June, produce the first batch of lithium concentrate in July, and achieve the first shipment in the first quarter of the 2027 fiscal year. This restart is one of the representative projects among Australian hard-rock lithium mines confirming a resumption earlier after price recovery, further strengthening market expectations for a recovery in mine-end supply.

On May 19, InfoLink Consulting released global energy storage cell shipment data for the first quarter of 2026. The report shows that global energy storage cell shipments reached 205.52 GWh in Q1, a year-on-year increase of 98.70% and a quarter-on-quarter increase of 1.62%. Among these, large-scale storage cell shipments were 178.27 GWh, up 84.54% year-on-year; small-scale storage cell shipments were 27.25 GWh, up 298.98% year-on-year. In terms of overall ranking, the global Top 10 energy storage cell manufacturers are all Chinese companies, with the top five being CATL, Hithium Energy Storage, BYD Energy Storage, EVE Energy, and CALB.

Chinese lithium salt capacity expansion projects have been intensively launched recently. On May 19, Xinyu, Jiangxi Province, announced the official launch of an 8,000-ton lithium carbonate expansion project; on the same day, Dazhong Mining disclosed plans to expand its lithium carbonate project capacity to 40,000 tons. This marks the first concentrated signal of capacity expansion among Chinese lithium salt enterprises since 2026. In the previous year, under a low price of 58,000 yuan per ton, most upstream lithium mines in China were in a state of production cuts or maintenance. According to estimates by relevant institutions, if commissioned as scheduled, this will add at least 40,000 to 50,000 tons of lithium carbonate equivalent supply in the second half of 2026.

On May 21, Chinese-funded enterprise Yahua Group disclosed that the export procedures for lithium concentrate from its Kamativi Mine in Zimbabwe have been completed, and new batches of lithium ore are being shipped back to China in stages. The company also stated that the Kamativi Mine maintained normal production during the ban period, lithium ore output was unaffected, and current lithium concentrate inventory can guarantee domestic production needs. Since Zimbabwe issued the export ban in February, this is one of the first Chinese-funded enterprise projects to complete approval and substantively ship material, echoing the binding model of local deep-processing production lines established by Huayou Cobalt and Sinomine Resource Group during the same period.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com