en.Wedoany.com Reported - Millennial Potash's Gabon potash project has entered the development phase, with company Chairman Farhad Abasov stating that the project is one of the world's largest undeveloped potash resources. The project is advancing feasibility studies, environmental and social impact assessments, while simultaneously securing construction financing. For investors, the project sits at the intersection of global fertilizer supply security, geographic diversification, and the company's near-term drive to close deals or commence production.

The Gabon project covers approximately 1,500 square kilometers, with drilling to date having identified approximately 6 billion tons of resources in the measured, indicated, and inferred categories. Management notes that these drillings cover only about 4% of the total licensed area, indicating potential for further resource expansion. The company has completed a preliminary economic assessment, which shows its cost structure ranks among the lowest in the global potash industry. The resource scale, combined with the project's geographic proximity to demand centers in Brazil and Africa, forms the basis of the investment case. The project is classified as solution mining, with lower capital intensity compared to other large underground mining projects in the region.

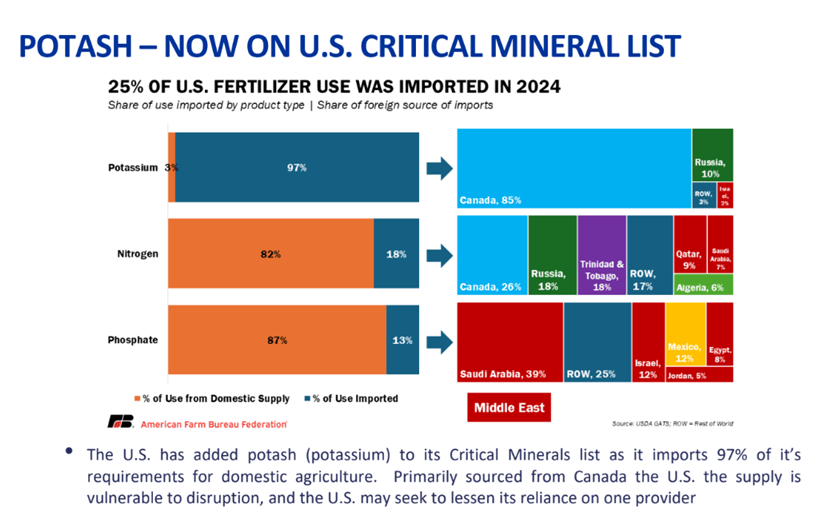

A core feature of the Gabon project is the support from the US International Development Finance Corporation (DFC). The DFC began due diligence in early 2024 and signed a formal support agreement in June 2025, including a $3 million feasibility study grant (disbursed in matching tranches, with the company having received the initial 10%), and a long-term pathway to provide debt financing for construction, contingent upon completion of the feasibility study, environmental and social impact studies, and obtaining a mining license. Abasov stated that the involvement of the US DFC de-risks the project politically and financially, and noted support from the US State Department and the US Embassy in Gabon. The company is also separately seeking support from the Canadian government. Management attributes the US government's interest to potash being included on the US critical minerals list and the ongoing US reliance on imported potash, including from Russia.

The global potash market is highly concentrated, with Russia, Belarus, and Canada estimated to account for 70% of supply, and including Jordan and Israel, approximately 80%. Management describes this concentration as a source of pricing discipline: low-cost producers such as Nutrien (Canada) and EuroChem (Russia) have estimated all-in costs of around $120 per ton FOB, with current prices ranging between $350 and $400 per ton. Regional prices vary, with Brazil trading at approximately $400-405 per ton, and African prices reportedly above $400 per ton. Annual potash consumption in Africa is approximately 2 million tons, a relatively small but underserved market compared to China's 17 million tons (of which 10 million tons are imported). Management positions the Gabon project to prioritize serving African agriculture, supplemented by sales to Brazil, the US Atlantic coast, and growing interest from Asian buyers.

The company's approach to offtake agreements differs from traditional pure sales structures. Management states that the goal is to secure commitments for approximately 20-25% of future production, but only from counterparties willing to provide financial support (direct equity investment or prepayment arrangements) prior to construction, rather than simple purchase agreements. Offtake terms under discussion are typically for 3 to 5 years, after which output would be sold on the spot market. Regarding overall project financing, management targets a capital structure leaning towards debt: approximately 60-65% debt financing plus royalty arrangements, with minimal equity dilution. Equity discussions are currently focused on US investors, in addition to the DFC grant and anticipated debt commitments, with African fertilizer industry conglomerates also listed as potential partners.

Management's published timeline is: completion of the feasibility study by end of 2026 or early 2027, finalizing financing and commencing construction by end of 2027, followed by an 18 to 24-month construction period. The project uses solution mining, which involves injecting water underground to dissolve potash, then pumping the brine to the surface for evaporation and separation. Management states this method has lower capital intensity than underground mining and a limited surface footprint. The same management team previously used solution mining on a Saskatchewan project (later sold to Germany's K+S AG, with annual production capacity exceeding 2 million tons) and an Ethiopian project (later acquired by Israel's ICL).

The project's economics are linked to surrounding infrastructure. An existing transshipment port (developed by a private London-based group) can be used to support initial production. The company is working with a partner group to advance a proposed deep-water port, which would be built and operated with external funding in exchange for handling fees. Management states this would allow capacity to expand from an initial approximately 800,000 tons per year to 4-5 million tons per year. A natural gas pipeline has recently been extended to the coast to support a power plant near the project, which management expects to be expanded as part of feasibility planning.

Management is pursuing two parallel paths: full project financing through debt, grants, and equity, and potential mergers, acquisitions, joint ventures, or strategic partnerships. Abasov noted that in the previous sale of a potash project to ICL, the acquirer was already a 17% shareholder but paid a 50% premium to acquire the remaining shares, an outcome he attributes in part to the International Finance Corporation adding credibility as a financing partner. Singapore-based family office Quaternary Group (with mining and agricultural backgrounds) holds a significant minority stake in Millennial Potash, and management states it participates with a similar dual-track approach. Management points out that a sale to a Chinese buyer would likely preclude continued DFC involvement, while a Western acquirer or partner would retain access to the existing DFC support package.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com