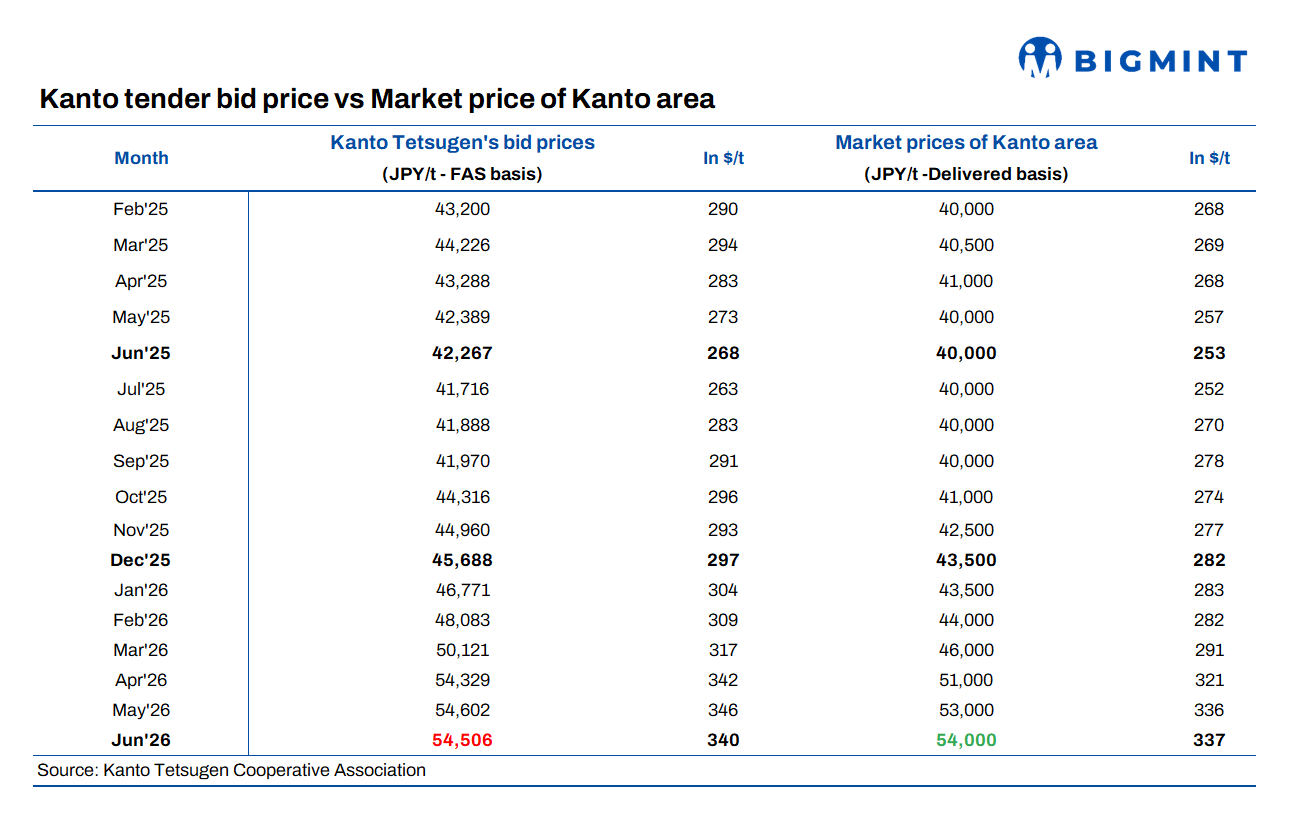

en.Wedoany.com Reported - Japan's June 2026 Kanto H2 export scrap tender price saw its first decline after ten consecutive months of increases, falling by 96 yen/ton ($1/ton) from the previous month to 54,506 yen/ton ($340/ton) FAS, covering 20,000 tons of cargo. The decline was minimal in yen terms, but more pronounced in dollar terms, with the tender value dropping about $6/ton from the May level of approximately $346/ton.

The latest tender price translates to approximately $347-348/ton FOB Japan, below $400/ton CFR Chittagong, with shipment scheduled before July 31, 2026. The decline was primarily driven by the yen's depreciation against the dollar, with the exchange rate weakening from about 157.1 yen/dollar during the May tender to 160.4 yen/dollar in June. While the yen-denominated price remained largely stable, the dollar-equivalent value decreased.

The cargo was awarded to a Japanese trading company and will be shipped to a steel mill in Chittagong, Bangladesh, marking the country's return to the Kanto market after a two-month absence. The tender received 14 bids totaling 120,400 tons, against a supply volume of 20,000 tons.

In contrast to weak exports, Japan's domestic scrap prices continue to rise. Supported by stable domestic demand and tight supply, domestic Kanto H2 scrap prices rose by about 1,000 yen/ton ($6/ton) month-on-month to approximately 54,000 yen/ton ($337/ton). Market participants noted that domestic fundamentals remain largely unchanged, and the weaker yen helps exporters maintain competitiveness in overseas markets. A Japanese trader said the decline in the dollar-denominated tender result was mainly due to currency fluctuations, not deteriorating scrap demand.

Despite Bangladesh's return to the Kanto market, sentiment for imported scrap purchases remains subdued ahead of the government's submission of the FY2027 budget on June 11. Market participants fear that higher electricity surcharges and other industrial taxes could further increase steelmaking costs amid sustained margin pressure.

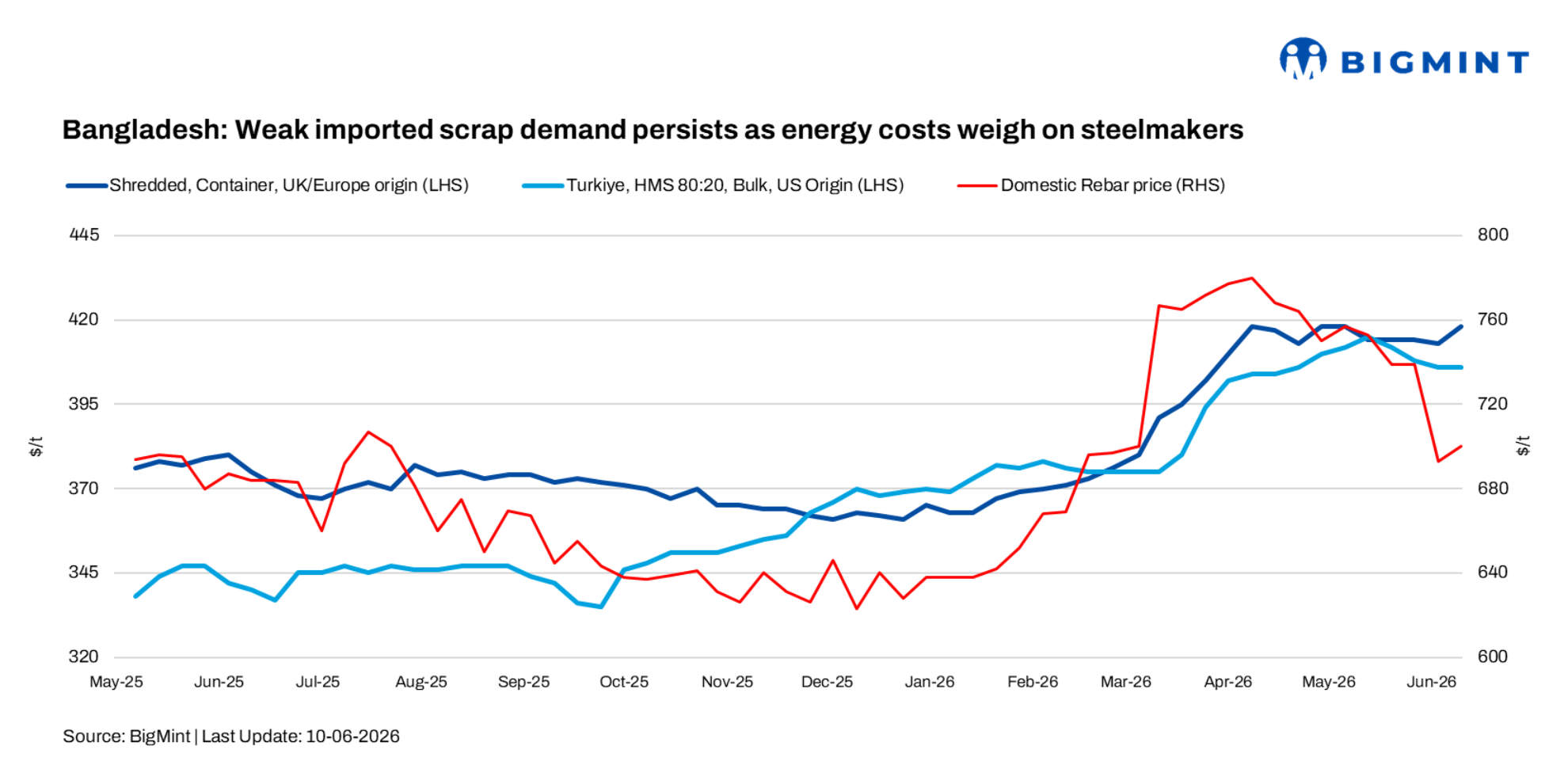

According to BigMint's weekly assessment, CFR Chittagong offers for European-origin containerized HMS (80:20) stood at $382/ton, down $2/ton week-on-week; European-origin containerized shredded scrap at $418/ton, up $5/ton week-on-week; Japanese-origin bulk H2 at $403/ton, down $12/ton week-on-week; and US-origin bulk HMS (80:20) at $410/ton, down $2/ton week-on-week.

Indicative offers remain inconsistent. Sources reported Philippine-origin galvanized scrap at $345-350/ton CFR Chittagong, and UK-origin HMS (80:20) at around $360/ton CFR Chittagong. Shredded scrap offers from Australia and the UK were reported at $420-430/ton CFR Chittagong, with bids for Australian-origin shredded scrap heard near $410/ton CFR Chittagong—persistent bid-ask spreads and cautious buying sentiment dominate the market.

Weak construction activity, sluggish real estate investment, and tight liquidity continue to constrain steel consumption, keeping buyers cautious. Industry observers believe that measures aimed at boosting consumer purchasing power, lowering financing costs, and supporting domestic manufacturing could help revive demand and improve sentiment in the steel sector.

Bangladesh's domestic scrap prices rose to 55,000-56,000 taka/ton ($448-456/ton), up from about 50,000 taka/ton ($407/ton) a week earlier. Despite the recent softening in the international scrap market, the sharp rise in local prices has reinforced steel mills' preference for domestic procurement. Market participants noted that buyers remain focused on maintaining liquidity and limiting exposure to policy uncertainty ahead of the FY2027 budget announcement.

A Dhaka mill source said the proposed 20-25% increase in electricity-related charges could significantly impact production costs. Amid high borrowing costs, rising energy prices, and currency depreciation, many steel mills continue to face margin pressure amid weak steel demand. Another Chittagong mill source noted that recent electricity tariff hikes have already increased production costs by about 2,000-4,000 taka/ton ($16-33/ton). Any further increases, coupled with rising natural gas prices and dollar-linked import costs, are expected to further drag on profitability.

Due to easier availability and faster delivery, local scrap remains the preferred choice for most Bangladeshi steel mills. Weak construction activity and slow steel demand keep buyers cautious, with most mills purchasing only on a need basis. Unless imported scrap prices become more competitive or domestic supply tightens, import activity is likely to remain limited in the near term.

BigMint expects Bangladesh's imported scrap market to remain under pressure as steel mills continue to prioritize liquidity management and closely monitor developments related to the FY2027 budget. Against the backdrop of weak steel consumption, high borrowing costs, and rising energy expenses, demand is likely to remain largely based on actual needs. While the weaker yen enhances the competitiveness of Japanese scrap, import activity is expected to remain restrained unless steel demand improves significantly or production costs and policy measures become clearer.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com