en.Wedoany.com Reported - U.S. copper tariff policies are becoming a core driver of regional copper pricing. In a market already facing supply shortages, the expansion of trade barriers has significantly altered the economics of copper products and created a two-tier market structure.

Since the initial imposition of Section 232 tariffs in 2025, the U.S. has expanded the policy scope: imposing tariffs on the full dutiable value of imported goods effective April 6, 2026, and lowering the domestic content threshold for preferential treatment from 95% to 85% on June 8. This policy has widened regional price spreads by restricting trade flows. J.P. Morgan Global Research and Goldman Sachs Research indicate that the upcoming refined copper tariff decision is a key near-term catalyst for copper prices. Imposing tariffs on refined copper could increase the value of domestic and allied supply; conversely, delaying the June 30 decision could reduce stockpiling demand and pressure copper prices.

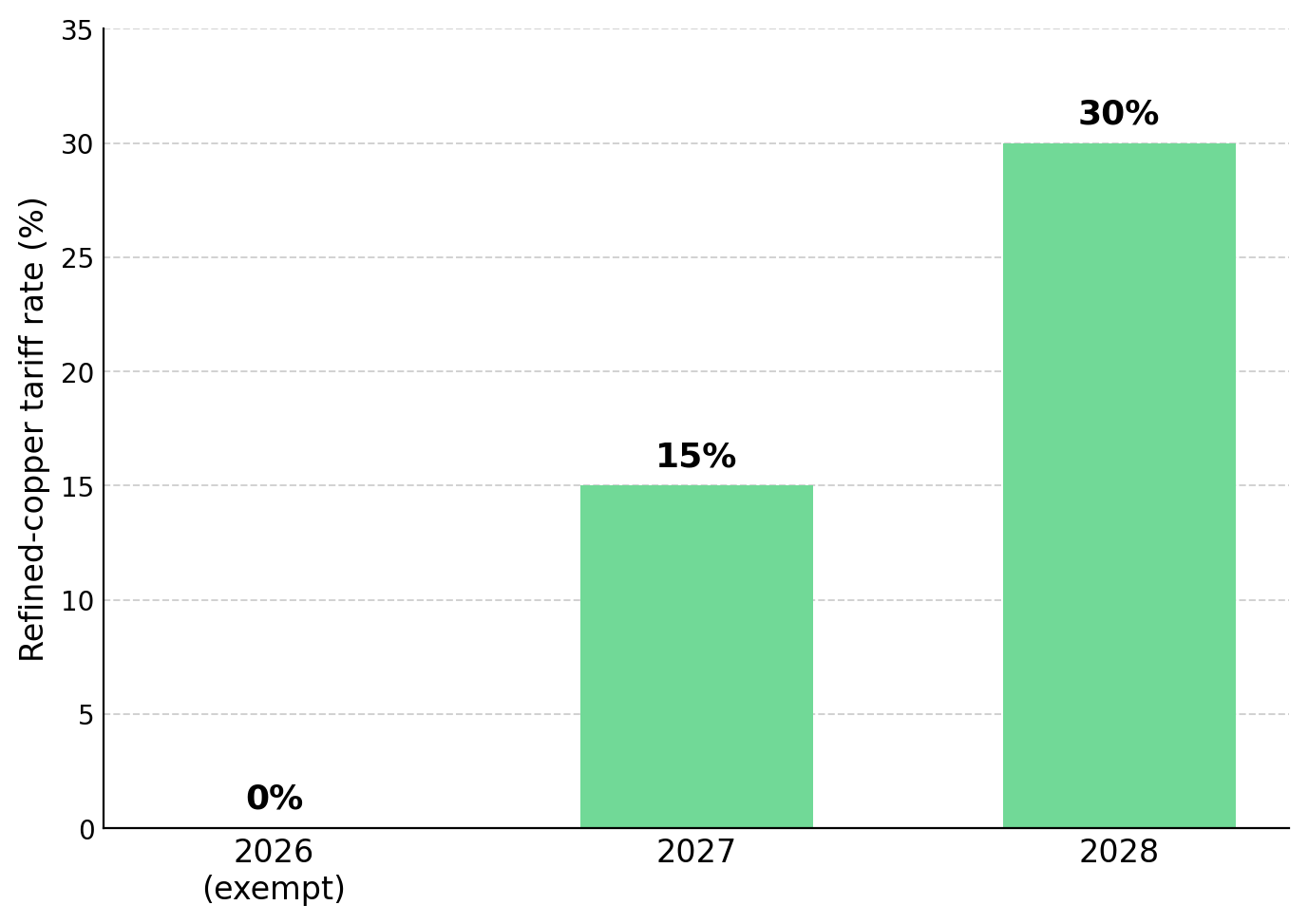

Currently, a 50% tariff applies to semi-finished products and copper-intensive derivatives, but refined copper cathodes remain exempt. This exemption, coupled with the proposed 15% tariff on refined copper in 2027 rising to 30% in 2028, encourages importers to ship refined metal into the U.S. ahead of future tariff implementation. The result is a significant flow of copper to the U.S. to capture tariff-related regional price spreads.

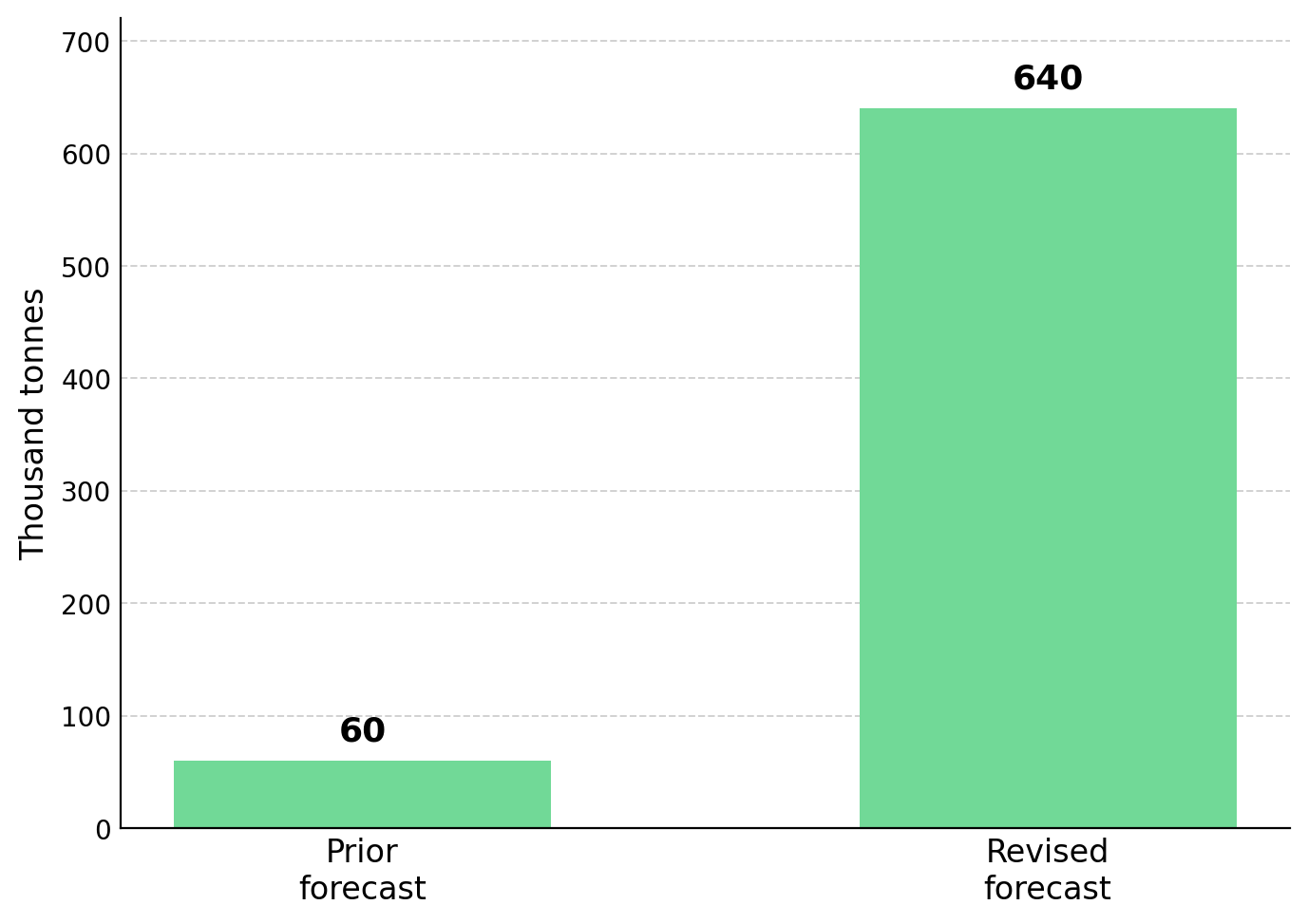

Importers shipped approximately 500,000 tons of copper into the U.S. within a month, compared to a normal monthly import volume of about 70,000 tons, pushing up U.S. copper premiums while tightening London inventories and driving Shanghai inventories to yearly lows. Goldman Sachs Research has revised its forecast for the copper shortfall outside the U.S. from approximately 60,000 tons to about 640,000 tons and lowered its 2026 global mine supply estimate by roughly 350,000 tons following disruptions at Grasberg in Indonesia and Kamoa-Kakula in the Democratic Republic of Congo.

The copper shortfall outside the U.S. reflects both trade policy impacts and limited concentrate supply. Treatment and refining charges (TC/RC), key indicators of concentrate availability, have fallen to near zero in some benchmark agreements for 2026. This indicates that concentrate supply remains tight regardless of tariff policies, supporting copper prices even without trade-related stockpiling.

U.S. tariff policies have increased the value of copper assets in allied jurisdictions by improving their access to preferential markets. Faster permitting processes, existing infrastructure, and political stability can shorten development timelines and lower discount rates, thereby increasing the relative value of assets in these regions. Canada is a major beneficiary. In Quebec, Abitibi Metals holds the B26 polymetallic deposit, with indicated and inferred resources of 25.3 million tons at a grade exceeding 2.1% copper equivalent. A preliminary economic assessment planned for completion in the first quarter of 2027 may enhance confidence in some inferred resources. SOQUEM, a subsidiary of Investissement Québec, holds a 20% stake in the project, while Eldorado's acquisition of Foran Mining for approximately C$3.8 billion highlights market demand for large-scale Canadian copper assets.

Existing infrastructure lowers the capital threshold for brownfield projects. Selkirk Copper offers an investment opportunity in the Minto project in Yukon. Minto is a former producing mine with indicated resources of 12.6 million tons at a copper grade of 1.20% and inferred resources of 23.7 million tons at a copper grade of 1.05%. Company President and CEO M. Colin Joudrie noted that over US$330 million has been invested in surface infrastructure, processing plants, roads, and underground works, so the project does not require significant capital for new power lines, roads, or surface facilities. Additionally, Indigenous control may support community coordination during project redevelopment.

If the June 30 ruling extends tariffs to refined copper, developers producing cathodes in allied jurisdictions will be most directly affected by the policy. Oxide ores can produce refined copper cathodes through heap leaching and electrowinning, with capital costs typically lower than sulfide projects requiring concentrators. Therefore, oxide projects planning to produce cathodes may benefit more from refined copper tariffs than projects producing concentrates. Marimaca Copper's oxide deposit in Chile has proven and probable reserves of 179 million tons at a copper grade of 0.42%, supporting its planned operation to produce 50,000 tons of cathode copper annually, which the company states is permitted and self-funding. CEO Hayden Locke stated that through the Pampa Medina oxide deposit, they see a very realistic near-term opportunity to expand cathode production from 50,000 to 75,000 tons per year. However, Pampa Medina remains an exploration target rather than a defined resource.

Fitzroy Minerals is exploring a copper oxide project in Chile that could support future cathode production. Buen Retiro has yielded shallow oxide intercepts, including a 78-meter section grading 1.70% copper. A heap leaching pre-feasibility study and a partnership with Pucobre support a maiden mineral resource estimate expected to be completed in the fourth quarter of 2026. CEO Merlin Marr-Johnson explained that the operation provides them with potential near-term non-operational cash flow and very low capital intensity. However, the potential of a larger iron oxide copper-gold (IOCG) system has yet to be confirmed.

Uncertainty surrounding the June 30 tariff decision favors companies funded through near-term milestones while increasing risk for projects requiring future equity financing. Abitibi Metals secured financing through key development milestones without issuing warrants. The company completed a C$31 million financing with no warrants, funding over 80,000 meters of drilling, a planned preliminary economic assessment, and feasibility work. CEO and Founder Jonathon Deluce stated that this funding provides them with ample capital to advance the project without issuing any warrants, avoiding shareholder dilution.

Cobra Resources offers an earlier-stage copper exploration opportunity. The company has obtained near-surface copper intercepts at the Blue Rose copper project in South Australia but has not yet defined resources or reserves. A fully funded diamond drilling program is testing deeper source zones. Managing Director Rupert Verco stated that successful drilling could support a low-cost, low-capital-expenditure heap leach startup approach combined with a flotation circuit for processing primary sulfide ore, but the project's value ultimately depends on drilling success and future financing.

The June 30 refined copper ruling will test whether trade policies can continue to reshape regional copper markets. With an estimated copper shortfall of 640,000 tons outside the U.S. and concentrate supply remaining tight, policy decisions are becoming an increasingly important driver of copper prices alongside traditional supply and demand fundamentals.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com