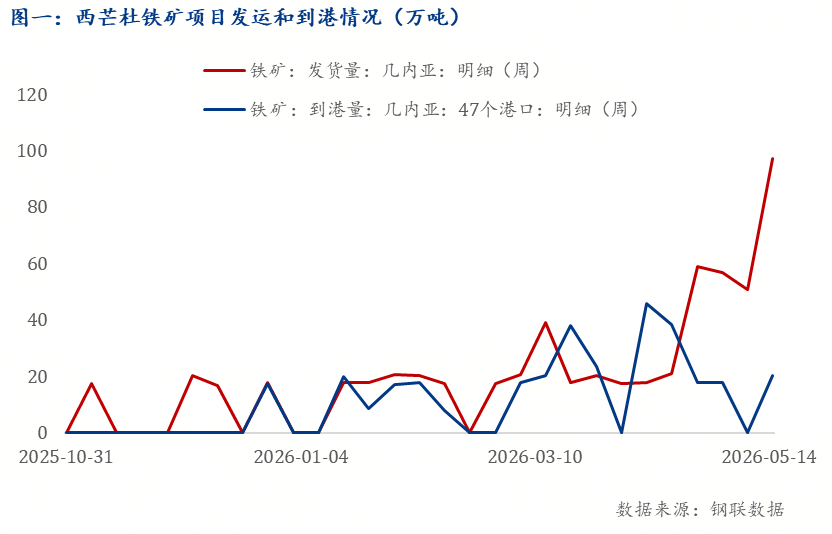

en.Wedoany.com Reported - Core data from Shanghai Ganglian (Mysteel) shows that since the first shipment of the Simandou iron ore project on November 7, 2025, shipment volumes have been ramping up rapidly. The first week's shipment was 174,000 tonnes, with subsequent volumes fluctuating mostly between 200,000 and 400,000 tonnes. As of mid-May 2026, cumulative shipments reached approximately 6 million tonnes, with a single-week peak of 974,000 tonnes in mid-May, setting a new record. In terms of arrivals, the first shipment of iron ore arrived in the week of December 26, 2025, also at 174,000 tonnes, with cumulative arrivals reaching approximately 3.2 million tonnes as of May 15. Looking ahead to the full year, Shanghai Ganglian expects total shipments in 2026 to potentially exceed 20 million tonnes.

Simandou products are relatively close to Carajas Fines (IOCJ) in iron grade, both in the 65% to 66% range. However, there are significant differences in other indicators: Simandou has a silica content below 2%, better than IOCJ's approximately 2.7%; its alumina content is around 2.7%, higher than IOCJ's roughly 1.4%. The higher alumina content is a key constraint in replacing IOCJ, as high alumina increases blast furnace slag viscosity and affects desulfurization efficiency, requiring steel mills to adjust their ore blending plans. Additionally, Simandou products contain a small amount of lump ore requiring screening, while IOCJ is a uniform fine ore ready for direct use. However, Simandou products offer environmental advantages with low carbon, low phosphorus, and low sulfur content, making them suitable for direct reduction pelletizing processes.

Market research indicates a divergence in steel mills' acceptance of Simandou products. Mills in the north and some in the east are cautiously optimistic, planning small-scale trials to compare Simandou and IOCJ performance in sinter strength and blast furnace utilization rates. Southern mills are more concerned about the higher alumina content, believing their slag systems are optimized for low-alumina environments, making the technical adaptation cost of switching to Simandou products relatively high. Traders show greater enthusiasm, with some having already purchased or planning to purchase Simandou products, generally optimistic about them becoming a mainstream variety, viewing the low silica characteristic as a differentiated advantage and the high alumina issue as solvable through proper ore blending.

As of mid-May 2026, actual transactions of Simandou high-grade fines concentrate have been concentrated among a few steel mills such as Baowu Group, Rizhao Steel, and Weiqiao Group, with procurement models including long-term agreements and spot purchases. Most steel mills remain in trial or wait-and-see phases, with no large-scale demand formed yet.

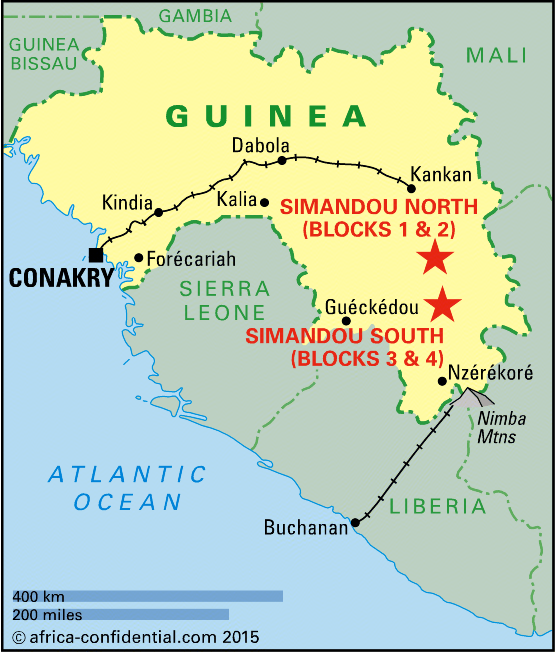

From the perspective of infrastructure progress, the three major components of the Simandou project—mine, railway, and port—are advancing simultaneously. On the mining front, Blocks 1 and 2 are already operational, while development of Blocks 3 and 4 is progressing orderly, expected to contribute incremental output from the second half of 2026. For transportation, the approximately 650-kilometer Dapilon-Santou Railway began operations at the end of 2025, with a designed annual capacity of 40 million tonnes. Recently, the 70-kilometer railway branch line connecting the SimFer mine to the Trans-Guinean Railway also achieved mechanical completion. On the port side, the first phase of the Morebaya Port, with an annual throughput capacity of 40 million tonnes, has been put into use, equipped with modern ship-loading equipment capable of loading 10,000 to 15,000 tonnes per hour per vessel.

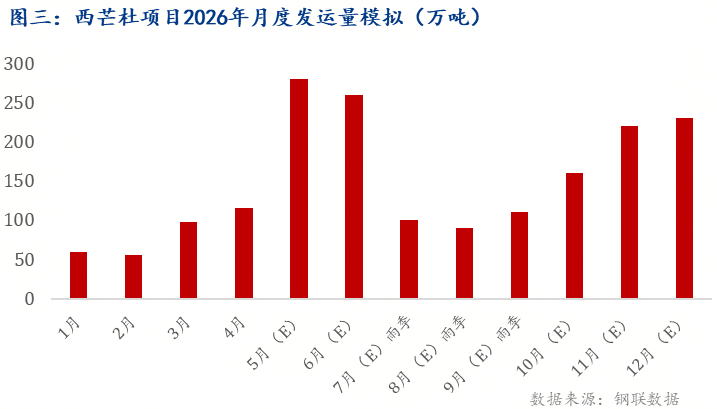

Thanks to the coordinated efforts of infrastructure, the pace of Simandou shipments is steadily accelerating. Looking ahead to the second half of the year, with the end of the rainy season from July to September, the shipment pace is expected to further quicken. Shanghai Ganglian comprehensively judges that total shipments in 2026 will exceed 20 million tonnes.

Regarding overall ore prices, although the ramp-up of Simandou intensifies the loose supply-demand balance for iron ore, Shanghai Ganglian data shows that global iron ore production in 2025 was approximately 2.613 billion tonnes. Simandou's 20 million tonnes accounts for a relatively small share, insufficient to trigger a significant decline in overall ore prices, which are expected to move moderately lower. At the variety level, Simandou products have a similar iron grade to IOCJ. If stable volumes are achieved and steel mills accelerate blending adjustments, it will squeeze IOCJ market demand, putting downward pressure on IOCJ premiums. As steel mills' technical adaptation capabilities improve, premiums for high-grade ore may narrow significantly, potentially encouraging mills to adopt more "high-grade + low-grade" blending models, indirectly boosting demand for low-grade ore and providing some support for low-grade ore prices.

Overall, the impact of the Simandou project on ore prices shows structural differentiation: overall ore prices will move moderately lower, high-grade ore premiums face pressure, and low-grade ore benefits relatively but with limited upside.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com