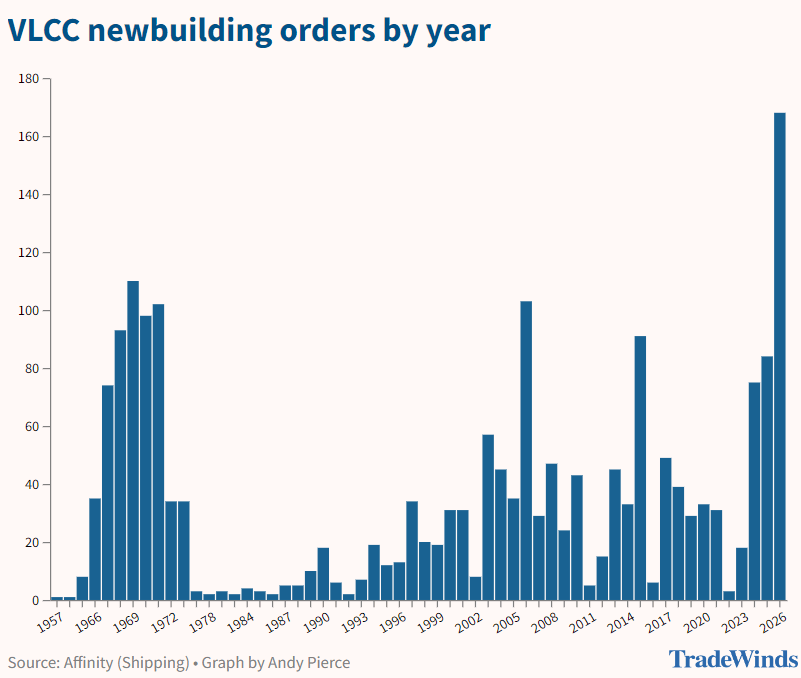

en.Wedoany.com Reported - In the first half of 2026, the order volume for very large crude carrier (VLCC) newbuildings hit a historic high, with total contracts not only surpassing the peak of the previous super cycle but also breaking all records since the late 1960s.

Data from multiple shipbrokers and shipping analytics firms show that from January to June this year, global VLCC newbuilding orders experienced exponential growth. According to global maritime data provider Veson Nautical, order volumes in the first half surged nearly tenfold compared to the same period last year. Analyst Rebecca Galanopoulos from the firm revealed that 197 VLCCs were ordered in the first half of 2026, compared to just 24 in the same period last year.

Records from shipbroker Affinity also confirm this growth trend—168 new VLCCs have been contracted so far this year, far exceeding the previous historical high of 110 set in 1969. The company's historical data shows that only two years, 1971 (102 vessels) and 2006 (103 vessels), had previously exceeded 100 contracts, while 2026 surpassed this level in just half a year.

Chinese shipbuilders have performed prominently in this order boom. Broker data shows that Hengli Heavy Industry dominates with 86 orders, followed by Dalian Shipbuilding Industry Group with 18. South Korea's Hanwha Ocean ranks third with 16 orders. BIMCO shipping analysis manager Filipe Gouveia noted that 2026 has become the highest year on record for crude oil tanker newbuilding contracts. Data from chartering platform Signal Ocean shows that VLCC orders alone accounted for 78% of the global tanker orderbook in the first half of the year.

Analysts believe this VLCC order wave is driven by multiple factors. First is fleet renewal pressure. The global VLCC fleet faces significant aging issues, with the average age of VLCCs continuously rising since 2011 to reach 14 years. Lauren Gallinari, an analyst at shipping brokerage and maritime consultancy MJLF & Associates (MJLF), stated that among the 926 VLCCs currently in service, 205 (about 22%) are over 20 years old and need replacement.

Geopolitical risks are another key factor. Ongoing tensions in the Strait of Hormuz are affecting market expectations, with the current crisis likely forcing major oil-importing countries to significantly increase strategic petroleum reserves. This implies that oil demand will far exceed actual consumption levels for years to come, creating long-term benefits for VLCC transportation. Lauren Gallinari believes that shipowners are willing to invest heavily at historically high vessel prices based on their assessment of the long-term evolution of the geopolitical situation. Additionally, earnings levels and charter rates have supported the order boom—one-year time charter rates remain high year-on-year, and charterers are willing to commit to forward deliveries, boosting shipowners' confidence in placing orders.

The boom in the newbuilding market has also spilled over into the secondhand vessel sector. In the first six months of 2026, VLCC secondhand vessel transactions reached 127, compared to just 85 for the entire year of 2025. About half of these transactions were concentrated early in the year, led by South Korean shipowner Sinokor, backed by the Aponte family behind Mediterranean Shipping Company (MSC). With newbuilding delivery times extended to three to four years, secondhand vessels have become more favored, driving up prices. Signal Ocean data shows that a five-year-old VLCC is currently valued at $174.5 million, higher than the $129.8 million price of a newbuilding, indicating the market's willingness to pay a premium for immediate tonnage.

Despite the already substantial volume of newbuilding orders, analysts believe that given about a quarter of the global VLCC fleet is over 20 years old, the market can absorb this new capacity without excessive concern over oversupply in the short term. Looking ahead to the second half of the year, multiple analysts expect the momentum for VLCC newbuilding orders to continue, though the pace may slow compared to the first half. Analyst Rebecca Galanopoulos concluded that, overall, the underlying drivers fueling this cycle are expected to persist, even if the order pace moderates from the extreme levels seen in the first half.